Digital challenger bank Monzo offers current accounts, integrated savings accounts, loans and investments in a slick app. We’ve picked it as the best bank for extra features, and these include cashback even with the free account. There are 3 perk-laden, paid-for current accounts, too. Customers love Monzo – 90% in our survey would recommend it.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for bank accounts

To make comparing even easier we came up with the Finder Score. Fees, features and customer service across 20+ of the most popular banks are all weighted and scaled to produce a score out of 10. The higher the score the better the account – simple.

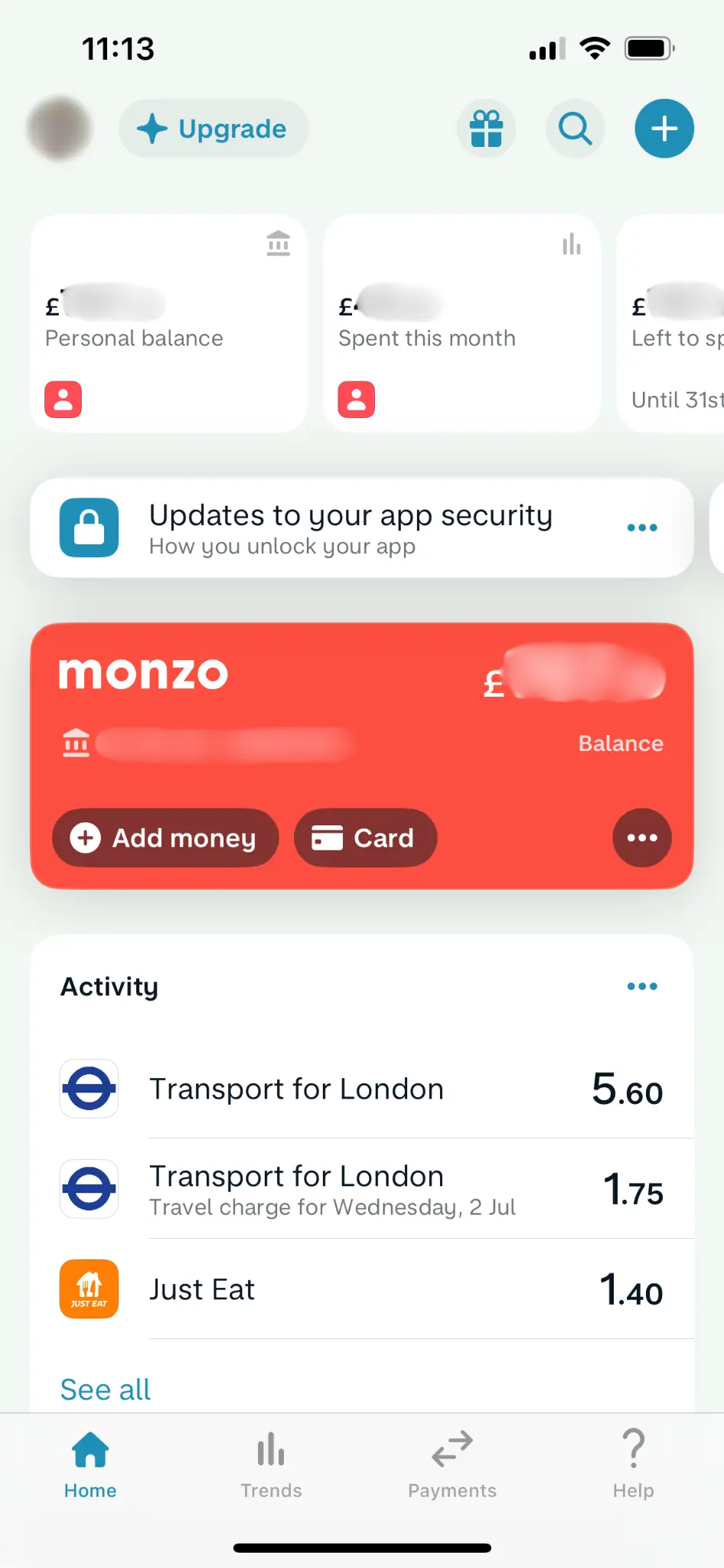

Monzo works in a similar way to any normal current account. When you apply for an account, you’ll be issued with a bright coral contactless Mastercard.

However, the account is entirely managed through the Monzo app, which is jam-packed with cool features and much slicker than your average banking app. The card is even controlled via the app: you can freeze it if it gets lost or stolen (and unfreeze it if you find it again).

Here are some of Monzo’s main features:

Earn cashback. Monzo allows you to earn cashback at popular retailers, restaurants and on travelling. You pick your offers, shop in person or online and see what you’ve earned instantly via the app.

Get paid a day early. Does what it says on the tin!

Salary sorter. Divvy up your salary into spending, savings and bills.

Spending budgets. Set budgets by category (e.g. eating out, entertainment, transport).

Buy now, pay later. Monzo offers a pay later (BNPL) option. If you’re a Monzo account holder, the Flex feature is designed to let you pay for purchases over £30 in a series of instalments.

Investments. Monzo Investments has 3 ready-made fund options all managed by BlackRock. Each fund has a different risk level: Careful, Balanced and Adventurous. So you can choose which one suits you best.

Monzo Extra

Beyond its free current account, Monzo has 3 paid-for account plans: Extra, Perks and Max. Monzo launched all 3 in April 2024 and each offers something slightly different. First up is Extra.

Basically, a Monzo account with a little bit more, Extra offers more advanced money management tools.

For a monthly fee of £3, you get:

Connected banks and credit cards. Add other bank accounts and cards to your Monzo app so you can see all your balances and transactions in one place.

Virtual cards. Link a virtual card to one of your Pots to help with budgeting.

Advanced roundups You can boost your spare change roundups and automatically put 2x, 5x or 10x into your savings every time you spend.

Custom categories Create your own categories to track how much you spend.

Credit insights Monzo now tracks your Equifax, Experian and TransUnion credit scores weekly and offers tips on how to improve your score by making certain changes.

Monzo Perks

Monzo Perks builds on Extra and offers more rewards, discounted fees and interest all for a monthly fee of £7.

Saving interest. Earn a higher rate of interest on your Instant Access Savings Pots.

Fee-fee withdrawals and cash deposits. Benefit from a higher fee-free withdrawal limit and 3 fee-free cash deposits.

Discounted investment fees. You’ll pay less in Monzo Investment fees as a Perks account holder.

Annual railcard. As part of your account you’ll get an annual railcard from Trainline. You can pick which one suits you best depending on your age, where you live and how you like to travel.

Monthly cinema ticket. You will also get a Vue cinema ticket every month, plus 10% off food and drink.

Weekly Greggs treat. Monzo knows its customer base, as it’s introduced a free weekly hot drink or snack at Greggs.

Monzo Max

Monzo’s top-tier account, Max, has everything that Extra and Perks offers plus benefits such as insurance and breakdown cover. Of course, there’s a higher monthly fee as a result and you’ll need to hold the account for a minimum of 3 months.

For £17 a month, you’ll get:

Worldwide travel insurance. Multi-trip cover including medical bills, lost valuables, winter sports and car hire excess. You can also choose to add family cover for £5 extra a month.

Worldwide phone insurance. Protect your phone from loss, theft and accidental damage.

UK and European breakdown cover. Benefit from personal cover including home insurance, onward travel and vehicle recovery.

"Monzo has a new feature where each month, 10 lucky customers get double their salary (capped at a maximum of £10,000). For example, if your take-home pay is £2,000, Monzo will add an extra £2,000 to your account. Sounds amazing, right? Let’s see. This kind of perk is designed to encourage you to use Monzo as your main bank account. To qualify, you’ll need to move your salary to Monzo, either by informing your employer or by using the Current Account Switch Service. But is it worth switching for? At the time of writing, Monzo has around 12.5 million current account customers in the UK, which means your odds of having your salary doubled are roughly 1 in 1.25 million. In other words, it shouldn’t be the deciding factor. It’s a fun bonus if you happen to be one of the lucky 10, but not a reason to switch on its own."

You can use a Monzo card abroad really easily. You don’t have to do anything! Just travel anywhere in the world and there are no charges for card transactions at all and no charges for ATM withdrawals up to £200 a month – then there’s a 3% fee. The monthly limit for cash withdrawals in European countries is slightly higher at £400, but be aware that is a combined threshold for ATM withdrawals made in the European Economic Area (EEA) and the UK (then the 3% fee applies). However, if you’re using Monzo as your main bank account or you’ve got one of the paid-for accounts, fee-free cash withdrawals in the EEA are unlimited.

Alternatively, if spending cash abroad is what is most important to you, you could consider Starling Bank. Starling’s account offering is very similar to Monzo’s, and there’s no charge on overseas card transactions, but there are also no charges at all for withdrawing cash abroad, and the maximum amount you can withdraw at an ATM each day is £300.

Also be aware that individual foreign ATMs may charge a fee too – that’s to do with the ATM network itself and nothing to do with Monzo though. All transactions on your Monzo card in a foreign currency are made at the current day’s Mastercard exchange rate, offering a competitive rate that responds to the live market.

Then, when you get back from your trip, Monzo will send you a little summary of how much you spent.

Can I use Monzo in the US?

Yes, it’s easy to use your Monzo card in the US. You just need to remember the limits mentioned above. As the US is not part of the EEA, you’ll start with a £200 cash withdrawal limit (anything over that will incur a 3% fee). Monzo won’t charge any fees for withdrawing cash, but the ATM provider might, so check before you complete your withdrawal.

There are no fees or limits on spending with your debit card, so if you want to avoid paying extra for cash withdrawals over your limit, use your card for purchases.

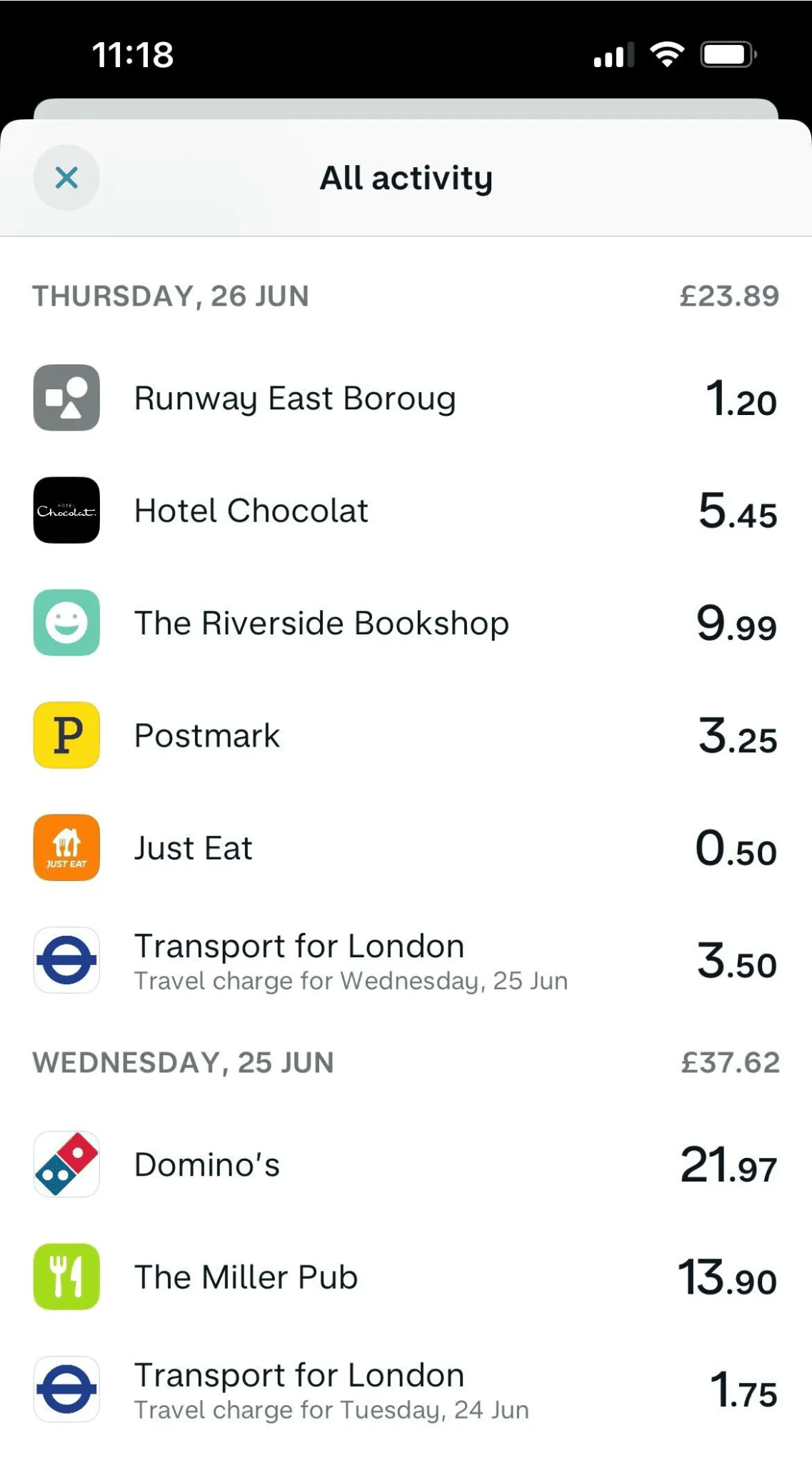

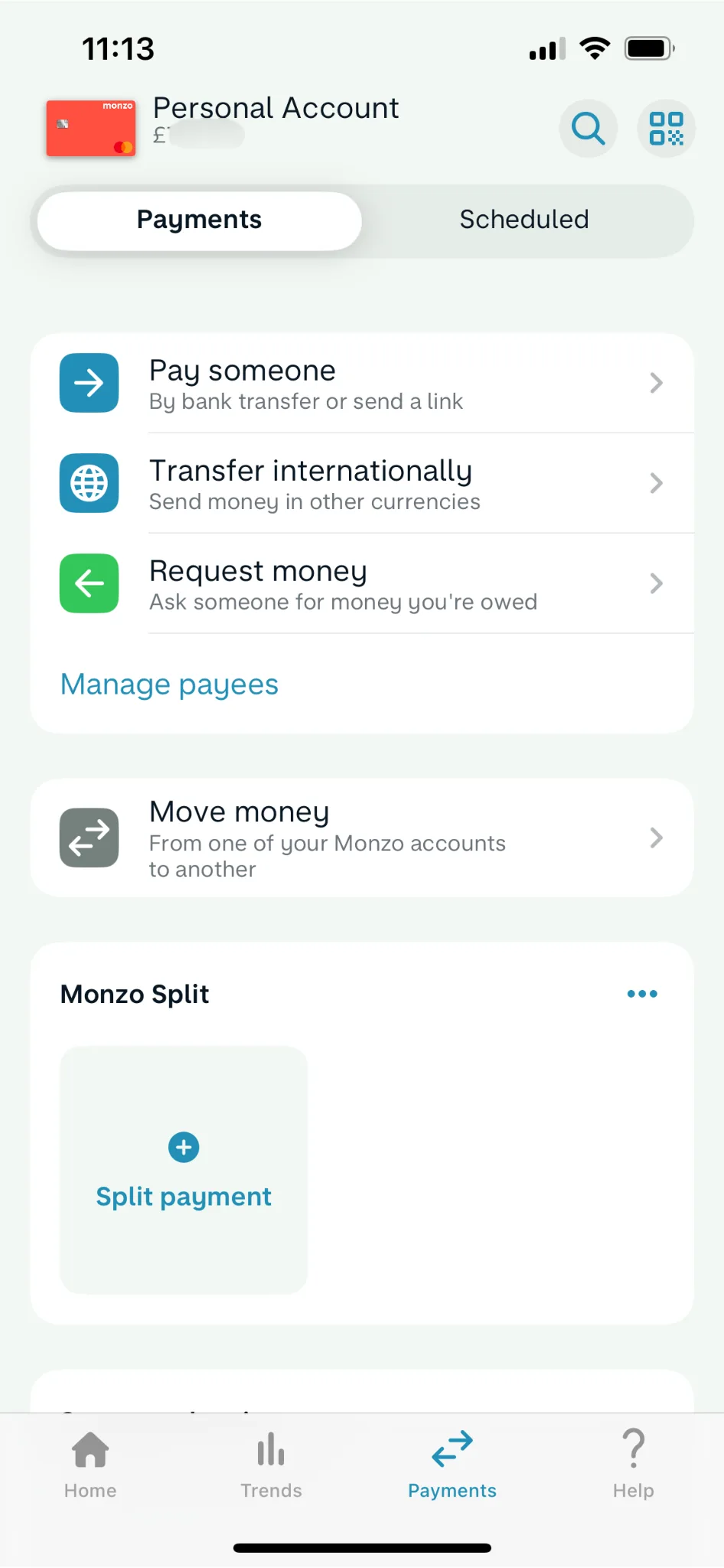

What does the Monzo app look like?

Is Monzo safe?

It’s as safe as any other bank. The money in your Monzo account is protected by the Financial Services Compensation Scheme (FSCS) up to £120,000. The FSCS is an independent statutory fund set up to safeguard consumer finances in the event of a bank being unable to meet its payment demands. Monzo has full FSCS protection, covering up to £120,000 of your money – as is the standard for UK bank accounts.

Does Monzo offer any promotions, discounts or refer-a-friend offers?

Monzo has a refer-a-friend scheme that earns £10 for each person. It doesn’t have any switching deals, but we have a guide on other switching deals if that’s what you’re looking for.

Does Monzo offer joint accounts?

Yes, Monzo offers joint accounts for 2 people. You can apply in the app and you both need to already have a Monzo current account.

Does Monzo offer premium/packaged or premier accounts?

Monzo offers a range of account options and you can subscribe to whichever one suits you best. If you can’t find what you’re looking for, you can compare other accounts in our guide.

What do customers say about Monzo?

93% of customers we surveyed in 2026 would recommend Monzo to a friend.

It's a clear favourite among its users, celebrated for its modern, feature-rich app that provides excellent visibility over spending. Standout features include the highly popular "get paid a day early" function, customisable savings pots, and fee-free spending abroad.

Customers consistently praise the quick, friendly customer service and the overall ease of managing their finances. It is widely regarded as a top-tier digital bank that genuinely helps users take control of their money.

AI-generated summary from the text of customer reviews on Finder.

Case study: Richard found separating his money into pots useful

"I chose to move to Monzo as I like the ability to use the pots feature. It helps to separate my bills, everyday spending money, rent and savings separately and clearly. I also like the idea of the bank being online and not having to visit a branch to resolve queries.

If there’s one thing you’d tell a friend who’s thinking of getting this, what would it be?

I would highly recommend Monzo to a friend. I’d let them know how useful I’ve found the pots feature."

Richard Loftin

Buckinghamshire

Monzo and Finder Awards

Our Finder Awards celebrate brands that truly stand out in their field. Monzo is one of these brands and has won multiple awards!

2025 Provider of the Year Award (Current Account)

2025 Provider of the Year Award (Packaged Account)

2025 Provider of the Year Award (Joint Accounts)

2024 Green Award (Digital Bank)

Customer service information for Monzo

Email support

Telephone support

In-app or live chat

Contact form

Branch support

Pros and cons of Monzo

Pros

Full UK current account – you can do all the stuff you can do with a normal bank and more.

Apply quickly from the app without proof of address – you won't be credit-checked unless you apply for an overdraft.

Slick, fun app that is packed with cool features.

Spend abroad with no fees at the Mastercard exchange rate.

Deposit cash into the account at any store which shows the PayPoint logo.

Buy now, pay later option for account holders (Monzo Flex).

Open a savings account directly from the app.

Fully FCA-licensed and FSCS-protected.

Cons

No bank branches isn't great for those who prefer face-to-face customer service.

3% charge for ATM withdrawals outside EEA over £200 – some other digital bank accounts (e.g. Starling Bank

You need to upgrade your account for full functionality.

Users have reported long waiting times to speak with the customer service team.

Cash deposits can incur a fee depending on your Monzo plan.

All in all, Monzo is great if you’re looking for a mobile-first current account with almost no fees, a slick user experience and a young and fresh vibe. Whether you’re planning on using it as a primary current account for your day-to-day finances or as a secondary account when you travel, it does the job quickly, efficiently and with a degree of cheerfulness.

Alternatives to Monzo

If you want a better option for travel, check out Chase or Starling. They both have higher allowances for withdrawing cash than Monzo’s free account. Monzo’s premium accounts have better limits, but still below what Starling and Chase offer for free.

Monzo’s limits can be quite confusing to understand as it depends on if your account is classified as your main bank account. If it is then you can make unlimited fee-free cash withdrawals in the EEA and take out up to £200 every 30 days for free outside the EEA. After that, Monzo charges 3%. If it’s not your main bank account, then you can only withdraw £400 in the EEA. However, if you upgrade to a paid for plan, you’ll get unlimited fee-free cash withdrawals in the EEA.

Chase lets you withdraw up to £500 a day anywhere. If you’re abroad, there is a £1,500 limit on cash withdrawals in a calendar month. If you’re travelling in the EEA and your Monzo account offers unlimited withdrawals then that’s a better option. But if you’re venturing outside the EEA, Chase beats Monzo’s highest limit (£600 for Monzo Perks or Max) by a long way.

Starling is simpler and better again, as it doesn’t have a monthly cash withdrawal limit. It only has a daily limit of £300. This is the same in the UK or abroad, so you won’t have to change your behaviour or try to remember a new limit while you travel.

If you’re using your card for purchases then all these accounts are the same as they use the Mastercard exchange rate for foreign transactions and don’t charge a purchase fee.

If you want cashback, Chase has a better offering

Monzo started dabbling in cashback in 2023 but rather than paying the same amount on every transaction, it has offers for specific retailers in its app. These all come with expiry dates and are updated regularly, but it’s a bit of a lottery if you’ll get an offer that is actually useful to you. You also have to check regularly and activate the offers you like. You can earn between 2% and 10%, though, so it could save you a lot of money.

Chase offers 1% cashback on eligible purchases made with your debit card for 12 months. You can earn up to £15 a month. After 12 months, you have to deposit at least £1,500 into your account each month to earn cashback. Chase’s rate is the best among debit cards from banks and there’s no annual fee to get it either, which is often the case with other bank accounts.

Monzo’s approach is interesting and does give you the potential to earn more than Chase on some purchases, but the offers you get might not be for things you’re going to spend money on anyway. Chase’s flat 1% rate gives you certainty about how much you can earn and much more opportunity to earn it just for buying things you were going to buy anyway.

If you want an app with more features, check out Revolut

Monzo is a slick and popular app that offers a range of features for everyday banking. But it doesn’t have all of the features that other finance apps do, such as Revolut.

With Revolut, you can send money for free to other accounts in the Single Euro Payments Area (SEPA) and hold multiple currencies in your own account. You’re able to open a free Under 18 account with debit card and app.

Our verdict: Is Monzo a good bank?

Monzo is the most popular digital challenger bank in the UK (by customer numbers), and for a good reason. Its free account is super easy to use, set up and manage, and the app is colourful and fun.

The only real drawback is the limit on free ATM withdrawals abroad, which is quite low compared to that of Starling, for example. For most people this won’t really be an issue, but if you’re a bit of a globetrotter and often travel to countries where cash is still king, you might want to consider the alternatives. Or have a look at some of Monzo’s other account plans which offer higher limits for fee-free withdrawals and cash deposits.

Frequently asked questions

Yes, it has been authorised fully by the Prudential Regulation Authority (PRA) and is regulated by the Financial Conduct Authority (FCA).

No. You don’t have to link another bank account with your Monzo card because when you open an account with Monzo, you will have a full UK current account which will allow you to do all the usual banking stuff.

Here are the ways you can put money into your Monzo account:

1. Transfer funds from another bank account to your Monzo account. 2. Get your salary paid straight into your Monzo account. 3. Deposit cash into your Monzo account at a PayPoint.

Unfortunately not with the free standard Monzo account. However, you can tag your transactions. This means you can still organise your spending, without adding too much complexity. If you do want the ability to create custom categories, you might want to consider upgrading to Monzo Plus.

Yes. All Monzo account debit cards are contactless. You can use your Monzo card on your phone too, with Apple Pay and Google Pay. Welcome to the future!

Yes. Monzo debit cards can generally be used at pay-at-pump fuel machines across the UK.

Yes, you can get your tax credits and child benefit paid into your Monzo account. You just need to give them your Monzo sort code and account number.

You don’t get interest on in-credit balances with the free Monzo account. But you can open a “savings pot” from the Monzo app and these pay interest. The rate you earn depends on the type of account. Our dedicated guide explains everything about saving with Monzo.

Monzo is a digital challenger bank in the UK. It offers current accounts and business accounts that can be set up and managed on your mobile phone. The accounts do come with a contactless payment card, but this is a debit card.

Monzo launched Monzo Flex in 2021. Flex is a type of hybrid of buy now, pay later and credit card. Our experts have reviewed Monzo Flex.

Yes, you can. Monzo offers 5 types of bank account: current accounts, business accounts, joint accounts, accounts for 16-17 year olds and accounts for under 16s. Before you think about setting up a joint account it’s worth remembering that doing so means you’ll be linked financially to the other person. This means that you can be jointly credit scored, and their credit history can have an impact on yours. You’ll also be joint 50/50 owners of whatever funds are in the account, so make sure you really trust anyone you’re planning to open a joint account with. Learn more about joint bank accounts.

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Sources

Was this content helpful to you?

Thank you for your feedback!

To make sure you get accurate and helpful information, this guide has been reviewed by

Rachel Wait, a member of Finder's

Editorial Review Board.

Kate Steere is an editor and money expert at Finder, specialising in banking, savings and fintech. She has previously written for The Motley Fool UK and Fitch Solutions, where she covered a wide range of personal finance topics and kept a close eye on market trends. Kate has a Bachelor of Arts in Modern History from the University of East Anglia. When not working, she can usually be found curled up with a good book or heading out for a run.

See full bio

Kate's expertise

Kate

has written

182

Finder guides across topics including:

Jason is a writer and editor. He worked as a senior subeditor for Finder for 5 years and in that time became familiar with a wide range of financial products and services. Before that, he worked for Australian Associated Press. He has a BA from Macquarie University in Australia. Jason loves to help other people find new ways to save money.

See full bio

Thinking about using Starling or Monzo? Compare both side by side using our table. We look at their costs, foreign transaction fees, card delivery speed and app features.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.