We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for credit cards

To make comparing even easier we came up with the Finder Score. Costs, perks and suitability across 120+ cards are all weighted and scaled to produce a score out of 10. The higher the score the better the card – simple.

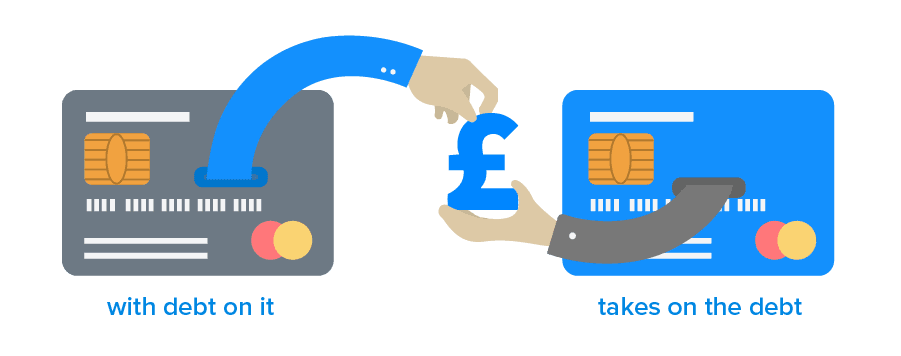

Transferring your current card debt to a 0% balance transfer credit card can be a smart choice if you’re seeking a more affordable way to pay off your outstanding balance.

The best balance transfer credit cards offer an introductory 0% interest period, in some cases more than 2 years, giving you plenty of interest-free breathing space to tackle your debt.

However, transferring your balance to one of these cards often means paying a fee: usually 1-3% of the balance. If you’re planning to transfer a hefty sum, this fee could be painful. Fortunately, there are no-fee alternatives out there.

How do no-fee balance transfer credit cards work?

They work in the same way as any other balance transfer card, except that, as long as the transfer is completed within a set period (usually 60 or 90 days, depending on the provider) you won’t be charged an upfront fee.

If you’re paying interest on existing credit card debt, switching it to a credit card with no balance transfer fee may seem like a no-brainer. However, there are some things you should consider.

Downsides of credit cards with no balance transfer fees

You’ll need a good credit score to qualify for the best deals.

0% introductory offers tend to be shorter compared to credit cards that charge a balance transfer fee. For example, as of January 2023, the top no-fee balance transfer card offered 22 months at 0%, compared to 33 months with a fee-charging card.

If you don’t pay off your balance before the 0% deal ends, you’ll pay a high rate of interest.

When comparing your options, it’s important to assess both the fee and the duration of the 0% introductory offer. If you’re confident you can pay off your debt in a shorter time and you can afford the repayments, opting for a no-fee card is likely to be the best option. However, if you require additional time to pay off your debt, it’s advisable to choose a card with a balance transfer fee. Paying a transfer fee could still work out cheaper than keeping your debt on an existing credit card that’s racking up a lot in interest.

No-fee balance transfer eligibility criteria

To qualify for a no-fee balance transfer card, you’ll need to be at least 18 years old and a UK resident. There may also be a minimum income requirement, depending on the provider.

To access the most competitive no-fee balance transfer deals, you’ll also need a good credit score. Without one your application may be rejected, or you could be offered a shorter 0% deal and a higher rate of interest once the 0% deal ends.

How to compare no-fee balance transfer credit cards

The most important thing to look for is the card with the longest 0% interest promotional period. The longer the deal is, the more time you’ll have to pay off your debt.

It’s crucial to be aware of the balance transfer deadline – the deadline for completing no-fee balance transfers. For most credit cards, the no-fee offer only applies to transfers initiated within the first few months of opening the card account.

Who is a credit card with no balance transfer fee suitable for?

As we mentioned, credit cards with no balance transfer fees tend to come with shorter 0% deals than fee-charging balance transfer cards. This means that a no-fee card will only be suitable for you if you can clear your balance within a shorter period.

Remember that the interest rate jumps as soon as the 0% deal ends, so you don’t want any debt remaining when this happens. You’re better off paying a small fee on a card with a longer 0% deal than risk failing to pay off your no-fee card on time.

No-fee cards are unlikely to be suitable for those who want to make credit card purchases: few of these cards have decent 0% purchase deals, and the standard interest rate on these cards is often relatively high. If you want to spend on your card, you’re better off applying for a second card to use for purchases.

Example: Janet and Marcus pay off their £7,000 wedding credit card debt

Janet and Marcus ran up a £7,000 credit card debt when paying for their recent wedding. The couple decided to transfer the £7,000 debt to a balance transfer card and were considering 2 different cards.

Card A was a 30-month 0% balance transfer card with a 3% balance transfer fee. With this card, they would have to pay off a total of £7,210 (including the £210 fee) by making monthly payments of £240.

However, they also looked at Card B: a balance transfer card with no fees, but a shorter 0% interest period of 22 months. Transferring their balance to this card would mean paying back a total of £7,000 in monthly payments of £318.

Janet and Marcus looked at their budget and worked out that they could afford the monthly repayments of £318, so they decided to opt for Card B. This meant they could avoid both £210 in fee costs and the hundreds of pounds in interest they would have paid on their original credit card.

There are 2 main catches with balance transfers. The first is that you might have to pay a transfer fee, which can work out to be expensive if you’re transferring a large balance. The second is that if you have a 0% introductory offer and do not clear your balance before the 0% deal ends, interest charges will be high.

Yes, you can. If you can’t pay off your debt within the 0% period, you can simply transfer the remaining balance to another 0% balance transfer card. But remember, this could involve paying another transfer fee and this can get expensive if you’re doing it on a regular basis.

A 0% balance transfer deal typically only applies to balances transferred within the few first months of card ownership. It’s best to transfer your debt as soon as possible.

You’ll only be eligible to transfer the balance if the new debt doesn’t take you over your credit card limit.

If you’re making different types of transactions on your credit card (for example, balance transfers, purchases and cash withdrawals), you will hold a separate balance for each.

When making repayments, the credit card company has to reduce the balance with the highest interest rate attached to it first.

However, if the interest rates are the same on each balance, it’s up to the credit card company which debt is reduced first.

When you apply for any credit card, including a balance transfer, this application will be recorded in your credit history. That’s why it’s so important to do your research before applying, to minimise the risk of being turned down and damaging your credit score.

Using balance transfers responsibly can help you maintain a healthy credit score in the long run, as long as you make all your payments on time.

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Was this content helpful to you?

Thank you for your feedback!

To make sure you get accurate and helpful information, this guide has been edited by

David Gregory

as part of our

fact-checking process.

Grace was a Finder writer specialising in credit and loans. She's been writing about personal finance for several years and enjoys helping consumers sort the facts from the fluff.

See full bio

If you have a lot of debt on multiple credit cards, you may have been considering moving all of the balances to one card. Find out how to do so in this article.

Had enough of paying a hefty rate of interest on your personal loan? Discover how you can repay your debt faster with 0% money transfer offers.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.