When it comes to choosing a credit card, debit card or prepaid card, you usually have the option of a Visa or a Mastercard. These are the two major card-processing companies used in the UK, followed by American Express.

Each Visa or Mastercard credit card is independently issued by a bank or other provider that also offers a range of features and services to customers across their networks. Most banks and card providers don’t give you a choice between Mastercard or Visa, so you’ll probably find it more relevant to your decision-making process to focus on the features offered by a particular card and the provider in general.

Generally, there are very little differences between the two networks and you will rarely deal with Visa or Mastercard directly (it would usually be through your card provider). However, if you’re trying to decide between these two options, here we compare Visa and Mastercard features side-by-side to see how they stack up.

What are Visa and Mastercard?

Visa and Mastercard provide the technology and networks required for processing card payments. So if you buy an item with a Visa credit card, for example, the transaction will be processed on Visa’s network from the shop to the relevant bank or banks (including your own). Similarly, Mastercard credit card transactions are processed via the Mastercard payment network. These two companies are the largest card processors in the world, and their cards are accepted at millions of shops and other providers all over the globe. Generally, you will find most shops accept both Visa and Mastercard payments.

Individual banks and other financial institutions issue Visa or Mastercard credit cards based on the payment processing network they want to use. Whichever network is used, the company’s logo will be visible on the card. A few providers even offer both Visa and Mastercard options. In regards to specific card features, such as interest rates, annual fees, rewards programmes and introductory offers, it is ultimately the card issuer that decides what will be available on specific cards.

Traditionally, Visa has dominated the UK debit card market, but this is set to change. Santander and TSB will start issuing Mastercard debit cards in 2019, joining Virgin Money, Citibank, Clydesdale Bank, Yorkshire Bank and Metro Bank, which already provide Mastercard debit cards.

Compare Mastercard Credit Cards by type

Comparison is ordered by representative APR with affiliated products shown first.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

What features and services do Visa and Mastercard offer?

Visa and Mastercard offer a wide range of features and services that banks and other providers can choose to include on their different cards. These include:

Contactless payments. Credit cards with Visa or Mastercard contactless functionality allow you to make payments by tapping your card against a compatible reader. You don’t even need to enter a PIN if the transaction is worth less than £45. Contactless Visa and Mastercard credit cards can also be added to compatible mobile payment services that allow you to use your phone for purchases.

Premium cards. Visa and Mastercard both provide a range of standard and premium card options, such as Visa Platinum credit cards or World Mastercard cards. Gold and Platinum features vary based on the credit card provider but could include concierge services, global customer assistance, complimentary insurance and offers and privileges at a range of stores, hotels and restaurants.

Exclusive offers. The Mastercard Priceless Cities programme provides exclusive entertainment, dining, travel and shopping offers and experiences to customers with a Mastercard. Some premium cards may also offer access to even more exclusive packages. Meanwhile, smaller rival American Express has a benefits programme called American Express Experiences.

Online payment. Visa Checkout allows customers to shop online with participating retailers using a simple sign-in, which allows them to securely store shipping and payment details. Meanwhile, Mastercard offers a similar system with their digital wallet Masterpass.

Global security services. The Visa Global Customer Card and Mastercard Global Service support hotlines provide assistance if your card is lost or stolen, or if you have enquiries about your account. These services are available 24/7 from anywhere in the world. Alternatively, you can call your bank or card provider.

Online shopping protection. Both Visa and Mastercard offer programs that add another layer of security to online card payments. Verified by Visa and Mastercard SecureCode are optional services that some providers may offer when you use your credit card online.

How can I compare Visa and Mastercard credit cards?

Visa and Mastercard both offer worldwide acceptance and a similar range of features and services. Again, the features available may still depend on the actual card issuer. So rather than only comparing these two companies, it’s better to look at the specific details of each card you’re considering. This could include:

Annual fees. Most credit cards charge an annual fee, which could be as low as £25 for a basic card, or upwards of £450 for a premium option. The credit card issuer determines the annual fee based on the features available, with more perks usually equalling a higher cost. For this reason, Visa Platinum, Signature and Infinite cards, as well as World Mastercards, typically have higher fees because of the premium features they offer.

Interest rates. Standard credit card interest rates can significantly increase the cost of the card you choose, so it’s important to look at both the purchase rate and the cash advance rate for each card you compare. Again, these rates are set by the issuer but tend to be higher for more premium products.

Rewards. There is a wide range of Visa and Mastercard credit cards that are linked to rewards programs and frequent flyer programs. These products offer you points per £1 spent on purchases and usually include other additional features as well as higher annual fees. When comparing rewards cards, consider the earn rate, the type of rewards available and your average card spending so that you can decide if the annual fee will be worth it.

Dual accounts. Generally, rewards credit cards processed on the American Express payment network offer a more competitive points earn rate than Visa or Mastercard options. As Visa and Mastercard have more extensive networks, though, you can use them in a wider range of locations. As a result of these different features, some card issuers offer accounts that come with both an Amex card and a Visa or Mastercard to help you maximise your rewards.

Interest-free days. If you pay your balance in full by the statement due date, most credit cards will offer an interest-free period, such as “up to 44 days interest free.” This feature allows you to make purchases while avoiding interest. It’s worth noting that interest-free days are not applicable for cash advances, balance transfers or if you don’t pay your balance in full by the due date on your statement.

Complimentary extras. Credit card providers may offer a range of additional perks, including complimentary insurance, concierge services, airport lounge access and flight vouchers. These benefits can add value to the card you choose if you use them, and vary significantly between products.

Introductory offers. Credit card providers regularly offer new customers additional perks for a limited time, such as bonus points, 0% balance transfer interest rates or 0% purchase rates. These features are available for an introductory period and can add short-term value to the card you choose.

Security services. In addition to the security services offered by Visa and Mastercard, credit card providers may offer 24/7 fraud-monitoring services, daily transaction limits or even the ability to temporarily lock your card if you have misplaced it. All credit cards are chip-and-PIN products, which offer superior security for in-person payments.

While it’s definitely more important to compare individual credit card features when looking for a new card, if you’re still interested in the whole Visa vs Mastercard debate, here are some other details to consider.

The history of Mastercard

Mastercard credit cards were originally developed in the US in 1966. This was during the early days of modern credit and charge cards, and there was a huge demand for products that could be used to make payments at a wide range of businesses. This led to the formation of the Interbank Card Association (ICA) and the MasterCharge card.

The Mastercard brand officially came into effect in 1979 as an evolution of this card payment network. It continued to grow as a major credit card brand and officially offered an IPO through the New York Stock Exchange in 2006 (trading as MA). Along with Visa, Mastercard has been at the forefront of credit card technology developments for security and card acceptance, including the implementation of EMV-chip credit cards and contactless payments.

The history of Visa

Visa’s history dates back to 1958 when the Bank of America launched the BankAmericard. This was the first mass-marketed credit card program and it quickly grew in popularity.

By the 1970s, BankAmericard was an independent entity and went on to take the name Visa. Visa then launched VisaNet, which was the first electronic payment authorisation, clearing, and settlement system in the world. It has continued to grow as a card payment processor since then and, like Mastercard, has been at the forefront of technologies including chip cards and contactless payments.

How do Visa and Mastercard make money?

Visa and Mastercard’s profits primarily come from the entities that use their services, such as banks and shops. Some of their sources of revenue include:

Card issuer fees. Both Mastercard and Visa charge financial institutions service fees for the use of their payment systems.

Bank settlement fees. Credit card issuers pay this fee at the time of settlement of payments.

Overseas fees. Mastercard and Visa charge issuers a fee for processing payments made in a foreign currency. These charges are often passed onto credit card customers in the form of a foreign currency or international transaction fee.

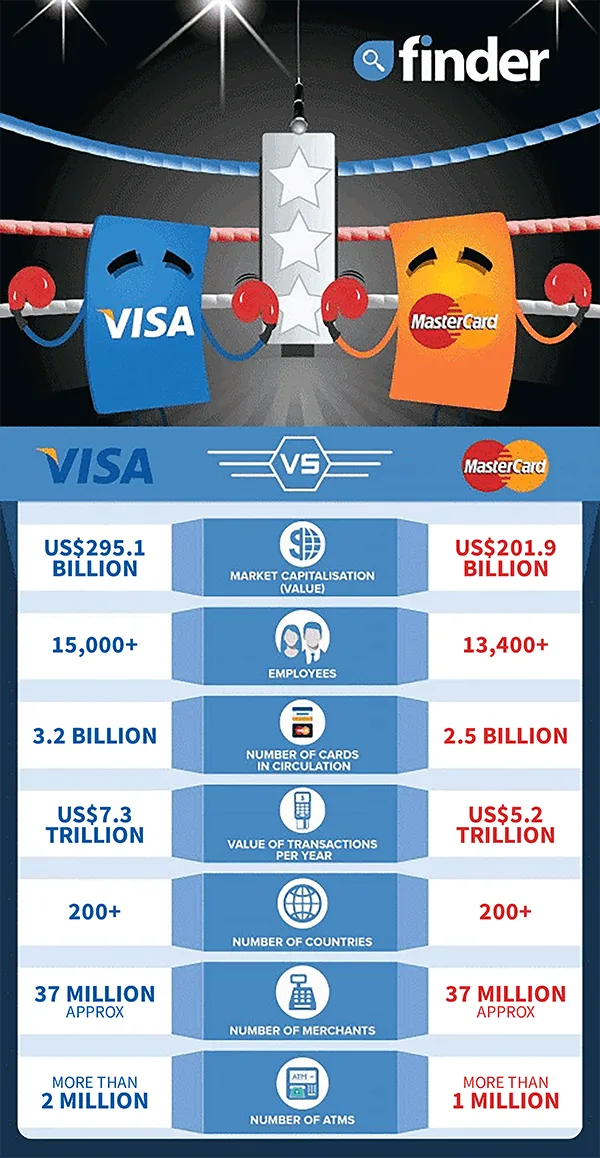

Visa and Mastercard compared

Visa

Mastercard

Market capitalisation (value)1

US$516.76 billion

US$390.40 billion

Employees2

15,000+

13,400+

Number of cards in circulation

3.2 billion3

2.5 billion4

Value of transactions per year

US$7.3 trillion5

US$5.2 trillion6

Winner?

The details above show that Visa is by far the bigger company. However, in recent years, Mastercard has substantially increased its market share, bridging the gap between these two credit card giants.

Visa

Mastercard

Number of countries and territories

200+

210+

Number of merchants5

37 million (approx)

37 million (approx)

Number of ATMs

More than 2 million7

More than 1 million8

Winner?

A tie

A tie

1 and 2 At October 2018, reported by Forbes3 Visa Annual Report 2017 4 Mastercard Incorporated Reports (October 2018) 5 Visa Annual Report 2017 6 Mastercard Sustainability Report 2017 7 Visa website (November 2018) 8 Mastercard Global ATM Locator (October 2018)

In terms of card acceptance, the table above shows that the two schemes are roughly the same. Although Visa boasts a wider ATM network than Mastercard, neither of them state a specific number of ATMs and acceptance may also depend on your card issuer. As these details are also published online with no date to them, it’s difficult to gauge how accurate they are, so we’ve called it a draw. As always, when choosing a card, make sure to weigh up all of its fees, features and benefits rather than just looking at which one is a Visa or a Mastercard.

While there are differences between Mastercard and Visa at a corporate level, the variations are relatively minor when it comes to using a credit card processed by one of the two companies. In general, you’re better off focusing on features such as the interest rate, annual fee and complimentary extras available when comparing credit cards so that you can find one that suits your needs.

Frequently asked questions

Visa is the larger of these two companies as of October 2018, with a 12-month market capitalisation of US$295.1 billion and 15,000 employees. In comparison, Mastercard has a market capitalisation of US$201.9 billion and over 13,400 employees.

Both cards are accepted in over 200 countries and territories around the world.

Yes. Eligibility requirements vary based on the credit card provider, but generally include the following:

You must be over 18 years of age

You must be a resident of the UK

You must have a good credit history

You might also have to meet minimum income requirements, depending on the card.

Sources

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Emily Herring is a Publisher at Finder specialising in credit-based products including credit cards and business and personal loans. Emily has recently joined the Investments team. She has a Masters in Creative Writing & Publishing and a Bachelor of Arts in Communication & Media.

See full bio

Emily's expertise

Emily

has written

101

Finder guides across topics including:

Discover how to supercharge your points through everyday spending – plus a few ways to redeem them with the American Express® Preferred Rewards Gold Credit Card. (Paid content)

Buy now and pay interest later with a 0% purchase credit card. Compare current offers with 0% p.a. on purchases.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.