Habito and L&C are two of the UK’s biggest and best-known mortgage brokers/advisers. They’ve probably got more in common than they have differences.

Both of these services sift through a huge panel of mortgage lenders to find you the best deal based on your circumstances and preferences, and both of them offer real human advice along the way. They’re also both fee-free – making their money through kick-backs from the mortgage providers.

Habito vs L&C: Our Verdict

They’re both very good. Choose the one that best suits your communication style.

Habito’s been acquired by Monzo, and that’s a good fit (not just because they’re both silly names): you get a beautiful digital user experience and everything’s instant and intuitive. You don’t need to schedule a phone call in advance to speak to an expert, you just start chatting with one in live chat… provided it’s within live chat hours. Maybe the names aren’t actually all that silly: L&C’s a little bit more old-school and phoney (as in, they like to use the phone – they’re perfectly authentic), but the fact that you can speak to them at weekends is a huuuuge plus.

I scroll socials with the sound turned off, whenever I fancy it, and that might make me more of a Habito person. Sometimes I wish I was more of an L&C person, who cleared the decks in advance to really focus on solving a problem.

At the end of both road tests, I ended up being offered the exact same rate on a 2-year fixed-rate deal. If the end destination was ultimately the same, then I slightly preferred the Habito journey.

Finder score

9.5Excellent

8.7Great

Fee-free service

Panel of lenders

95+

90+

Availability hours

9am-9pm Mon-Thurs and 9am-5pm Fridays

9am-8pm Mon-Thurs, 9am-5.30pm Fridays, 9am-5pm Saturdays and 10am-4pm Sundays

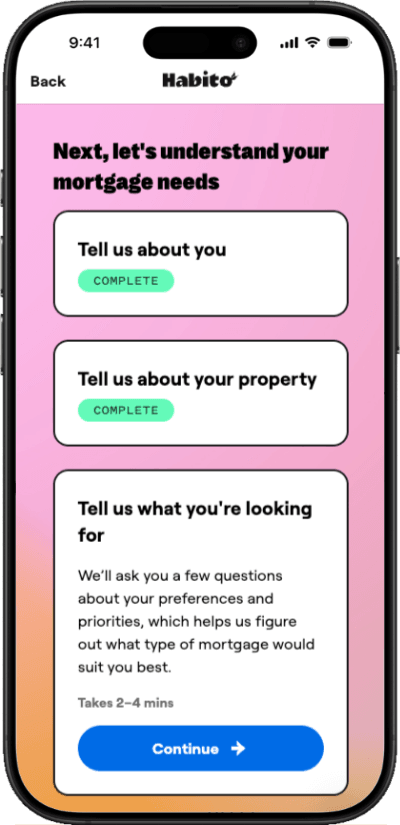

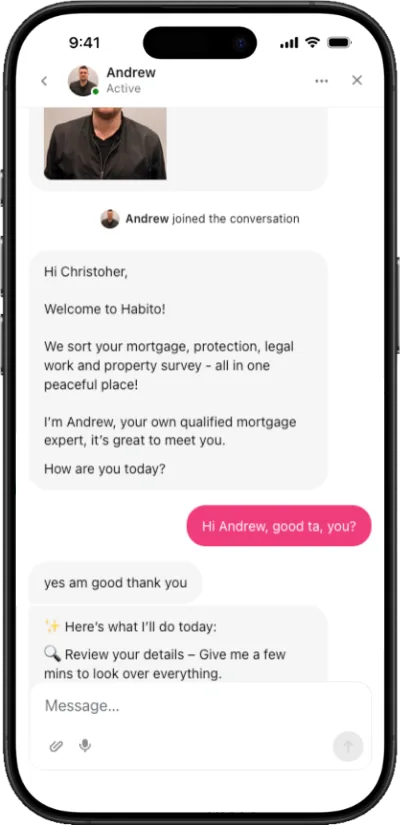

Both Habito and L&C start off with a form. Habito’s is a little more long-winded, but at the end you’re straight into live chat with an expert who’s probably got everything they need to start showing you specific deals from specific lenders.

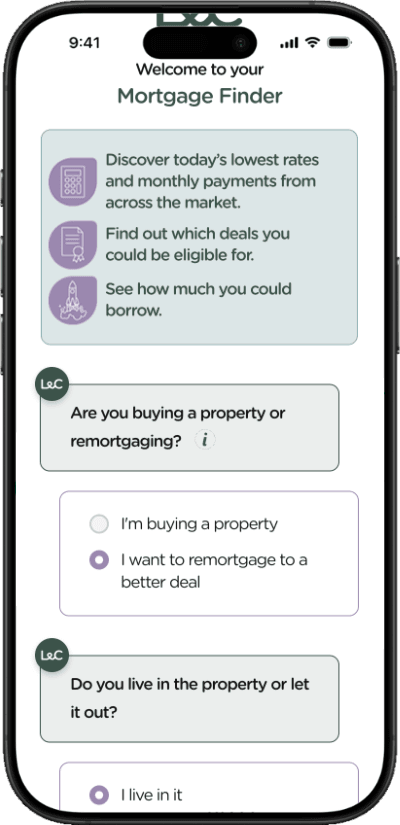

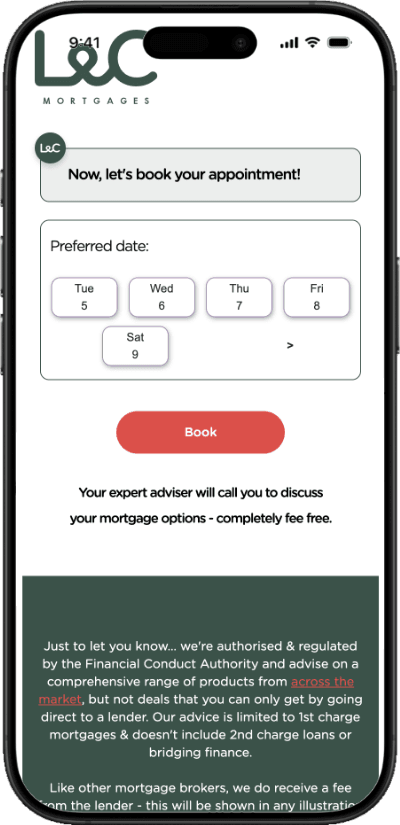

L&C’s form is shorter, and you can leave fields blank, but completion leads you to a “Now book an appointment” screen.

Since both forms take over 5 minutes to complete, I was a bit miffed when I realised I would then have to wait until my appointment to speak to an L&C expert. That said, there was availability the same day, which was impressive.

With Habito, you fill out a fairly detailed on-boarding form then get straight into live-chatting with your assigned expert about rates.

Meanwhile L&C’s form is shorter (you can even even skip questions), but at the end you’re prompted to book a phone call with an adviser.

Round 2: Support and advivce

Within minutes of filling in the onlne form, I was live-chatting with a human adviser at Habito. I was delighted to be through to the real-human stage so quickly, although I noticed that every so often, one of his messages was machine-generated, or at the very least copy and pasted. Maybe that’s inevitable when mortgage advisers have to be sure they’ve communicated certain things, and in a clear way, but nonethless it was a tiny bit jarring.

My phone call approintment with L&C was a 1-hour window. They called in the first 5 minutes and the call lasted around 45 minutes. The first 10 minutes or so was fairly black-and-white questions that could easily have just been incorporated in the web form. Maybe L&C are running drop-off experiments to see what works best. But I was annoyed when a number of the questions from the web form were repeated in the phone call. It was also clear that the adviser I was speaking to was simply filling out a digital form themselves!

What I did like, was that for the monthly expendidture questions (which were quite in-depth) L&C had modelled the likely numbers for my household, and they sounded about right most of the time, so that saved me some head scratching!

Round 3: Panels and recommendations

Anywhere close to 100 lenders is very good in the UK. Habito currently advertises 95+ mortgage lenders in its panel, while L&C advertises 90+.

My L&C adviser mentioned that L&C doesn’t work with Lloyds (Habito doesn’t either). As it happens, I didn’t mind that, as I’m not a fan of Lloyds’ new policy of undermining any overpayments you make by simply reducing your monthly direct debit.

After about 40 minutes on the phone with L&C, I was given some indicative rates. The next step then is a 10-minute “recommendation call”, summarising your requirements and explaining how these have led to a specific mortgage product being recommended. L&C likes to immediately follow this call with a chat with a protection adviser (to discuss life and home insurance). That’s likely to be a long one.

Habito was faster in getting to the actual rates, but perhaps a tiny bit less thorough (which, at less than an hour into my research journey, wasn’t necessarily a bad thing).

After getting an indicative rate, I asked my Habito adviser if I might be able to access better rates on a slightly longer or shorter fixed-rate term. He said he’d check the shorter term. L&C actually made the suggestion for me without prompting, and checked both shorter and longer terms.

Round 4: Next steps

After a recommendation call with L&C, provided you want to go ahead, the “case management team” takes over. That means it’s no longer a single adviser handling your case. You can still make an appointment with your dedicated adviser, subject to their specific working hours (which might not be at weekends, for example).

With Habito you can log back in and select “Resume my chat” whenever you like within opening hours. If your dedicated adviser isn’t online, your chat can be picked up by somebody else. Habito’s portal is clean, glitch-free and ultimately easier to use than L&C’s.

The bottom line

I probably had a slightly stronger feeling that I’d done my due diligence with L&C. But it was sometimes a bit painful getting to that point. For the initial research stage, Habito was faster, slicker and easier.

Ultimately, both these brokers are providing a strong service to Brits seeking a new mortgage. Especially given that they’re not charging consumers a fee. They’ve got similar near-comprehensive panels, and experienced in-house human experts. There are just slight differences in the journeys which might be a matter of personal preference. Young, digital-savvy first-time buyers may prefer Habito. Others may like a phone-call-based service. While it maybe shouldn’t form a huge part of your consideration, L&C offers a £20 refer-a-friend Amazon voucher… which is a nice touch!

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Chris Lilly is Head of publishing at finder.com. He's a specialist in personal finance, from day-to-day banking to investing to borrowing, and is passionate about helping UK consumers make informed decisions about their money. In his spare time Chris likes forcing his kids to exercise more.

See full bio

Chris's expertise

Chris

has written

515

Finder guides across topics including:

Looking for a mortgage with TSB? Compare different rates and mortgage types, and find out how to get the right home loan for you.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.