Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

Offset mortgages

An offset account could save you thousands and shave years off your mortgage.

Offset mortgages are often used as a way to save money. They are used to help reduce your monthly payments or shorten the term to enable you to be mortgage-free sooner.

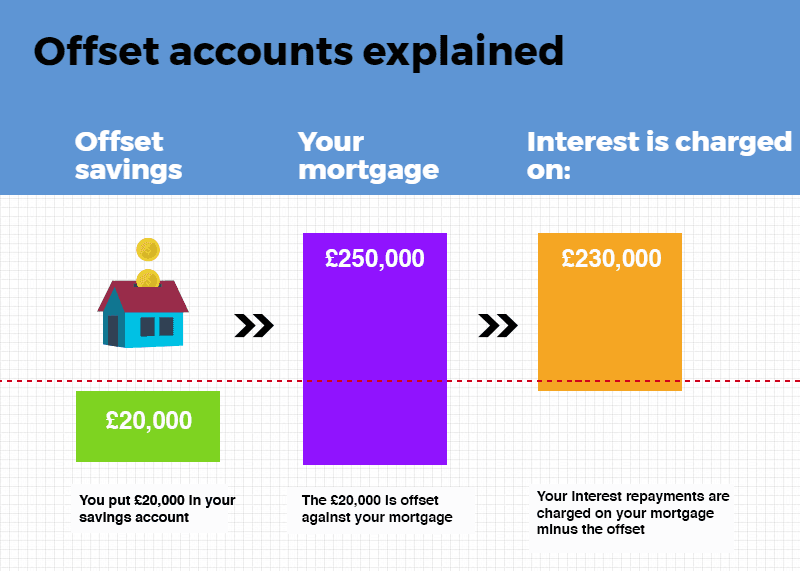

An offset account is a transaction account attached to a mortgage. The balance of a 100% offset account is taken away from the principal remaining on the mortgage for interest calculation.

In this hypothetical situation, interest is applied to £230,000 instead of the full £250,000 owed. As savings grow, the amount saved on interest also grows. Effectively, this reduces the amount of interest charged over the life of the mortgage.

An offset account may save you interest and cut the length of a mortgage. It will work best for people who can maintain a decent balance in their offset account and contribute further to it over time. It is worth shopping around, as offset accounts can differ in inclusions and fees.

Traditionally, mortgages with offset accounts would either attract a higher interest rate or higher fees and sometimes both. However, with the emergence of smaller online lenders, many mortgages are feature-packed with market leading rates. Major lenders still tend to charge a premium for offset accounts, so it is worth shopping around.

Yes, there are 100% offset accounts and partial offset accounts:

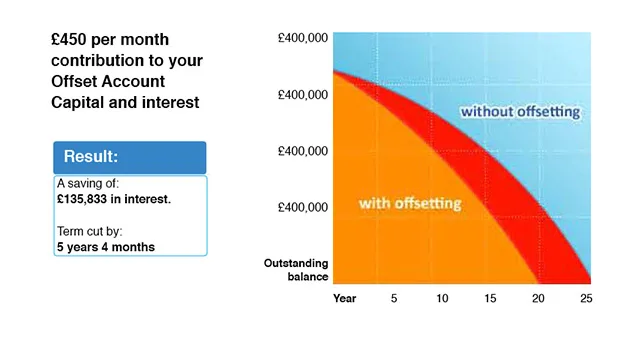

From this example, taking the mortgage with an offset account saves a whopping £136,000 over the life of the mortgage. It also reduces the term of the mortgage from 25 years to 19 years and 8 months. Owning a home outright, debt free, is a goal that is well worth fast-tracking. Especially as first-time buyers are waiting longer to plunge into the property market.

Some offset accounts charge fees on standard transactions. It is well worth putting the research in as to whether the mortgage you’re applying for has a transaction account that will end up costing you money.

| Response | Yorkshire and the Humber | West Midlands | Wales | South West | South East | Scotland | Northern Ireland | North West | North East | Greater London | East of England | East Midlands |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| No | 45.88% | 39.13% | 46.97% | 52.17% | 45.03% | 47.37% | 66.67% | 51.24% | 57.14% | 27.78% | 55.17% | 52.27% |

| Yes | 29.41% | 33.04% | 22.73% | 20.29% | 33.11% | 34.21% | 25% | 21.49% | 14.29% | 48.15% | 21.84% | 28.41% |

| Not sure | 24.71% | 27.83% | 30.3% | 27.54% | 21.85% | 18.42% | 8.33% | 27.27% | 28.57% | 24.07% | 22.99% | 19.32% |

Habito and L&C go head-to-head as we outline the differences between these free mortgage broker/adviser services.

Official data shows that 63% of people in England and Wales own their home. We look at the latest home ownership statistics in the UK.

We look at the latest first-time buyer statistics to see how difficult it is to get your foot on the property ladder in the UK.

From the average mortgage payment and debt to how many outstanding mortgages there are, we explore the latest mortgage statistics in the UK.

Find out what a discount mortgage is and whether it’s right for you.

Discover if you need a mortgage broker, find out how one can help you and learn how to find the best mortgage broker for your situation.

A comprehensive six-part guide covering every step of the home buying journey from early research to getting the keys to your new home.

Our review reveals everything you need to know about Habito.

Want to get a mortgage with as little as a 5% deposit? Here’s how you can do it.

Find out about L&C mortgage brokers.