There are many types of compound interest accounts, such as traditional savings, certificates of deposit, money market accounts and more. The best account type for you depends on what you’re saving for, how often it compounds, the eligibility and requirements and how strong the rate is. No matter your end goal, the right compound interest account could help you reach your financial goals sooner.

Compare savings accounts by compound interest

Narrow down top compounding accounts by rates, fees and benefits. Select up to four accounts and select “Compare” to see how they stack up side-by-side. You can also use the calculator to estimate how much your savings can grow.

{"userFilters":[{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["8.95-10","6.95-8.94999","4.95-6.94999","0-4.94999"],"fields":[{"label":"[[FINDER_SCORE_BADGE|9+]] Excellent: 9+","value":"8.95-10","comparator":"range"},{"label":"[[FINDER_SCORE_BADGE|7+]] Great: 7+","value":"6.95-8.94999","comparator":"range"},{"label":"[[FINDER_SCORE_BADGE|5+]] Standard: 5+","value":"4.95-6.94999","comparator":"range"},{"label":"[[FINDER_SCORE_BADGE|0+]] Basic: 0+","value":"0-4.94999","comparator":"range"}]},"dataSelector":{"recordType":"PRODUCT","fieldCode":"FINDER_SCORE.FINDER_SCORE"},"dataType":"NUMBER","label":"Finder Score","queryParameter":"finderScore"},{"config":{"MULTISELECT":true,"VALUES":"ATM\/debit card,Online only,Bonus offer,No monthly fee,Joint account,Crypto account,High APY"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.ACCOUNT_FEATURES"},"dataType":"TEXT","label":"Account features","order":null},{"config":{"MULTISELECT":true,"VALUES":"Cash by teller, Cash by ATM, Check by teller, Check by ATM, Mobile\/remote check deposit, Bank transfer, Wire transfer, Direct deposit, Fiat currencies, Cryptocurrencies"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.DEPOSIT_METHODS"},"dataType":"TEXT","label":"Deposit methods","order":null},{"config":{"MULTISELECT":true,"VALUES":"Alabama,Alaska,Arizona,Arkansas,California,Colorado,Connecticut,Delaware,District of Columbia,Florida,Georgia,Hawaii,Idaho,Illinois,Indiana,Iowa,Kansas,Kentucky,Louisiana,Maine,Maryland,Massachusetts,Michigan,Minnesota,Mississippi,Missouri,Montana,Nebraska,Nevada,New Hampshire,New Jersey,New Mexico,New York,North Carolina,North Dakota,Ohio,Oklahoma,Oregon,Pennsylvania,Rhode Island,South Carolina,South Dakota,Tennessee,Texas,Utah,Vermont,Virginia,Washington,West Virginia,Wisconsin,Wyoming"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.STATE_AVAILABILITY"},"dataType":"TEXT","label":"States serviced","order":null},{"dataSelector":{"recordType":"UI_FILTER_COMPONENT","fieldCode":"SPECIAL_OFFERS"},"dataType":"BOOLEAN","label":"Special offers","componentType":"SpecialOffersFilter","config":{"VALUES":"1","fields":[{"value":"rewards_exclusive","label":"Finder Rewards & exclusives"},{"value":"all_offers","label":"All offers"}]},"options":{"comparator":"eq"},"queryParameter":"special-offers"}],"niche":{"currencySymbol":"$","decimalPoint":".","decimalPlaces":"2","thousandsSeparator":",","filterBoundsMap":{"product.DETAILS.ACCOUNT_FEATURES":null,"product.DETAILS.DEPOSIT_METHODS":null,"product.DETAILS.STATE_AVAILABILITY":null}},"prefilled":false,"experimental":false}

6 of 18 results

Compare other products

We currently don't have that product, but here are others to consider:

Looking for other options? Check out other similar products.

How we picked these

What is the Finder Score?

The Finder Score crunches over 250 savings accounts from hundreds of financial institutions. It takes into account the product's interest rate, fees, opening deposit and features - this gives you a simple score out of 10.

To provide a Score, Finder’s banking experts analyze hundreds of savings accounts against FDIC-reported national averages as a baseline. Accounts with rates well over the national average are scored the highest, while accounts with rates well below are scored low.

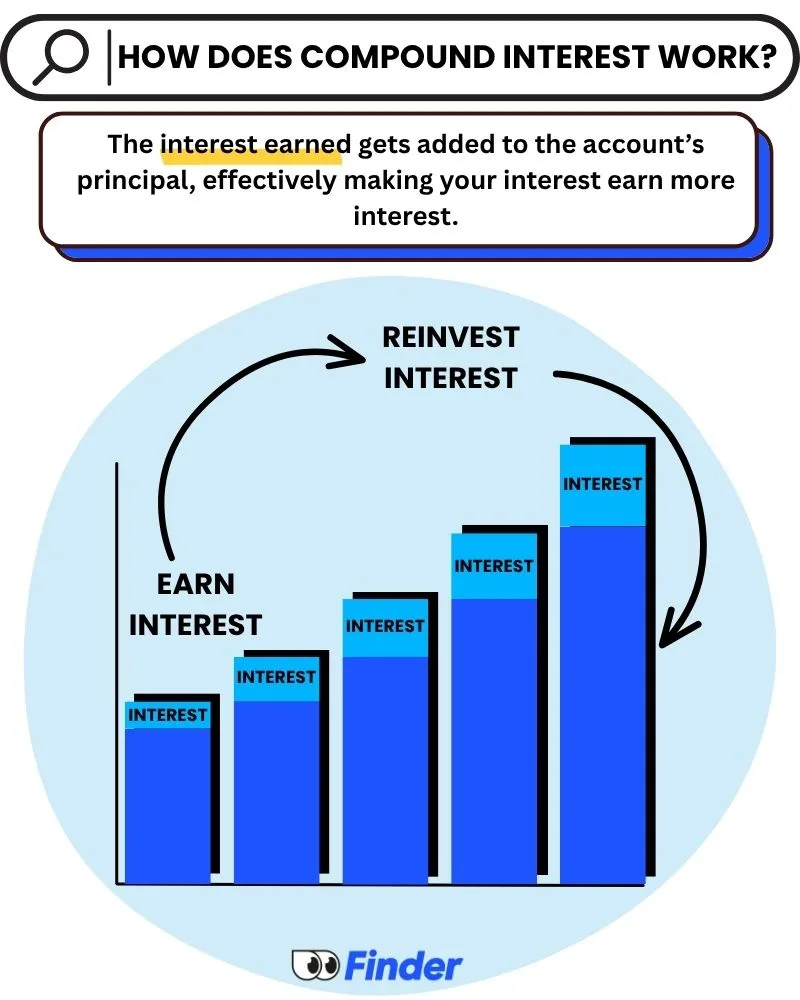

Compound interest is actually very simple: The interest earned gets added to the account’s principal, effectively making your interest earn more interest.

Compound interest has three main factors:

Interest rate: This is the percentage of the principal that is added as interest, often expressed as an annual percentage, such as a 5% annual percentage yield (APY).

Principal: The total funds the interest rate is applied to.

Time: How long you let the principal sit in the account to earn interest.

Most interest-bearing accounts compound daily or monthly, meaning your earned interest is folded into your balance each day or once a month. Daily compounding is the ideal rate, as it’s the fastest way to grow your money. But depending on the interest rate and your balance, the difference between daily, monthly and yearly compounding might only amount to a matter of pennies.

Here are the four most common ways interest is compounded:

Daily compounding. This is the quickest way to grow your money because interest is added to your account balance every day. Most savings accounts compound interest daily and post earnings to your account monthly.

Monthly compounding. Interest is calculated on your account once per month. Your balance doesn’t grow as fast as it would with daily compound interest, but it’s still quicker than other frequencies.

Quarterly compounding. Interest is calculated once every three months. Although uncommon, some credit unions still use this compounding period.

Annually compounding. As the name suggests, annual compound interest is calculated once a year. This compounding period is most commonly used with investment accounts.

What does “compounded continuously” mean?

Continuous compounding is a theoretical idea where interest would be earned and added to the balance an infinite amount of times. This, however, does not happen in real life, so you won’t find any accounts that are compounded continuously. However, many savings accounts compound daily, which is the quickest way to earn interest over time.

9 types of compound interest accounts

When comparing the best compound interest account for you, consider the account’s requirements, its rate and how often it compounds.

Savings accounts with compound interest often compound daily or monthly. These accounts tend to limit the number of withdrawals you make each month, and their interest rate fluctuates alongside changes to the federal interest rate. The best high-yield savings accounts offer far more competitive yields than traditional brick-and-mortar banks, and we often see APYs around 3%.

With SoFi Checking and Savings get paid up to two days early. Set up direct deposit to automatically get your paycheck up to two days early every time you get paid

Up to 3.10% APY on savings by meeting deposit requirements or by paying the SoFi Plus subscription fee every 30 days

Get a $50 or $400 bonus depending on direct deposit amounts

New and existing Checking and Savings members who have not previously enrolled in Direct Deposit with SoFi are eligible to earn a cash bonus of either $50 (with at least $1,000 total Eligible Direct Deposits received within 25 calendar days of your first Eligible Direct Deposit of $1 or more) OR $400 (with at least $5,000 total Eligible Direct Deposits received within 25 calendar days of your first Eligible Direct Deposit of $1 or more). Cash bonus amount will be based on the total amount of Eligible Direct Deposit received within 25 calendar days of your first Eligible Direct Deposit of $1 or more. If you have satisfied the Eligible Direct Deposit requirements but have not received a cash bonus in your Checking account, please contact us at 855-456-7634 with the details of your Eligible Direct Deposit. Direct Deposit Promotion begins on 5/15/2026 and will be available through 12/31/26. See full bonus and annual percentage yield (APY) terms at sofi.com/banking/checking-offer/

Annual percentage yield (APY) is variable and subject to change at any time. Rates are current as of 5/28/26. There is no minimum balance requirement. Fees may reduce earnings. Additional rates and information can be found at https://www.sofi.com/legal/banking-rate-sheet

We do not charge any account, service, or maintenance fees for SoFi Checking and Savings. We do charge transaction fees for outgoing wire transfers, Instant Transfers, and global remittance transfers. Our fee policy is subject to change at any time. See the SoFi Bank Fee Sheet for details at sofi.com/legal/banking-fees/.

SoFi Bank is a member FDIC and does not provide more than $250,000 of FDIC insurance per depositor per legal category of account ownership, as described in the FDIC’s regulations. Any additional FDIC insurance is provided by the SoFi Insured Deposit Program. Deposits may be insured up to $3M through participation in the program. See full terms at SoFi.com/banking/fdic/sidpterms. See list of participating banks at SoFi.com/banking/fdic/participatingbanks.

We’ve partnered with Allpoint to provide you with ATM access at any of the 55,000+ ATMs within the Allpoint network. You will not be charged a fee when using an in-network ATM, however, third-party fees may be incurred when using out-of-network ATMs. SoFi’s ATM policies are subject to change at our discretion at any time.

Early access to direct deposit funds is based on the timing in which we receive notice of impending payment from the Federal Reserve, which is typically up to two days before the scheduled payment date, but may vary.

Overdraft Coverage is a feature automatically offered to SoFi Checking and Savings account holders who receive at least $1,000 or more in Eligible Direct Deposits within a rolling 31 calendar day period on a recurring basis. Eligible Direct Deposit is defined on the SoFi Bank Rate Sheet, available at https://www.sofi.com/legal/banking-rate-sheet. Members enrolled in Overdraft Coverage may be covered for up to $50 in negative balances on SoFi Bank debit card purchases only. Overdraft Coverage does not apply to P2P transfers, bill payments, checks, or other non-debit card transactions. Members with a prior history of unpaid negative balances are not eligible for Overdraft Coverage. Eligibility for Overdraft Coverage is determined by SoFi Bank in its sole discretion. Members can check their enrollment status, if eligible, at any time by logging into their account through the SoFi app or on the SoFi website.

Earn up to 3.80% Annual Percentage Yield (APY) on SoFi Savings with a 0.70% APY Boost (added to the 3.10% APY) for up to 6 months. Open a new SoFi Checking & Savings account with Eligible Direct Deposit by 12/31/26. Rates variable, subject to change. Terms apply at sofi.com/banking#2. SoFi Bank, N.A. Member FDIC.

2. Certificates of deposit (CDs)

CDs typically compound daily or monthly. Compared to savings accounts, their main advantage is that they’ll lock in the account’s APY for the duration of the CD term — if the fed rate changes, your CD’s APY is unaffected for the term. If you need to withdraw your money before the term is up, you’ll pay an early withdrawal fee. The best CDs offer high interest rates for a low minimum opening deposit, and average rates are anywhere from

0.23% to

1.35%, according to the FDIC.

Patriot offers a strong 3.60% APY on its 3-month CD through Raisin. Pay no fees and just a $1 minimum deposit.

3.60% APY.

Interest compounds daily.

$0 monthly fee.

3. Interest-bearing checking accounts

While rare, some checking accounts offer interest, which typically compounds daily, monthly, quarterly or yearly, depending on the bank. Checking accounts tend to have lower interest rates than savings accounts or CDs and may also carry fees or restrictions.

With SoFi Checking and Savings get paid up to two days early. Set up direct deposit to automatically get your paycheck up to two days early every time you get paid

Up to 3.10% APY on savings by meeting deposit requirements or by paying the SoFi Plus subscription fee every 30 days

Get a $50 or $400 bonus depending on direct deposit amounts

New and existing Checking and Savings members who have not previously enrolled in Direct Deposit with SoFi are eligible to earn a cash bonus of either $50 (with at least $1,000 total Eligible Direct Deposits received within 25 calendar days of your first Eligible Direct Deposit of $1 or more) OR $400 (with at least $5,000 total Eligible Direct Deposits received within 25 calendar days of your first Eligible Direct Deposit of $1 or more). Cash bonus amount will be based on the total amount of Eligible Direct Deposit received within 25 calendar days of your first Eligible Direct Deposit of $1 or more. If you have satisfied the Eligible Direct Deposit requirements but have not received a cash bonus in your Checking account, please contact us at 855-456-7634 with the details of your Eligible Direct Deposit. Direct Deposit Promotion begins on 5/15/2026 and will be available through 12/31/26. See full bonus and annual percentage yield (APY) terms at sofi.com/banking/checking-offer/

Annual percentage yield (APY) is variable and subject to change at any time. Rates are current as of 5/28/26. There is no minimum balance requirement. Fees may reduce earnings. Additional rates and information can be found at https://www.sofi.com/legal/banking-rate-sheet

We do not charge any account, service, or maintenance fees for SoFi Checking and Savings. We do charge transaction fees for outgoing wire transfers, Instant Transfers, and global remittance transfers. Our fee policy is subject to change at any time. See the SoFi Bank Fee Sheet for details at sofi.com/legal/banking-fees/.

SoFi Bank is a member FDIC and does not provide more than $250,000 of FDIC insurance per depositor per legal category of account ownership, as described in the FDIC’s regulations. Any additional FDIC insurance is provided by the SoFi Insured Deposit Program. Deposits may be insured up to $3M through participation in the program. See full terms at SoFi.com/banking/fdic/sidpterms. See list of participating banks at SoFi.com/banking/fdic/participatingbanks.

We’ve partnered with Allpoint to provide you with ATM access at any of the 55,000+ ATMs within the Allpoint network. You will not be charged a fee when using an in-network ATM, however, third-party fees may be incurred when using out-of-network ATMs. SoFi’s ATM policies are subject to change at our discretion at any time.

Early access to direct deposit funds is based on the timing in which we receive notice of impending payment from the Federal Reserve, which is typically up to two days before the scheduled payment date, but may vary.

Overdraft Coverage is a feature automatically offered to SoFi Checking and Savings account holders who receive at least $1,000 or more in Eligible Direct Deposits within a rolling 31 calendar day period on a recurring basis. Eligible Direct Deposit is defined on the SoFi Bank Rate Sheet, available at https://www.sofi.com/legal/banking-rate-sheet. Members enrolled in Overdraft Coverage may be covered for up to $50 in negative balances on SoFi Bank debit card purchases only. Overdraft Coverage does not apply to P2P transfers, bill payments, checks, or other non-debit card transactions. Members with a prior history of unpaid negative balances are not eligible for Overdraft Coverage. Eligibility for Overdraft Coverage is determined by SoFi Bank in its sole discretion. Members can check their enrollment status, if eligible, at any time by logging into their account through the SoFi app or on the SoFi website.

Earn up to 3.80% Annual Percentage Yield (APY) on SoFi Savings with a 0.70% APY Boost (added to the 3.10% APY) for up to 6 months. Open a new SoFi Checking & Savings account with Eligible Direct Deposit by 12/31/26. Rates variable, subject to change. Terms apply at sofi.com/banking#2. SoFi Bank, N.A. Member FDIC.

4. Money market accounts

These accounts compound daily, monthly, quarterly or yearly, depending on the bank. Money market accounts are very similar to a savings account when it comes to interest and saving money. The main difference is that money market accounts typically offer a debit card and the ability to write checks. Rates between savings accounts and money market accounts are roughly similar, so the one you choose depends on whether you value the additional spending flexibility.

5. IRA accounts

An IRA account is made of a variety of investment options, and each could compound at a different rate: monthly, bi-monthly or annually. There are multiple great IRA options, including Roth and Simple IRAs, each with its own set of rules and advantages. Compared to savings accounts or CDs, IRA accounts are riskier as they’re subject to the ups and downs of the stock market. These accounts have the opportunity for the biggest gains over a long period, though they carry more risk of value loss through market volatility.

6. Cash management accounts

Also called CMAs, these accounts are like a checking and savings hybrid. They’re FDIC insured and can offer checks and debit cards, earn APY and allow you to easily move your funds to and from your investment account. CMAs are typically offered by non-banks, such as investment firms or brokerages, where your funds are invested across different institutions. CMAs often have high balance requirements and may come with monthly fees.

7. Dividend stocks

Dividend stocks tend to compound quarterly, though you can find some that compound monthly. Dividend stocks are a type of stock investment that pays out dividends based on your owned shares. These can lead to stable, reliable returns on an investment, though the quality of your investment can range from company to company and how they react to a fluctuating economy.

8. Bonds

Bonds earn interest monthly and compound semi-annually every six months. Bonds are an asset investment option similar to stocks or real estate. By buying one, you’re technically giving the entity a loan. These entities eventually pay back the bond amount purchased by the consumer, plus interest. They fall into three categories: corporate, government and municipal. You can’t retrieve your money before the bond’s maturity without paying some form of penalty, typically three to 15 months of interest, depending on when you cash out. Bonds tend to have higher interest rates than savings accounts and CDs: I bonds currently sport an APY of 6.89%, according to TreasuryDirect.

These high-return investment options grant assets that return a portion of the company or land’s profits. Since its profits rely on other factors like the real estate market, REITs are a riskier investment compared to savings accounts or CDs.

The power of compound interest

Compound interest can mean big savings over time, with little to no effort.

For example: Let’s say you place $500 into a daily compounding savings account with a 5% interest rate and let it sit for one year. After one year, your total principal balance is $525.63, the next year it’s at $552.58, and the next is $580.91, and so on. In five years, your balance becomes $642. Compound interest drastically speeds up the savings process without any extra effort — that’s the power of compounding interest accounts.

How to open a compound interest account

You can open a compound interest account the same way you would any bank account. The first step would be to find an account with a compounding frequency that suits your needs. Look at the deposit agreement to find the account’s compounding frequency, and if you can’t find it, contact the bank.

How do I make the most of compounding interest?

Get the most out of the power of compounding interest with these tips:

Try not to withdraw. Uninterrupted compounds interest grows consistently when you do not make withdraws, so the more that’s in your account at the end of the month, the more interest you’ll earn. For this reason, it’s a good idea to have a daily, uninterrupted compound interest account that’s seperate from your everyday checking account.

Start early. Time is a major factor with compound interest accounts. The sooner you start, the more interest you can earn over time.

Make frequent deposits. The more you can add to the principal, the more growth and compound interest you can earn and take advantage of uninterrupted compound interest.

Stay on top of your monthly minimum. Some accounts require a minimum monthly balance before requiring a fee. Keep more money in your own pocket by meeting that minimum.

Get a free account. The best accounts won’t nickel and dime your savings away.

Compound interest is one of the most important things to consider when trying to save money.

If you’re not sure where to start, look at our top savings accounts. Note that interest rates are often variable, meaning they can change according to the federal interest rate.

Frequently asked questions

Are compound interest accounts secure?

Yes, most are protected compound interest accounts. As long as you bank with an FDIC- or NCUA-insured institution, your funds are protected up to $250,000. Most reputable banks and accounts are insured. Accounts that don’t offer this insurance are much riskier.

CD vs. high-yield savings: Which is better?

Certificates of deposit (CD) and high-yield savings are both deposit accounts that earn interest. With CDs, your funds are locked for a set term, usually between three months to 10 years. If you withdraw funds from a CD before the term is over, you’ll likely have to pay early withdrawal penalty fees, usually around 90 to 180 days of earned interest. CDs also don’t allow you to add more funds to the account after you open it. With savings accounts, you can add or withdraw funds as you wish within the transaction limits.

If you want more access to your savings, a high-yield savings account is the way to go. But if you want more bang for your buck, a CD is the better option, and they tend to offer much higher APYs than traditional savings accounts.

Do T-Bills compound interest?

Unlike Treasury bonds, treasury bills (T-bills) don’t compound interest. Treasury bonds compound interest every six months. T-Bills are bought at a discounted rate, and you get the full value when it matures. For example, say you were to buy a T-Bill for $90, and it’s worth $100. Once it matures, you get $100, so you technically made $10.

Does a 401(k) have compound interest?

Yes, they can. A 401(k) is a retirement plan offered by employers to help employees save up money for retirement. When you contribute to the 401(k), you can choose to invest the funds into investments that compound interest.

Bethany Hickey is the banking editor and personal finance expert at Finder, specializing in banking, lending, insurance, and crypto.

Bethany’s expertise in personal finance has garnered recognition from esteemed media outlets, such as Nasdaq, MSN, Yahoo Finance, GOBankingRates, SuperMoney, AOL and Newsweek. Her articles offer practical financial strategies to Americans, empowering them to make decisions that meet their financial goals. Her past work includes articles on generational spending and saving habits, lending, budgeting and managing debt.

Before joining Finder, she was a content manager where she wrote hundreds of articles and news pieces on auto financing and credit repair for CarsDirect, Auto Credit Express and The Car Connection, among others.

Bethany holds a BA in English from the University of Michigan-Flint, and was poetry editor for the university’s Qua Literary and Fine Arts Magazine.

See full bio

Bethany's expertise

Bethany

has written

448

Finder guides across topics including:

Compare some of the best high-yield savings accounts available.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.