See cards you're likely to get

Check your chances of being accepted before you apply

It's simple, fast and free

It won't affect your credit score

We currently don't have that product, but here are others to consider:

How we picked theseTo make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

Read the full methodologyApproval for any credit card depends on your status. The representative APRs shown represent the interest rate offered to most successful applicants. Depending on your personal circumstances, the APR you're offered may be higher, or you may not be offered credit at all. Fees and rates are subject to change without notice. It's always wise to check the terms of any deal before you borrow. Most of the data in Finder's comparison tables is provided by Defaqto.

A 0% balance transfer enables you to move your current credit card debt to a new card that charges zero interest on your balance during the promotional period. The duration of this interest-free period varies by card, with some offering up to 40 months of no interest on balance transfers. After the promotional period ends, the balance transfer interest rate reverts to the card’s standard interest rate.

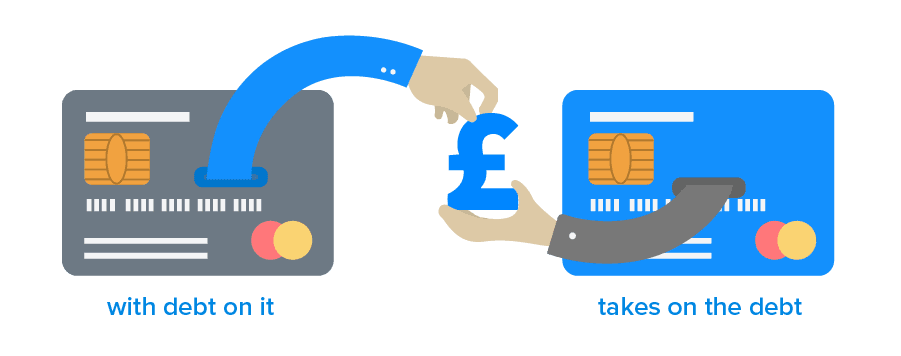

A 0% balance transfer credit card gives you the option to transfer an existing high-interest debt to a new card that offers a promotional 0% interest rate. You can initiate the balance transfer request during the application process for the new card. If your application is approved, your new credit card provider will pay off the outstanding balance on your old card and move it to your new account. Whilst the 0% promotional balance transfer offer is in place, you won’t accrue any additional interest as you repay your debt.

This means you can clear your balance without collecting more debt for a promotional period of up to 40 months depending on the card. Not only can you clear your debt faster, but you can save hundreds or thousands of pounds on interest charges at the same time.

If you have a credit card debt of £1,000 and you make £100 repayments per month, a balance transfer offer can help you regain control of your finances and save:

| Normal credit card without balance transfer offer | 0% balance transfer credit card | |

|---|---|---|

| Interest rate | 20% p.a. | 0% p.a. |

| Months required to repay | 12 months | 10 months |

| Interest paid over this period | £200 | £0 |

As you can see in the example above, not only can you save £200 in interest costs, but you’ll also repay your debt faster.

This example assumes that the cardholder cleared the debt before the promotional offer finished. Once the 0% balance transfer period offer finishes, a higher standard interest rate will apply. So if you’re unable to pay off your debt before the introductory offer ends, your remaining debt will be charged the standard variable interest rate for balance transfers.

Here are the most important factors you should keep in mind to find a 0% balance transfer card to consolidate your debt:

While you don’t pay interest on the debt you move to a 0% balance transfer card, there are a number of other fees you should be aware of before you apply. Some of the most common costs include:

Depending on the 0% balance transfer card you choose, other fees and charges may also apply in some circumstances. Make sure you check the standard terms and conditions for individual cards before you apply.

These simple steps will help you find and apply for a 0% balance transfer offer that fits your budget and your needs.

Consider how much debt you want to transfer, and how long you think it will take you to pay it off so that you know what kind of offers will help you achieve your goal.

Look at all the different features and types of balance transfer offers, weighing them up based on the length of the 0% balance transfer offer, the amount you have to repay and the fees and features that come with the card. You should also make sure you meet the eligibility requirements before you apply.

You will need to provide personal details including your full name, date of birth, street address, driver’s licence number and/or passport number. Keep these documents handy and submit copies as requested by the credit card issuer.

There is a section of the credit card application that asks for details of any balance transfer requests. You will need to fill this out with information including the current credit card company, the account number and the total amount of debt you want to transfer to the new card.

You should get a response within 60 seconds of applying. You may be required to provide supporting documentation as part of this process. When you receive your card and activate it, your new provider will process the balance transfer from your old card to the new one. If you’d like to cancel your old credit card, contact your old bank directly to request for the account to be closed.

Applying for a 0% balance transfer can be a daunting task. We have answered the most popular questions from our users about applying for and using a 0% balance transfer credit card here.

Find out how you could improve your credit score and earn rewards with the 2 credit cards from Yonder.

We look at the average APR on credit cards in the UK and how credit card interest rates have changed over time.

Find out how to spread your purchases over 3, 6 or 12 months with Monzo Flex.

What is the average credit score in the UK and how many Brits are estimated to be ‘credit invisible’?

Let Finder check your chances of getting approved for a range of popular UK credit cards.

Learn how to approach getting a credit card as a young adult with a limited credit history.

People collecting a pension are eligible to apply for credit cards. Learn more about the application requirements and documents you’ll need to apply today.

Frequent John Lewis and Waitrose shoppers can discover how this loyalty-point-earning Mastercard compares.

Find out which credit cards offer the best earn rates per £1 and start collecting Nectar points every time you use your card.

Looking for a balance transfer, 0% purchase or platinum card? Compare the range of credit cards on offer from Post Office Money.