Investing for your children can help secure their financial future, and including them in the process can teach them the value of disciplined wealth-building.

Index funds, with their low costs and broad market exposure, are a reliable choice for long-term growth — for children, adults, anyone really. Index funds minimize risk through diversification and require minimal oversight, making them ideal for busy parents.

Here’s why index funds work, how to choose the right account and practical steps to start investing for your kids.

Why choose index funds for kids’ investments?

Index funds track major market indexes like the S&P 500, offering steady growth over decades. Their low expense ratios, often below 0.1%, preserve returns compared to actively managed funds. The average expense ratio for index equity ETFs (exchange-traded funds) was 0.14% in 2024, compared to 0.44 percent for actively managed ETFs.(1)

For children, the long time horizon maximizes compound interest, turning small contributions into significant wealth. Unlike trendy investments, index funds provide predictable performance, reducing the need for constant monitoring. They’re a practical way to build wealth for future goals like college, a home or financial independence.

Custodial brokerage vs. 529 vs. UTMA: Which account is best for index funds?

Choosing the right account depends on your goals, tax considerations and control preferences. Each option has distinct tradeoffs.

Teen-owned brokerage account. This type of account lets teens invest in index funds themselves, with a parent providing oversight. The account is in the teen’s name, and they can make trades and learn by doing. Gains are taxable. It’s a great option for building investing skills early on.

529 plan. A 529 offers tax-free growth and withdrawals when used for qualified education expenses.(2) You can invest in index-fund-style portfolios, but choices are limited to the plan’s offerings. It’s best if you’re confident the money will go toward education.

UTMA/UGMA (Uniform Transfers/Gifts to Minors Act). This account is parent-managed and holds assets for a child until they reach adulthood, usually between 18 to 25.(3) You can invest in index funds and use the money for anything that benefits the child. Gains are taxable, and the account is less tax-efficient than a 529 but much more flexible.

Custodial brokerages offer the most flexibility for index fund investments, while 529s prioritize education. UTMA/UGMA accounts balance control and gifting but require careful tax planning.

Index funds with low fees and broad exposure suit young investors with decades to grow. Here are some top options:

Vanguard S&P 500 ETF (VOO). Tracks the S&P 500 and has a low expense ratio of 0.03%. It captures large-cap US companies, making it a solid choice for steady, long-term growth.

Vanguard Total Stock Market ETF (VTI). Covers the entire US stock market, including small-, mid- and large-cap stocks. With a 0.03% expense ratio, it offers broad diversification at a low cost.

Fidelity 500 Index Fund (FXAIX). Mirrors the S&P 500 and comes with an even lower expense ratio of 0.015%. Its low fees and consistent performance make it a strong option for cost-conscious investors.

These funds balance cost, diversification and historical returns averaging over 10% annually over the past 10 years.(4),(5),(6)

How to open a custodial account for index fund investing

Opening a custodial account is straightforward and takes less than an hour, often minutes. Follow these steps:

Choose a brokerage: Vanguard, Fidelity Investments and Charles Schwab offer low-cost custodial accounts with access to index funds. Compare fees and fund availability.

Gather documents: You’ll need your child’s Social Security number, birth certificate and your identification.

Fund the account: Most platforms have no minimums to start. Set up automatic contributions for convenience and consistency.

Select index funds: Allocate funds to index funds like VOO, VTI or FXAIX based on your risk tolerance and goals.

Monitor sparingly: Rebalance annually or when contributions increase significantly. Avoid frequent trading to minimize taxes.

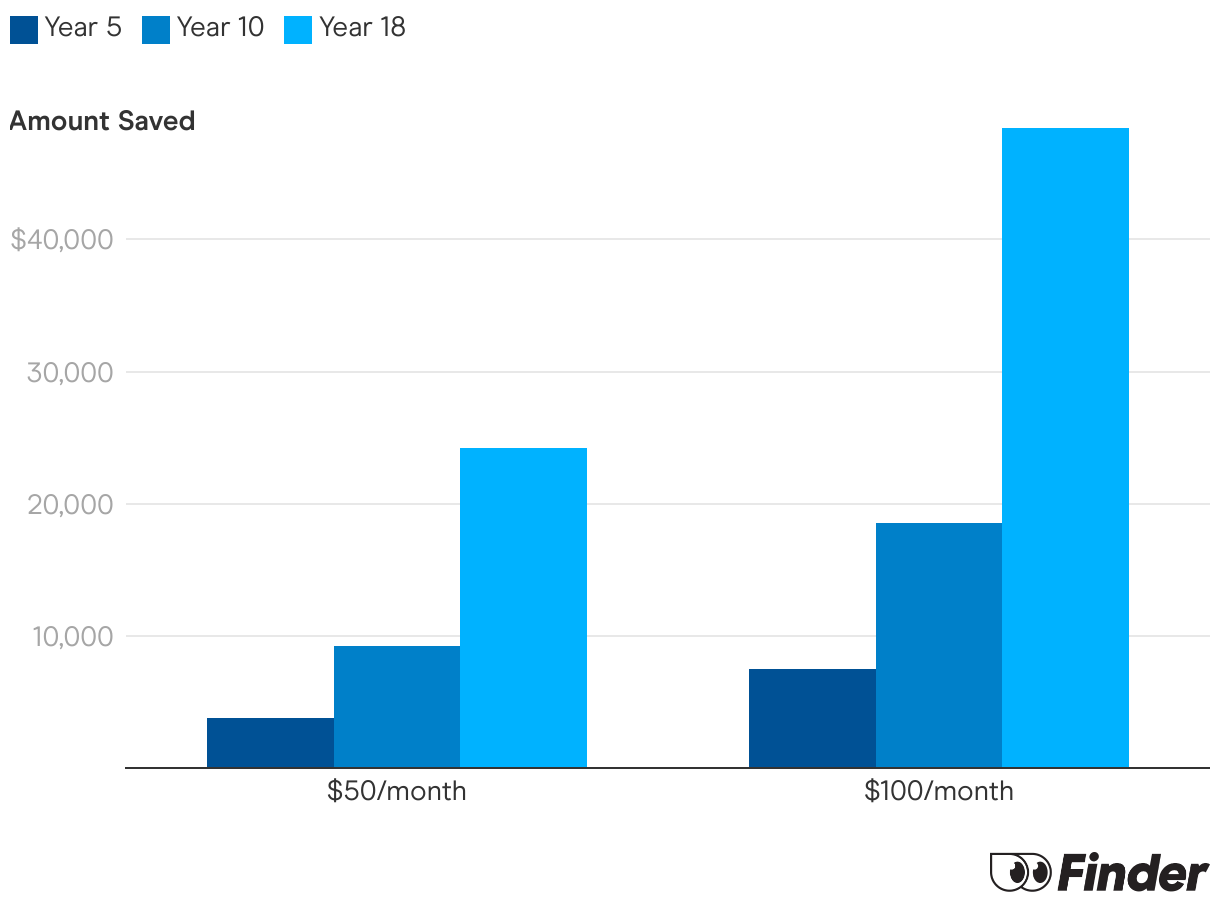

Compound interest example: $50/month over 18 years

Small, consistent investments grow significantly over time. With a $50 initial deposit, investing $50 monthly in an index fund with an 8% average annual return yields:

After 5 years: ~$3,748

After 10 years: ~$9,258

After 18 years: ~$24,214

Starting at birth, $50 monthly becomes more than $24,000 by age 18, a good chunk of money your child can put toward college tuition or a home down payment. Increase contributions to $100 monthly, and the total approaches $49,000. Compound interest rewards early, consistent investing.

This example assumes no withdrawals and doesn’t include reinvested dividends, which would grow the value even more.

Investment calculator

Project the potential growth of investing by considering initial investment, additional contributions, contribution frequency, expected rate of return, compound frequency and your investment time horizon.

Investment Calculator

$

$

years

%

Fill out the form and click on “Calculate” to see your estimated monthly payment.

Results

Teaching your child about index fund ownership

Involving kids in their investments builds financial literacy. Start with age-appropriate lessons:

Ages 5–10. Explain that their account “owns a piece” of many companies, like stores or tech firms. Show them a simple chart of growth.

Ages 11–15. Discuss how small savings grow over time. Share the $50/month example to make it tangible.

Ages 16+. Introduce expense ratios and diversification. Let them track the account’s performance online.

Encourage questions, but keep it practical. Frame investing as a tool for future freedom, not a get-rich-quick scheme. By 18, they’ll understand the value of patience and long-term growth.

Compare investing accounts for kids

Compare accounts based on their fees, age requirements, and features.

Index funds offer a low-cost, low-maintenance way to build wealth for your children. By starting with small contributions in a custodial account, you leverage decades of compound growth. Compare the best brokerage accounts, choose a fund like VOO or VTI, automate investments and teach your kids the principles behind their growing wealth. The earlier you begin, the more time works in their favor.

Frequently asked questions

Yes — a child can have an index fund through a custodial account — like a UGMA or UTMA — managed by an adult until the child reaches legal age.

Matt Miczulski is an investments editor and market analyst at Finder. With over 450 bylines, Matt dissects and reviews brokers and investing platforms to expose perks and pain points, explores investment products and concepts and covers market news, making investing more accessible and helping readers to make informed financial decisions.

Before joining Finder in 2021, Matt covered everything from finance news and banking to debt and travel for FinanceBuzz. His expertise and analysis on investing and other financial topics has been featured on Yahoo Finance, CBS, MSN, Best Company and Consolidated Credit, among others. Matt holds a BA in history from William Paterson University.

See full bio

Matt's expertise

Matt

has written

282

Finder guides across topics including:

The most popular stocks, Finder ranked stocks by the largest daily volume. Stock volume refers to the number of shares traded in a stock.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.