Find out how to transfer money abroad safely to protect your hard-earned cash, and everything else to consider if you’re looking for the safest way to send money internationally.

Sending money across borders shouldn’t feel like a high-stakes gamble. Finder statistics reveal that 24% of Brits cite security as the most important aspect for a money transfer. So, it’s no surprise that looking for the safest way to send money internationally is increasingly becoming a key priority.

However, if you’re trying to find out how to transfer money abroad safely, where do you even start and what do you need to look for? We’ve got you covered. Here we’ll explain all the safe ways to transfer money to another country and how to decide the best transfer service to use.

What are the safest ways to send money internationally?

As technology advances, it’s more important than ever to make sure your money transfers are safe and secure. Some transfer services, like TapTap Send for example, have even implemented measures like AI-powered fraud detection, to help ensure that artificial intelligence is working for you and not against you.

You’ll generally find yourself choosing between 3 main pathways: digital money transfer apps, traditional bank transfers, and physical cash pickup services. While all 3 are heavily regulated, they approach security, speed, and cost from completely different angles.

Digital money transfer platforms (specialist fintechs)

Modern fintech platforms like Taptap Send, Wise, and Remitly have completely revolutionised cross-border payments. These slick apps run circles around traditional banks when it comes to real-time security.

Because they build direct digital pipelines into local infrastructure (such as the PIX network in Brazil or UPI transfers in India) the money moves rapidly and securely without passing through multiple intermediaries. So, you get an ideal balance between safety, speed, and cost.

Transfer safety example: Taptap Send is fully FCA Authorised as an Electronic Money Institution (FRN 900842) and is independently SOC 2 Certified (“System and Organization Controls 2” – a voluntary cybersecurity and compliance framework), meaning rigorous external audits have verified its data-handling controls. Plus, it delivers 93% of global transfers in under 5 minutes with no transfer fees for most corridors.

Traditional bank transfers (high street banks and mainstream institutions)

Your local high-street bank like HSBC, NatWest or Barclays, provides a tried and trusted way to send money abroad safely, but it comes at a steep premium. Banks rely on the legacy SWIFT network, routing your money through various international correspondent banks.

While highly secure, this multi-stop relay network means your transfer can take a number of working days, leaving your funds hanging in limbo far longer compared to a digital transfer app. Also, banks typically hit you with high upfront transfer fees and uncompetitive, marked-up exchange rates.

Transfer safety example: HSBC UK is authorised by the Prudential Regulation Authority (FRN 765112) and regulated by the Financial Conduct Authority (FCA). It safely conducts transfers via the legacy global SWIFT network, securely moving funds internationally within 1 to 5 working days but with fees of up to £5.

Old-school legacy operators like Western Union and MoneyGram allow you to fund a money transfer online or in-store for a physical collection at an overseas branch.

This method is highly regulated and useful if the person you’re transferring to doesn’t have access to a bank account or digital wallet. However, physical cash introduces its own set of real-world safety vulnerabilities.

While the initial international transfer to a branch can be secure, your recipient faces the physical security risk of traveling to a storefront to pick up physical cash and bank notes, making it a less safe end-to-end method than digital routes.

Transfer safety example: Western Union provides customer protection under global regulatory frameworks, leveraging a secure Money Transfer Control Number (MTCN) tracking system that allows recipients to collect physical cash safely at hundreds of thousands of global locations within minutes, but fees can range from £2 to £25.

Bank transfers vs. international money transfer apps security features

Here’s how traditional banks hold up against modern fintech apps from a security perspective when it comes to core safety features:

Security feature

Traditional high-street banks

Specialist money transfer apps

Best service for this feature

Identity verification

Rely on legacy credit agency background checks, slow manual document uploads, or in-branch physical paperwork.

Real-time KYC (Know Your Customer) checks using instant, automated biometric ID and facial scanning.

Revolut – offers an incredibly fast, automated onboarding process that prevents identity fraud seamlessly.

Underlying network

Move money via the legacy SWIFT network, bouncing your funds through multiple intermediary clearing banks.

Direct digital integration with local payment networks like PIX (Brazil), UPI (India), or mobile money networks.

Wise – its far-reaching, proprietary global network of local bank accounts bypasses SWIFT entirely for faster, safer transfers.

Fraud and threat detection

Mostly reactive security setups that flag unusual activity or freeze your accounts after a shady transaction has already happened.

AI-powered fraud detection machine learning models analysing billions of transfer signals and patterns in real time.

Taptap Send – uses a proprietary machine learning model that analyses every transaction in real time. Unusual patterns trigger automatic alerts or transaction blocks.

Transaction authentication

Basic online password entries, cumbersome hardware card readers, or simple SMS text message authorisation codes.

Integrated biometric authentication (face ID/fingerprint) paired with advanced global 3D Secure 2 (3DS2) protocols.

Stored on massive, centralised legacy corporate banking frameworks that are secure but prone to bureaucratic lag.

Bank-level encryption (TLS) for data in transit and at rest; strict data protection setups and industry certifications.

Taptap Send – stands out for being independently SOC 2 Certified, verifying its rigorous, audited data handling and privacy controls.

Fund protection

Automatically backed by the government-backed FSCS deposit scheme, protecting your cash up to £120,000 if the bank fails.

Regulated Electronic Money Institutions (EMIs) must safeguard 100% of customer funds in ring-fenced, separate accounts.

High-street banks – the FSCS provides a significant safety net, whereas apps legally hold your cash separately so it can’t be touched if they go under.

Taptap Send is an example of a global transfers app that’s authorised and regulated by major national bodies such as the Financial Conduct Authority, and uses encryption, biometrics and segregated accounts to protect its users’ funds.

How to safely transfer money abroad

If you want to master how to transfer money abroad safely, follow this step-by-step checklist every single time you open an app or log into online banking to carry out an international transfer:

Verify the regulatory status. Before attempting to transfer a single penny, verify the service is authorised and regulated by a top-tier regulator like the UK’s Financial Conduct Authority (FCA).

Double-check recipient details. Typos and human error are the number one cause of missing funds. Make sure the name matches their ID exactly, and carefully verify local routing numbers, UPI IDs, or mobile wallet accounts.

Activate multi-factor authentication. Never rely on a password alone. Always enable Face ID, fingerprint scanning, or two-factor authentication (2FA) apps to keep your transfers secure and safe.

Confirm the safeguarding policy. Ensure the provider explicitly uses segregated accounts, has adequate insurance in place or is protected by compensation schemes like FSCS in the UK or the Deposit Guarantee Schemes (DGS) in Europe.

Avoid public Wi-Fi networks. This is a tip to keep in mind when travelling, always try to avoid an international money transfer while connected to unencrypted public Wi-Fi at a cafe or airport. Always use a secure home network or your phone’s data connection where possible.

What are the risks involved with international money transfers?

While modern infrastructure makes cross-border payments incredibly secure, navigating the space still requires a sharp eye. Here are some of the most common transfer risks and how to bypass them completely:

Falling prey to authorised push payment (APP) scams

This happens when a fraudster tricks you into willingly sending them money under false pretences – such as posing as a HMRC tax agent, an emergency utility company, or even a romantic interest. Once you authorise the transaction, the money is gone.

How to avoid it: Never send money to someone you do not know personally. Remember that reputable remittance platforms and official bodies will never call, text, or email you demanding an urgent transfer or asking for in-depth personal or account details.

Company insolvency and bankruptcy

If a non-bank financial institution unexpectedly collapses or goes bust while your money is mid-transit, your cash could potentially get trapped in corporate bankruptcy proceedings if the provider hasn’t managed its regulatory obligations.

How to avoid it: Only use platforms that strictly adhere to FCA safeguarding rules. For example, providers like Taptap Send and Wise keep your funds isolated in legally separate, ring-fenced customer accounts, ensuring your money is protected and returned to you even if the platform goes under.

Currency devaluation and teaser rates

Some providers lure you in with attractive “teaser rates” on your first transfer, only to quietly hit you with heavily marked-up exchange rates on your second and third transactions.

How to avoid it: Choose transparent providers that reject teaser rates entirely. Ideally, using a service that handles exchange rates dynamically throughout the day using live mid-market feeds, ensuring you get consistent, reliable value across every single transfer you make.

Bottom Line

If you’re transferring massive, multi-thousand-pound sums (anything over £10,000), traditional high-street banking rails or dedicated corporate currency brokers remain a safe transfer option, despite their slower processing speeds and clunky compliance pipelines.

However, for everyday global transfers, mobile-first specialist apps are the undisputed sweet spot for both safety, cost and convenience. These platforms are proof that you don’t have to sacrifice speed or be at the mercy of hidden fees just to keep your money safe. By combining a range of safety measures they deliver a secure, transparent, and efficient way to safely send money internationally.

Frequently asked questions

Can you track an international money transfer to ensure delivery?

Yes, most digital platforms provide real-time transaction transfer tracking and instant push notifications directly to your phone the second your funds leave your account, clear compliance screening, and land in your recipient’s digital wallet or bank account.

If you use a traditional bank, you can request a SWIFT MT103 document, which acts as a digital receipt to trace your cash across intermediary banks.

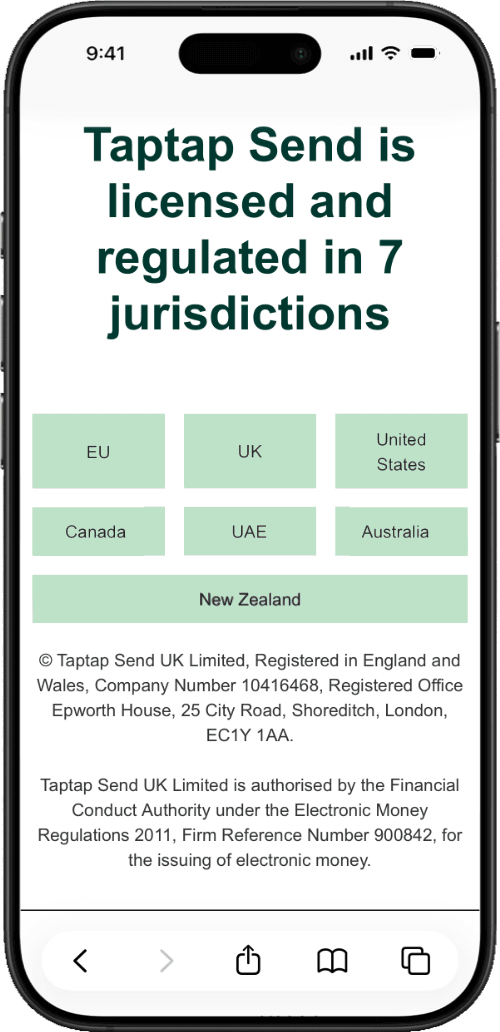

How do you verify if an online money transfer service is legitimate and licensed?

Scroll to the footer of the provider’s official website or app store description to find their regulatory credentials.

For example, a legitimate UK provider will explicitly display their Financial Conduct Authority (FCA) status, such as Taptap Send UK Limited noting its authorisation under the Electronic Money Regulations 2011 (FRN 900842). Cross-reference this number directly on the official FCA public register.

What are some common international money transfer scams?

The most prevalent scams include phishing emails pretending to be your app provider asking you to “verify your password,” romance scams where an online acquaintance requests emergency cash, and advanced-fee scams promising a massive payout if you send an initial processing fee.

Always stay alert and remember to protect your personal details; a secure provider will never ask for your full card or password info over a random phone call.

Which of the safest international money transfers method is the cheapest?

Specialist digital transfer apps are almost always the most cost-effective and secure choice.

Unlike traditional banks that charge hefty transfer fees and hide extra costs inside marked-up exchange rates, these platforms offer transparent, daily negotiated exchange rates with no transfer fees on the majority of their corridors.

What should I do if an international money transfer goes missing?

First, check your transaction receipt to confirm that you didn’t make a typo in the recipient’s name or account number. If the details are completely accurate, get in touch with your provider’s customer service team immediately.

Opting for apps that offer 24/7 customer support via in-app chat, text, or email means you can get a real human on the case at any hour of the day.

Sources

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

George is a deputy editor at Finder. He has previously written for The Motley Fool UK, Nasdaq, Freetrade, Investing in the Web, MoneyMagpie, Online Mortgage Advisor, Wealth, and Compare Forex Brokers.

He's focused on making personal finance and investing engaging for everyone. To do this he draws from previous work and his Level 4 Diploma for Financial Advisers (DipFA), sharing what he’s learnt. When he’s not geeking out about money, you’ll find him playing sports and staying active.

See full bio

George's expertise

George

has written

283

Finder guides across topics including:

A traditional bank account may not be necessary to transfer or receive funds when you’re looking to send money. Learn what to use and how long it’ll take.

How do you know if your international money transfer made it safely? Learn how to track or cancel, and find out what your rights are when it comes to sending money.

Paying a bill in another country? Compare international money transfers so that you can find the best deal for you.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.