Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

How to calculate your loan-to-value ratio (LTV)

Know how much equity you have in your home.

A loan-to-value ratio is the size of a loan compared to the value of a property expressed as a percentage.

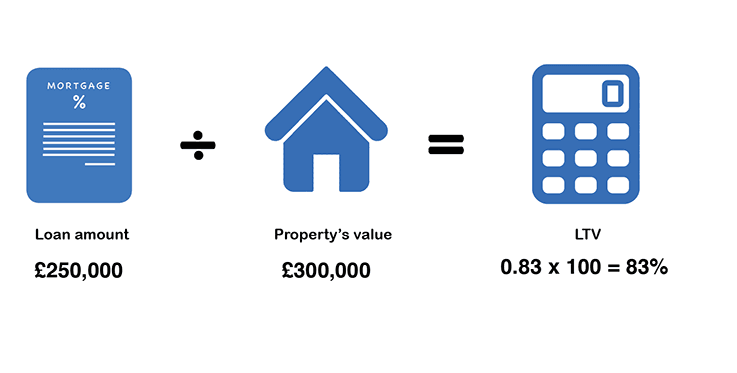

You can find this out by dividing the amount you’ll need to borrow to purchase a property by the property’s value.

If you buy a property for £300,000 and need a loan amount of £250,000 to purchase it, your LTV ratio will be 0.83, or 83% when expressed as a percentage. Scroll down to see this equation used in a common example.

LTVs are important when it comes to getting a mortgage. Generally, the lower the LTV, the lower the risk you present to your lender. Also, lower LTVs often qualify for cheaper interest rates. Generally, a loan of 80% or less is recommended, as borrowing more leads to more fees and charges and the possibility of higher interest rates.

To work out your property’s value, a lender will order an independent property valuation. The loan amount is simply the amount you need to borrow to purchase the property.

Both your property value and your loan amount can rise and fall. Property values fluctuate with the market value of the property, whereas the loan amount can rise if a borrower borrows more. Making principal repayments reduces your loan amount, as does making additional repayments.

The size of a deposit (or existing equity when remortgaging) is what determines an LTV. The larger the deposit saved compared to a property value, the lower the LTV.

David has saved up £35,000 to use as a deposit and he wants to know the maximum price of a property he can purchase, with the lowest interest rates and affordable repayments. His £35,000 deposit therefore has to represent at least 20% of the value of the property. To calculate an 80% LTV ratio, David multiplies his deposit amount by five, which works out to be £35,000 x 5 – giving him an upper property price limit of £175,000.

David can’t spend more than £175,000 on buying a property. With a property price of this value, his loan would be £140,000 (£175,000-£35,000).

| Amount | Percent | |

| Property value | £175 000 | 100% |

| Deposit | £35 000 | 20% |

| Loan Amount | £140 000 | 80% |

* This is a fictional, but realistic, example.

You can calculate your maximum budget for a property based on the average maximum LTV accepted and the amount you have saved up for a deposit. While this in no way guarantees that you will be approved for all the mortgages you apply for, it is a good starting point.

Let’s assume that you have saved up £35,000 to use as a deposit and you’re hoping to take out a loan with no higher than 80% LTV, so your £35,000 has to represent at least 20% of the value of the property. Using a mortgage calculator, we see that the value of the property should not exceed £175,000 and the maximum mortgage you can get is £140,000.

Of course, just because your LTV is within acceptable bounds, there’s no guarantee that your application will be approved, as there are many other variables involved including your financial position.

In certain situations, you can obtain a loan with a little or no deposit but you need to have a guarantor. With guarantor mortgages, you can sometimes obtain as much as 100% of the property’s value but remember that you are risking someone else’s home in the process, so make absolutely certain you are in a financial position to make the repayments on time. You can use an online mortgage calculator to help you work out how much your repayments will be to ensure you can afford it.

If you are struggling to save up a deposit for your first house, you could potentially borrow up to 95% of the value. This is a high LTV mortgage. Check out our guide on getting a mortgage with just a 5% deposit.

When buying a home, your LTV may influence:

| Response | 55+ | 45-54 | 35-44 | 25-34 | 16-24 |

|---|---|---|---|---|---|

| Somewhat agree | 29.36% | 28.65% | 35.17% | 33.54% | 33.98% |

| Neither agree nor disagree | 27.15% | 28.07% | 22.46% | 21.74% | 24.27% |

| Strongly disagree | 20.22% | 15.2% | 14.41% | 11.8% | 9.71% |

| Somewhat disagree | 15.51% | 18.13% | 17.37% | 18.01% | 9.71% |

| Strongly agree | 7.76% | 9.94% | 10.59% | 14.91% | 22.33% |

Learn more about Simply Adverse, a mortgage broker, which specialises in finding the best available deal for those with a bad credit score.

Here’s everything you need to know about fees when exiting a mortgage.

Everything you need to know about joint mortgages and buying a property with your parents.

How to purchase a buy-to-let property as a limited company.

You should be aware of how being a guarantor could influence your ability to qualify for a mortgage.

Learn how a personal loan could affect your eligibility for a mortgage.

Find out if financing a car affects your mortgage application.

They have been popular in other countries for some time, and now 15 year fixed rate mortgages are available in the UK.

Plenty of lenders will let you borrow 95% of a property’s value.

Looking for a mortgage with TSB? Compare different rates and mortgage types, and find out how to get the right home loan for you.