We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

Approval for any credit card depends on your status. The representative APRs shown represent the interest rate offered to most successful applicants. Depending on your personal circumstances, the APR you're offered may be higher, or you may not be offered credit at all. Fees and rates are subject to change without notice. It's always wise to check the terms of any deal before you borrow. Most of the data in Finder's comparison tables is provided by Defaqto.

Today’s longest Balance transfer deals at a glance

Rank

Product

Months at 0%

1

TSB Platinum Balance Transfer Card

38

2

Royal Bank of Scotland Longer Balance Transfer Credit Card

36

3

Ulster Bank Longer Balance Transfer Credit Card

36

4

Virgin Money Balance Transfer Credit Card (36 Mths)

36

5

NatWest Longer Balance Transfer Credit Card

36

6

MBNA Ltd Long Balance Transfer Credit Card

36

7

HSBC Balance Transfer Credit Card (36 Mths)

36

8

Barclaycard Platinum Balance Transfer (36 Mths)

36

9

Tesco Bank Balance Transfer Credit Card

36

10

Lloyds Bank Long 0% Balance Transfer Card

35

11

Halifax Longest 0% Balance Transfer Credit Card

35

12

Santander Everyday Long Term Balance Transfer Credit Card

34

13

M&S Bank Transfer Plus Credit Card

30

14

Nationwide Building Society Member Credit Card (BT Offer)

30

15

Virgin Money Balance Transfer Credit Card (30 Mths)

30

Picking the best long 0% balance transfer deal

To access the longest available 0% deals, you’ll need good credit and you’ll probably have to pay a small transfer fee – this can be added onto the balance you’re transferring. The absolute longest 0% deal currently available is months, but it’s important to factor in the transfer fee and any ongoing fees when you’re picking the right deal for you.

If you don’t need quite so long at 0%, you should consider a low- or no-fee balance transfer deal. Although these offers won’t have the very longest 0% interest periods on the market, if the 0% periods that they do offer can give you long enough to clear your card debt, they’re likely to be the cheapest option. You can use the filters on our comparison above to quickly find the longest deals with and without a balance transfer fee.

4:08

An intro to balance transfers

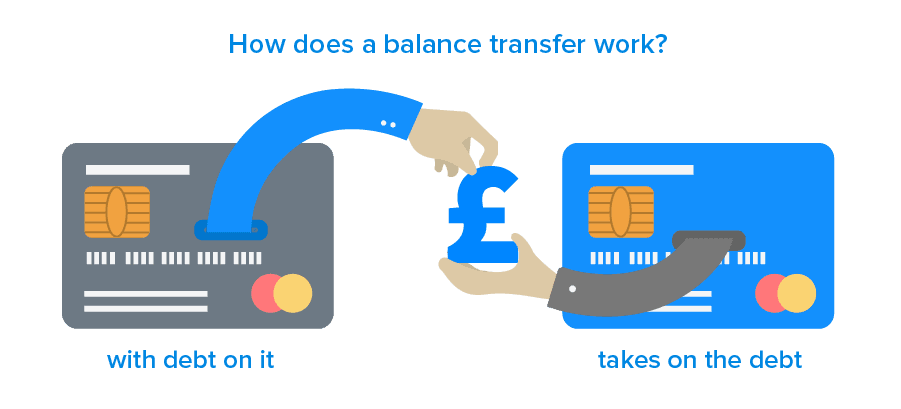

Whether you’re looking to pay off your existing credit card debt or wanting to organise your debts into one place, with cards offering low or 0% interest for a specified period, a balance transfer card could help pay off your debt faster.

A balance transfer refers to the process of transferring your existing credit card debt to a new card issued by a different bank, in return for a lower interest rate during the introductory period. Most balance transfer credit cards have an introductory promotional rate which runs for a fixed number of months.

If used correctly, you could transfer your existing balance from a different bank and make use of a card with up to 12, 24, 30 months (or even longer!) 0% interest on your balance. This means that you could pay off your debt within this time period without any monthly interest being added on top, or pay off a considerable amount of debt before the monthly interest kicks in.

So, what’s the catch?

After your specified 0% balance transfer period ends the provider will begin to charge you monthly interest on your remaining balance, just like a usual credit card. There may also be a balance transfer fee to pay when you are moving existing debt to a balance transfer card. This fee, however, is usually low compared to the interest you may be paying on your current credit card balance. Even with this fee, a 0% interest rate usually means that you can clear your debt faster and more cheaply than you would if you remained with your current card.

How much will it cost to clear my balance?

Complete the fields above to estimate your monthly repayment

How does it work?

Let’s assume that you already have existing card debt and you want to save on interest by moving it to another card issuer.

Once you’ve picked a balance transfer deal, you’ll usually be prompted to check your eligibility. Provided its good news, you can then go ahead and apply for the new card.

During the application process, you’ll be asked if you want to transfer a balance and prompted to provide details of how much it is, which bank it’s currently held with and the account number.

When you’ve received your shiny new card (which can take up to two weeks) and activated it, the card issuer will then request the transfer of all outstanding funds from your old bank. From this point, the transfer will typically take around 1-3 working days. If there’s a transfer fee involved then this can be added to your balance.

From then on it’s over to you. You can pay as much or as little as you like each month, subject to the new card’s minimum repayment requirement (typically 1% or 2% of your outstanding balance). Ideally, you should pay enough each month to ensure you’re debt-free before the introductory low-rate period expires.

What is a balance transfer fee?

Most – but not all – balance transfer cards (particularly those with the longest promotional periods) charge a balance transfer fee. This is a one-time fee that’s calculated as a percentage of the debt you wish to transfer to the new card. Typically the balance transfer fee is between 1.5% and 3.5%. A minimum is usually also specified, so a card issuer might describe its balance transfer fee as “3% (minimum £5). So if you had a £2,000 debt to transfer, the transfer fee would cost you £60. If you had just a £150 debt to transfer, the fee would cost you £5.The fee is usually added to the balance and so also benefits from the 0% promotional period.

If you can afford to pay off your balance in a shorter amount of time, it’s worth looking for a balance transfer card that has no balance transfer fee, but might offer a shorter 0% deal.”

Expert video: Choosing the right balance transfer card

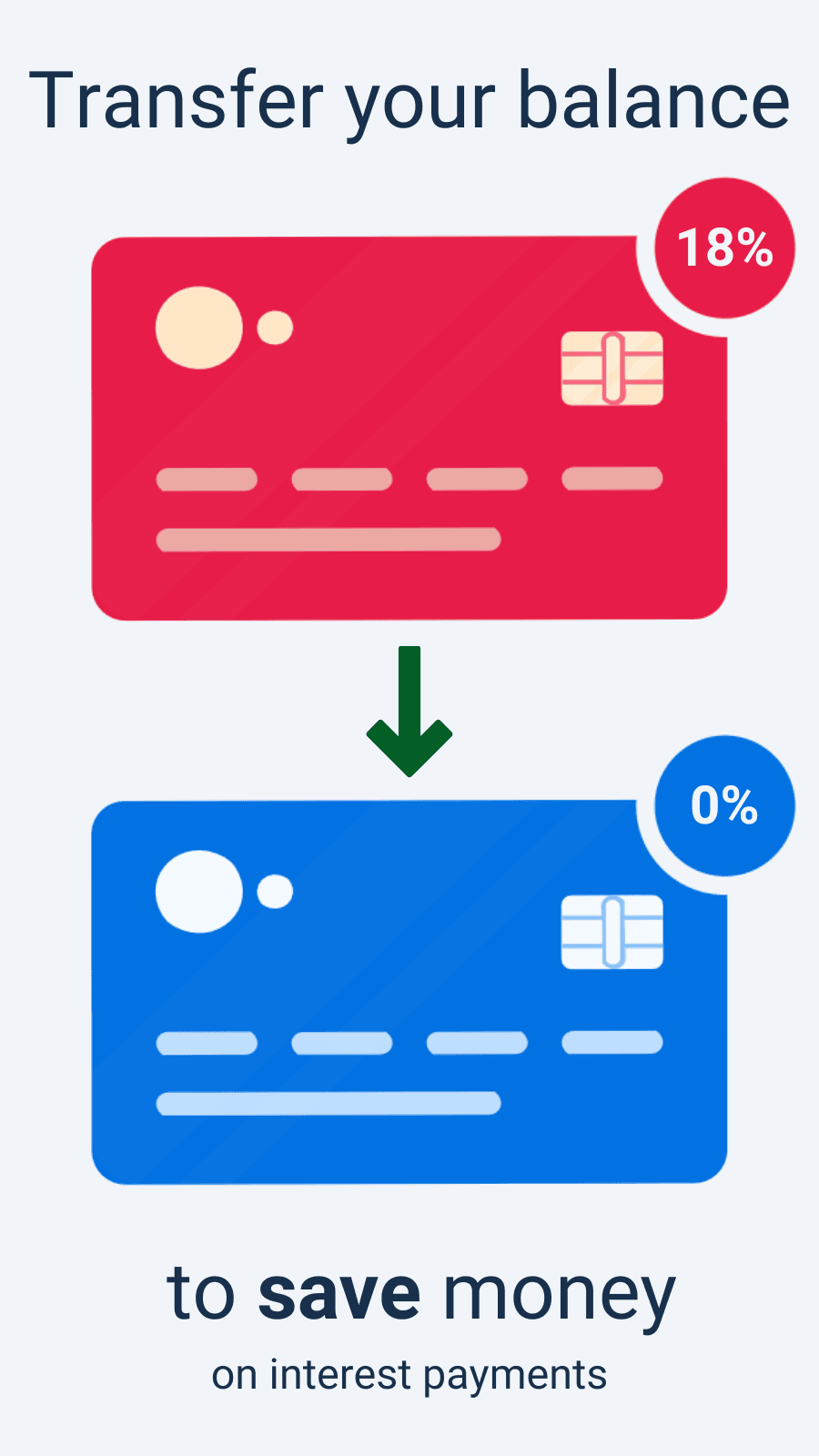

How much money can I save with a balance transfer?

Exactly how much you’ll save will depend on the size of your debt, the length of the 0% balance transfer offer and your repayments, but you could save hundreds or thousands of pounds in interest while you clear your debt. Here’s an example:

Balance transfer illustration

Let’s say you have £3,000 debt on a card that’s currently charging 20% interest annually, but you’ve been offered a new card with 0% on balance transfers for 18 months, a 3% transfer fee and no annual fee.

Clearing your debt over 18 months would be around £407 cheaper using the new 0% card than it would on the old card. What’s more, you’d be debt-free three months sooner than if you’d made the same monthly repayments to your old card. All in all, a worthwhile exercise!

Remember that this isn’t based on simply paying the minimum monthly repayments, but on overpaying as much as is necessary to completely clear the debt before the revert rate kicks in. In this example you’d want to pay around £172 each month to clear the debt in time. To get that figure we divided £3,090 (the balance being transferred with the transfer fee on top) by 18 (the number of months in the introductory rate period).

The dos and don’ts of balance transfers

Used intelligently, a 0% balance transfer card will reduce your interest payments and get you out of credit card debt faster. Used the wrong way, your debts can become larger and last, well, indefinitely. Ensure you don’t get trapped in problem balance transfer debt with our dos and don’ts.

How to do balance transfers right

DO: Compare the best deals and use eligibility checkers. Your goals should be to get debt-free as cheaply as possible and in as little time as possible. To do this, you’ll want to pin down the best deal available to you.

DO: Look at deals with no balance transfer fee first. Many people don’t take the time to understand balance transfers and the potential costs involved and end up paying a balance transfer fee that they hadn’t been banking on. If you’re reading this, you’re already ahead of the curve.

Do: Consider all applicable fees While you won’t be charged interest with a 0% balance transfer, you may have to pay annual fees and a balance transfer fee. Make sure you consider these when choosing a balance transfer deal, but bear in mind it can be a mistake to dismiss cards purely based on fees.

DO: Request the transfer at the earliest possible opportunity. Most balance transfer deals only apply to balances transferred within the first 60 or 90 days of account opening, so it’s better not to hang around.

DO: Keep making payments on your old card until you’re sure the transfer has gone through. Balance transfers are still far from instant, frustratingly. In fact, they can take a couple of weeks. Don’t risk damaging your credit record by missing a repayment on your old card.

DO: Set up a direct debit for repayments. Ensure you’ll never miss a repayment and protect your credit score by setting up a direct debit for repayments. You can do this during the application when you accept the offer that the card issuer has made. You can set up a direct debit to pay the minimum monthly repayment, a fixed amount or a fixed percentage of the outstanding balance. Choosing a fixed amount of direct debit is likely to be the most straightforward option – simply divide your balance (plus the transfer fee, if applicable) by the number of months in the 0% deal to see what you need to pay each month to be debt free at the end of the promotional period.

Mistakes to avoid with balance transfers

DON’T: Forget you still have to make payments. Despite the promotional period with interest at 0%, you still have a debt, and you still have to make at least the minimum payment each month. You can’t simply transfer a balance and then stop making payments. The minimum repayment is usually stated in terms like “2.5% of your outstanding balance or £5 (whichever is greater)”.

DON’T: Forget to check the standard interest rate. Once your balance transfer promotion finishes, you’ll be paying the standard rate on any remaining balance. Choose a card with a standard rate that’s lower than your current credit card rate if possible or make sure you repay the entire debt before the standard rate applies.

DON’T: Use your card for further spending. Adding new debt will slow down your ability to repay your card. Don’t buy anything new on your credit card that you can’t immediately pay off in full. Also, banks are required to allocate repayments to whichever debt is accruing the highest interest on your account. So, if your balance accrues 0% interest and your purchase collects the standard interest rate, your repayments will go to the purchases rather than your balance transfer. It’s usually better to focus on clearing the debt you have, rather than adding to it. However, there are cards which offer 0% deals on both existing debt and additional purchases. Watch out for rewards programmes that incentivise additional spending – you could end up paying much more in interest than you earn in points.

DON’T: Only pay the minimum repayment each month. If you’re only paying the minimum repayment each month, you won’t be able to repay the entire balance by the time the 0% balance transfer offer ends. Then your debt will start to collect interest and it will grow again. Instead, you should calculate exactly how much you need to pay each month to repay the entire balance by the time the interest-free period ends. You can do this by dividing the size of your debt by the number of months in the balance transfer offer. This will give you a goal repayment to meet every statement period to clear the debt before the 0% promotion ends.

DON’T: Keep your old card open It’s tempting to hang on to your old card “for use in emergencies”. Realistically, if you’ve run up debt on it before, you’re likely to do so again. Cancel the card and concentrate on paying off your balance. Remember to transfer any regular payments, and ask your old bank for your final balance so you don’t have any leftover debt. Even after you’ve made a balance transfer you may still be liable for accrued interest from your final statement, or for missed payment charges. Make sure these are cleared – if you don’t take action they’ll continue to build up interest and penalties.

How to do a balance transfer in five steps

Follow these five steps to successfully apply for a balance transfer credit card and improve your chances of approval:

Compare balance transfer offers to get a sense of what’s out there. Use our comparison tables to easily compare a range of cards and see how much you could save.

Use an eligibility checker to see which cards you could get approved for. Soft-searching eligibility checkers (like Finder's!) can show you your likelihood of approval for a range of cards from popular providers. You can also start to get an idea of the credit limit you might be offered. Some banks don’t show this until you actually apply, but luckily, some do. The amount you can transfer to your new account will vary, but is usually capped at between 90% and 95% of your credit limit. So, if you can only transfer 90% of your £1,000 credit limit, you’ll only be able to transfer up to £900. Remember, you won’t know for sure what your credit limit will be until you’ve made your application, and this will depend on a number of factors, such as your overall credit rating, income and employment status. You can contact the bank in question to get an estimate before you apply. You’ll also need to make sure that you’ve selected a new card that accepts transfers from your current bank and card.

Submit your application. If you’ve found a balance transfer credit card that looks right for you, you can click on the “Go to site” button to be directed to a secure online application.

Wait for your application to be approved. Most banks can process your request and offer approval within 60 seconds of applying, but some can take a couple of days. If you haven’t heard from the bank after this time, you may wish to contact them to find out if there’s an issue. During the application process, you’ll be asked if you want to transfer a balance.

Confirm the transfer has taken place then close your old account. Once your new card is set up, contact your old bank and make sure the previous account is closed to avoid any further fees or interest payments.

Chip away at that card debt! Now it’s time to start repaying your debt, with the goal of clearing it all before the end of the 0% period.

Do I have to contact my old bank and new bank to make the switch?

Your new card issuer manages this process after both your card and the balance transfer are approved. You just need to provide details of your existing card when you apply. But if you want to close your old card, you’ll need to do that yourself by contacting your bank. If you don’t close your old account, you could be stuck with annual fees and any other maintenance costs that come with your existing account.

How does transferring a balance from one credit card to another impact my credit score?

When you transfer a balance from one credit card to another, it’ll save you money on the interest you’re paying and could help you pay off your debt faster, which could potentially boost your credit score. However, when opening any new credit account, it could negatively affect your credit score in the short term.

So, before you decide to go for a balance transfer, it’s important to weigh the potential long term benefits against the short term effects on your credit score. Consider how much money you’ll save in interest and how quickly you can pay off your debt compared and ultimately, it’s about finding the right balance for your financial situation and goals.

Your questions about balance transfers answered

Applying for balance transfers

Maximum balance transfer limits can vary slightly from card to card, but typically you can transfer up to 95% of your credit limit. Your credit limit is set by the card issuer and it’s based on its assessment of your circumstances – taking into account factors like your income, outgoings and credit record.

You can use the product reviews on Finder to confirm the maximum percentage of the credit limit you can transfer to a particular balance transfer credit card.

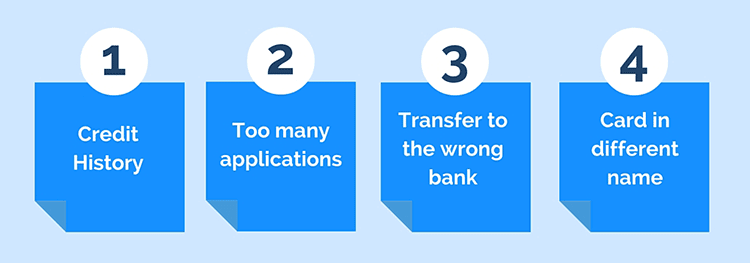

Financial institutions assess balance transfer applications carefully. To increase your chances of approval, consider some of the factors that could cause a bank to decline your application before you apply:

Poor credit history. You’ll need a good credit history to obtain a balance transfer deal. However, if you have a poor credit history due to missed payments, defaults on your account or significant levels of debt, you might need to repay more of your debt and demonstrate your ability to make regular repayments before you apply.

Submitting multiple applications too rapidly. Each application you make for a balance transfer deal is recorded in your credit history. If your application is refused, don’t just apply to a different credit card issuer straight away. Instead, take some time to repay your debt and carefully compare other card options and ensure that you tick off the eligibility criteria before you apply.

Transferring to the wrong bank. If you try to get a balance transfer deal from a bank with the same owner as your current card, you’ll be immediately refused. You can’t transfer your debt from a Royal Bank of Scotland account to a NatWest card, for instance, as they’re both owned by the same group.

Cards in a different name. Your new balance transfer card must be in the same name as your current card. If you apply with a different name, such as your partner’s name, you’ll be turned down.

Yes. Providing that both you and your partner/spouse are already using a joint-account credit card. However, you usually can’t transfer a debt that is in someone else’s name to a new account that is under your name.

The key rule that decides whether you can transfer a balance to a bank is whether or not your existing bank belongs to the same credit provider. For example, balance transfers are not allowed between NatWest and Royal Bank of Scotland since RBS is the credit provider for both.

No. Existing customers are ineligible to apply for balance transfer offers with their existing bank. However, if you then transfer your balance to a different bank, when this balance transfer promotion has ended you will be able to transfer to the first bank again.

Credit card issuers make money when you pay interest, so why would they charge 0% when they could charge 22% or more? Here’s why:

You’ll eventually revert to a higher rate. If you don’t pay off your entire debt at the 0% rate, you’ll end up collecting interest at the standard rate for your card. This is usually the purchase rate or cash advance rate, which can range between 9% and 22%. Once that happens, your new credit card issuer can potentially make hundreds or even thousands of pounds from you in interest charges.

Persuading you to switch is tough. People are reluctant to switch banks, and it’s expensive to acquire a new customer. Offering a discounted interest rate is one of the cheapest ways for banks to attract potential customers. It’s essentially a cheap form of marketing.

No, you typically can’t perform a balance transfer while staying with the same institution. You also can’t perform a balance transfer to other banks within the same group or owned by the same organisation. For instance, you can’t transfer from NatWest to Royal Bank of Scotland as both banks are part of the same company.

While most balance transfer deals are for credit card debt, some credit card issuers will let you transfer debt from a personal loan or store card as well. You may wish to consider a money transfer credit card instead – these let you control the transferring, so you can transfer funds from the card to your current account, for any purpose.

While you could be approved for your credit card within 60 seconds, it can take between 1-2 weeks for your old balance to appear in the new account. Please note that the 0% balance transfer offer applies as soon as your card is approved rather than when your balance is in your account.

Using balance transfers

Yes you can, although it’s not recommended if your main objective is paying off existing credit card debt. The interest-free period will depend on the card. Most providers offer a standard 56-day interest free period, while others offer longer promotional periods alongside balance transfer deals. However, some card providers offer a “all-rounder” or “matched” credit card which offers 0% interest-free on both balance transfers and purchases for a specific period.

You should make repayments by the due date detailed on your bank statement for each statement period. While you’re only required to pay the minimum repayment, you should always aim to pay more to clear your debt faster. This is especially important when you’re using a 0% balance transfer offer that will only apply for a promotional period. To avoid paying interest on your debt, you should calculate how much you need to pay each month by dividing the size of your debt by the number of months in your promotional period. This will give you a goal repayment to make each month to repay your balance before the promotion ends.

Yes, you can repay your balance as early as you’d like. In fact, it’s wise to clear your debt as fast as possible to avoid reverting to more expensive standard rates and incurring any additional interest costs. Unlike a fixed-schedule personal loan or home loan, there are no penalties for clearing your credit card debt ahead of time.

Banks will allocate your repayments to the highest rate of interest first. This means that with a low interest rate balance transfer promotion, repayments will usually go towards purchases and cash advances first. As a result, it is ideal not to make other transactions when repaying a balance transfer to ensure that all of your repayments are dedicated to clearing your debt.

Most credit cards offer a set period of interest-free days as a standard feature of the card – some will offer promotional interest-free periods of up to 30 months. During this time, you can use your card to make purchases and you won’t pay any interest on them for the duration of the period. However, if you don’t pay off the balance resulting from these purchases within the agreed time-frame – which is a separate time-frame from your balance transfer deal – you’ll be liable for interest. In some cases, missing payments on purchases will also invalidate your balance transfer deal. The exact terms and conditions will depend on your bank.

Your old credit card will remain active even when your balance has been transferred. You can either continue using it or request that your old bank cancel the card. Don’t forget, your old card may have an annual fee, so forgetting to cancel it could cost.

Yes, it’s possible to transfer a balance after you’ve applied for the card. However, the exact terms and conditions of doing this vary between banks. It’s a good idea to contact your bank directly to discuss your options, but here are some examples of bank processes below:

Halifax. Promotional balance transfer rates are available for all transfers made in the first 90 days, a 3% fee applies thereafter.

Santander. Transfer a balance fee-free at any time during the promotional period.

Barclays. You can apply for a balance transfer offer within 60 days of card approval.

TSB. Balance transfers must be made by a certain date depending on the specifics of the promotion it is running at any given time.

Sainsbury’s Bank. In the first 3 months a 1.5% balance transfer fee is charged and then fully refunded directly to your account within 60 days. A 3% fee applies thereafter.

Sources

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Was this content helpful to you?

Thank you for your feedback!

To make sure you get accurate and helpful information, this guide has been reviewed by

Rachel Wait, a member of Finder's

Editorial Review Board.

Chris Lilly is Head of publishing at finder.com. He's a specialist in personal finance, from day-to-day banking to investing to borrowing, and is passionate about helping UK consumers make informed decisions about their money. In his spare time Chris likes forcing his kids to exercise more.

See full bio

Chris's expertise

Chris

has written

515

Finder guides across topics including:

Discover the best credit cards with no balance transfer fees. They are a useful tool if you want to take a break from paying interest on credit card debt.

If you have a lot of debt on multiple credit cards, you may have been considering moving all of the balances to one card. Find out how to do so in this article.

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.