Gross profit: £60,000

House flipping: How to successfully do property flipping in the UK

What is property flipping and how can you make money doing it? Here’s what you need to know.

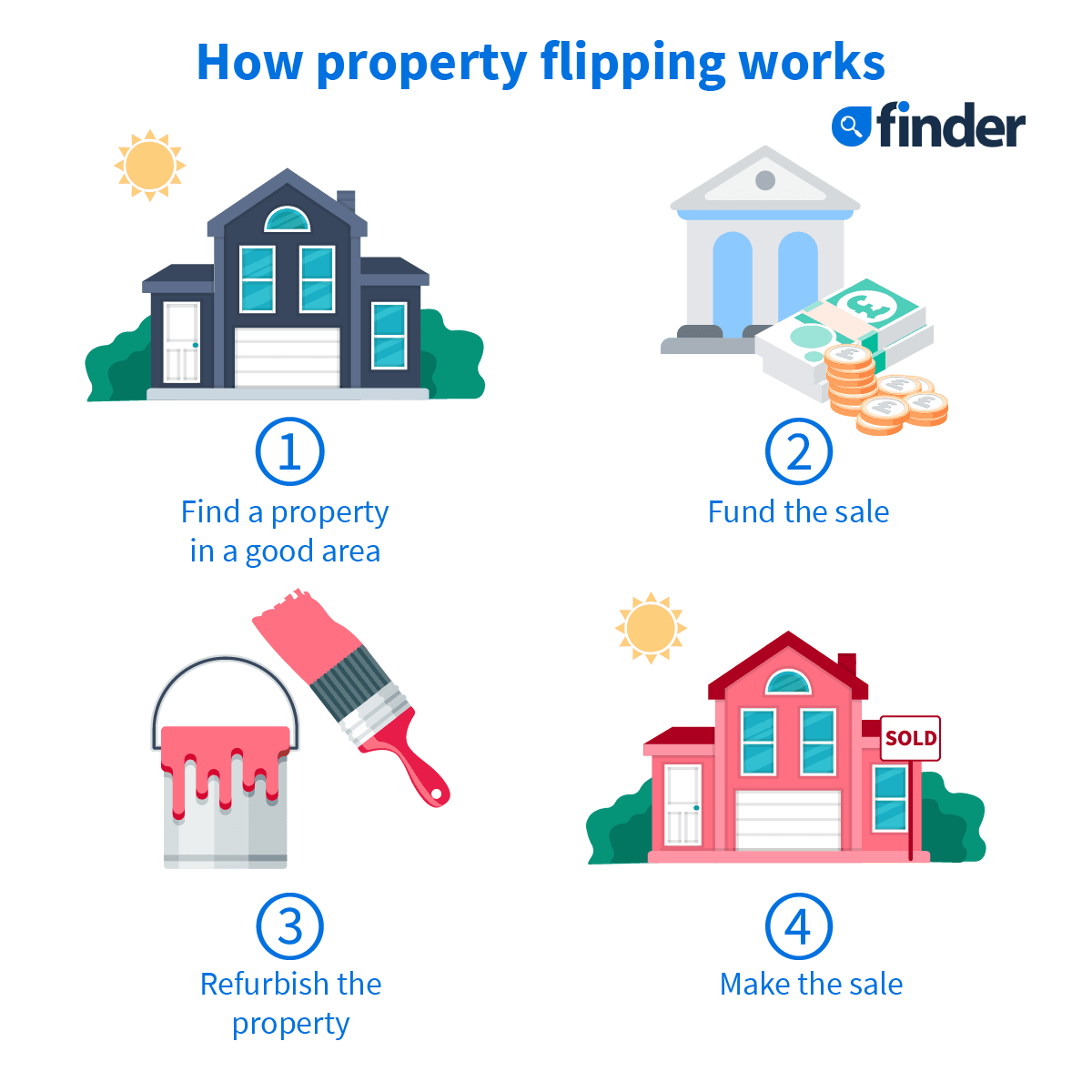

Property flipping is when a property is bought and then sold again after a short period of time – usually within a year – with the aim of making money. In times when house prices are rising rapidly, you may be able to make money without doing anything to the property, but when prices are rising more slowly you’ll need to renovate and improve it to boost its value.

Research by estate agent Hamptons International shows that the popularly of house flipping (defined as homes sold more than once within a year) has fallen dramatically as house price inflation has slowed. At its peak in 2004, 60,340 homes were flipped in England and Wales compared to just 18,630 in 2018 – a 69% drop. As a proportion of all homes sold, 4.8% were flipped in 2004 versus 2.1% in 2018.

Hamptons International said that house prices rose by 13% on average between 2000 and 2007, which explains the popularity of house flipping during this period, but growth slowed following the financial crisis in 2008 and the Brexit vote in 2016. According to Nationwide, in 2019 UK house prices rose by just 1.4% on average (some regions actually experienced price falls) so flipping property is much riskier than it used to be.

If you want to get into property developing either as a sideline or a full-time career move, then property flipping is the opportunity to generate an income by refurbishing a property and selling it on at a profit.

Or, you may decide to view it as a one-off project, using some savings or an inheritance to snap up a bargain property and generate a return on your money by selling the property for a higher price after completing the renovations.

Alternatively, your individual circumstances may inadvertently lend themselves to property flipping at that particular time in your life. Perhaps you know you’ll only be living in a certain area for a year or less, so will decide to buy a run-down property, live in it while you do it up, then sell it on when you’re off to pastures now.

Since the current level of house price inflation isn’t enough to make you money on a property in itself, especially once you factor in the cost of buying, owning and selling it, you’ll need to renovate the property to make flipping worthwhile and then sell it for the best price possible – showing it with furniture and accessories will make it more saleable for example.

You can maximise your profits by buying a property for less than its market value in the first place – consider buying a repossessed property or buying at auction to try and get a bargain. Also ask estate agents if they have any properties on their books where a quick sale is needed, such as the owners are getting divorced or the property is about to be repossessed, as you may be able to get it for less.

Remember that the fees you’ll have to pay will be significant. You’ll pay stamp duty if you’re buying a property for more than £125,000 and if you already own a property you’ll have to pay 3% extra too. You’ll also have to spend another few thousand on legal, survey and other fees and will pay a minimum of 1% plus VAT in estate agents’ fees when you sell it, which equates to £3,600 if the sale price is £300,000.

If you don’t already have the cash available to buy and renovate the property there will be finance costs and you will have to pay for council tax, utilities and insurance. You could end up spending £20,000 on top of the cost of the renovations, which will take a big chunk out of your profit.

Also bear in mind that you will have to pay capital gains tax (CGT) on your profits when you sell if you’re not doing it as part of a business. This could be up to 28% of your “gain” (depending on which income tax bracket you’re in), worked out as how much you sold the property for minus how much you bought it for, how much you spent in fees and on improving the property and your annual CGT-free allowance (£12,000 in the 2019/20 tax year). There are however some ways one can avoid capital gains tax when selling property.

So, it’s essential to do your sums to work out all the costs involved and the potential profit before you buy anything. A minimum return on your investment of 20% is a healthy amount to aim for.

| Purchase price | £250,000 |

|---|---|

| General Costs (Refurbishment etc) | £30,000 |

| Buying/selling costs | £15,000 |

| Selling price | £350,000 |

| Profit | £55,000 |

If you’re not going to be living in the property you won’t be able to take out a residential mortgage to buy it. These are also designed to offer longer-term funding than you will need if you’re flipping the property within a year. And if you won’t be renting it out you won’t be able to get a buy-to-let mortgage either. When you’re taking out any kind of mortgage, the property needs to be habitable, which it might not be if you’re planning major works.

The best option if you’re buying to sell is to take out short-term finance (also known as a bridging loan or a buy-to-sell mortgage) specifically designed for this purpose. It can be arranged more quickly than a mortgage but the interest charged is higher.

You’ll still need cash to pay a deposit of at least 20% of the purchase price and loan fees, for which you could use savings or release equity from your home. You can either make interest payments each month or roll up the interest so that you pay it off with the loan once the property is sold.

Speak to an independent mortgage adviser for advice on your options or compare bridging rates online.

It’s essential to choose the right property at the right price to have a chance of making money. The more it can be improved the better, although some major renovations will add more value than others and you need to avoid any major issues that will be costly to put right, so it’s important to get a building survey done on the property.

Look at house price data to see where they are increasing the most, although bear in mind that this can vary hugely within individual regions and cities. Speak to estate agents to get a more localised view of which areas are likely to go up in value and what buyers are looking for as it’s essential to cater for the right market. It’s also worth finding out about areas that are being invested in, which could mean they’re up-and-coming.

You can look at the Zoopla website to get estimates of how much individual properties in an area are worth when you’re deciding how much you should pay. It also tells you how many bedrooms and bathrooms they have, which will give you an idea of how this affects the value.

Depending on the area, a two- or three-bedroom house is likely to have wider appeal than a flat and have more scope for adding value. You should also consider local transport and amenities, the crime rate and whether there are good schools nearby if you’re targeting families. It’s better to target buyers who will live in the property and want somewhere that doesn’t need any work rather than investors who may want to pay under market value.

The more you spend on refurbishing the property the more you will have to sell it for to make money, so it’s important not to spend over the odds. Relatively cheap improvements, such as redecorating, replacing old flooring, making the front of the house look more appealing by tidying up the front garden and repainting the front door, and repainting old kitchen units rather than replacing them can go a long way towards boosting its value.

You will save money if you can do some of the work yourself, although you should get the experts in for more complex jobs such as electrical work and plumbing.

If you’re using tradespeople you should get multiple quotes before deciding who to use – ideally this is something you should do before you buy the property so you know how much you will have to spend on it. You can either project manage the refurbishment and get the individual tradespeople in yourself, which will be cheaper but require more time and effort, or get a contractor to do it all for you.

When you’re thinking about making more expensive changes, it’s essential to do your homework to make sure the outlay and extra time will be worth it. Adding an extra room by converting the loft or building an extension will almost always boost your profits as long as it’s something that suits your target market. We explore refurbishment loans in greater detail here.

Property flipping can present an opportunity to turn a quick profit, but make sure you’re aware of all the costs and risks involved before you attempt it for the first time. Some people flip property as a one-off scenario, while others have turned it into a full-time career. Even if you do become proficient at it over a long period of time, be mindful that a sudden or unexpected downturn in the housing market could hamper your chances of success at any given point.

Finder data suggests that men aged 35-44 are most likely to be researching this topic.

| Response | Male (%) | Female (%) |

|---|---|---|

| 65+ | 3.70% | 2.58% |

| 55-64 | 7.18% | 3.70% |

| 45-54 | 9.32% | 5.84% |

| 35-44 | 16.16% | 8.42% |

| 25-34 | 14.59% | 11.78% |

| 18-24 | 9.65% | 7.07% |

Everything you need to know about commercial bridging loans. We look at when they’re useful, how they work and what to be aware of before taking one out.

In-depth guide to bridging loans if you have had credit problems in the past, including what lenders are willing to overlook and which are the most important factors.

Complete guide to buying at auction with a mortgage. Find out which types of properties could be unmortgageable and how to get your finances in place before the auction.

How to buy a repossessed property and what the risks and benefits are. Plus, where to look for properties, buying at auction and issues to look out for.

The complete guide to property auctions, including how the process works and the checks to make on the properties you want to bid on.

Discover if a short term mortgage is a right option for you depending on your circumstances.

Buy-to-sell mortgages (also called bridging loans) are designed for buyers who are looking to sell on a property within a relatively short time-frame. Read our guide and compare rates.

If you haven’t sold your house yet, but want to buy your next one before the sale is completed, a bridging loan may be able to help.