Personal loan early repayment calculator

Enter the details of your outstanding loan to estimate how much you could save by repaying early.

Whether you’ve currently got a personal loan or are looking to take one out, it’s important to understand how easy it is to overpay and what doing so will save you on repayments. But frustratingly, UK lenders are not always as upfront about the costs and savings as they could be. The good news is that they’re all bound by the same rules.

Yes. Under the Consumer Credit Regulations 2004, you’re entitled to fully or partially repay your personal loan early in the UK, but lenders can still charge you up to an additional two months interest on any sums paid ahead of time.

So while many lenders advertise that you won’t pay an early repayment charge (ERC) or fee if you pay off your loan sooner than agreed, chances are you’ll still be charged up to two months interest on whatever sums you repaid early. Some lenders will classify this additional interest as an ERC, others won’t. It means you may be in for a surprise when you request a final settlement figure and find you haven’t saved quite as much as you might have imagined.

Whether it’s because you’ve been responsible with your spending and saving, have come into an unexpected inheritance or have even won the lottery, it generally still makes financial sense to try and pay off your loan as soon as possible. After all, nobody knows what’s around the corner, so it’s smart to get yourself in a strong financial position while the going’s good!

This can vary from lender to lender and can also depend on the length of time remaining on your loan:

Additionally, if part of your monthly repayments goes towards the product fee (this is normally the case with peer-to-peer loans), then you’ll need to clear the fee in full when you settle the loan.

If you’re part-way through a loan and want to find out the exact amount, contact your lender and request a “final settlement figure”.

Thanks to the Consumer Credit Act, borrowers who repay early are entitled to a rebate equivalent to the difference between the total remaining projected cost of the loan and the amount given by the following formula (explanations of the various elements of this formula can be found at the link above):

Got that? Glad that’s sorted then. Don’t worry if that looks a bit complicated. The long and short of it is that the amount you’ll save by repaying early is likely to vary from lender to lender, but they’re all subject to the restrictions of the above formula. You can use our calculator to get a rough idea.

Enter the details of your outstanding loan to estimate how much you could save by repaying early.

After 6 months, you decide you want to repay the loan in full. Up to this point, you’ve actually repaid around £876 of the original £10,000 (as well as around £277 in interest).

This means you still owe around £9,124 on your original loan amount. As you’ve still got more than 12 months left on your loan, your lender charges you an additional 58 days interest. So as well as that outstanding £9,124 you’ll pay around a further £86 in interest.

If you repay now, then the overall cost of the loan will have been approximately £10,363.

If you leave the loan to run its natural course, then the overall cost of the loan will be approximately £11,529.

As with the first example above, you decide you want to repay your loan after 6 months. So far, you’ve repaid around £756 off your initial loan amount (as well as £573 in interest). You still have more than 12 months remaining on your loan term, so the lender charges you an additional 58 days of interest.

You still owe £9,244 on your original loan amount, and the 58 days interest on this equates to around £185 in interest.

If you repay now, then the overall cost of the loan will have been approximately £10,758.

If you leave the loan to run its natural course, then the overall cost of the loan will be approximately £13,297.

As you can see from the examples above, you may save hundreds or even thousands of pounds by repaying your loan early. However, even repaying a 5-year loan after 6 months can still end up being quite expensive.

Because of the way interest repayments work, the amount of interest you pay each month decreases over the course of the loan. This means you’re paying off less of your principal in the early months of the loan, but this amount will still need to be repaid when you decide to pay off your loan early.

As a general rule of thumb, you’ll likely save money in interest by repaying your loan early if you have at least 2 months left on your loan term, but the amount you save overall may be less than you expected.

It’s worth contacting your lender directly and ask for a calculation of how much you’d owe in fees and interests if you were to repay your loan early.

Most peer-to-peer platforms (these are online marketplaces where investors lend money to borrowers) – like Zopa or RateSetter – charge a “loan fee” or “lender fee” as well as interest. Normally a small part of each monthly repayment will go towards this fee, and if you want to pay off your loan early, you’ll need to clear this fee in full.

Your credit agreement sets out the terms which both the lender and the borrower must stick to. It’s this document that’s covered by the Consumer Credit Act (bear in mind that certain types of loan are exempt from this, such as loans from an employer, mortgages and credit union loans). This should detail how you can repay your loan early, as well as any interest charges or ERCs you may need to pay.

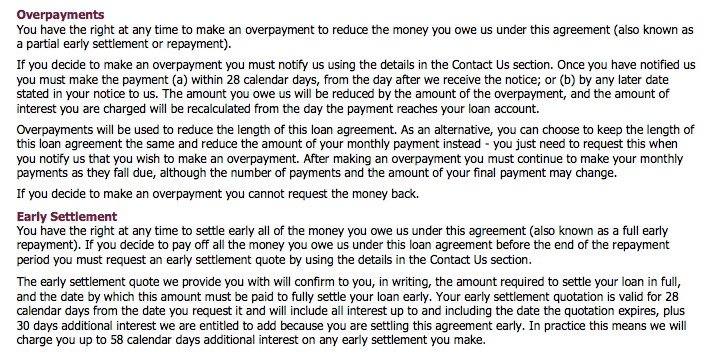

Below is an excerpt from one popular lender’s agreement document:

The early repayment policy above is quite typical – any sums paid early may incur up to about 2 month’s interest beyond the date on which the lender received notice from you. Some lenders, especially many of the “payday” lenders, will only charge you for the days on which you borrowed the money.

Here are the steps you’ll need to follow if you want to settle your loan ahead of time.

If you’re aiming to make overpayments here and there when you’ve managed to save a little extra or spend a little less that month, or if you’ve come into some money and want to pay a chunk off your debt, here’s what you should do.

It many cases, it should be possible to simply transfer funds to your loan account. In a few, more old-school cases, you may need to let your lender know verbally or in writing of your intention, and then make your overpayment within 28 days (you are under no obligations at this point, and can simply continue with the loan as previously agreed should you wish).

Either way, your payment schedule for the rest of the loan will be adjusted accordingly. Lenders can either keep your remaining instalment amounts the same, and your loan will simply end earlier; or reduce your instalment amounts so that the loan still ends at the same point. Your lender should clarify in the loan agreement which of these they will do by default, and you may allowed to specify which of the two you’d rather.

Potentially, yes. After signing the loan agreement you’ll have 14 days in which to cancel – this is your “cooling off” period. What’s more, you don’t even have to give a reason. Naturally, the lender will want you to return the all money straightaway – legally you have 30 days in which to do so. Just remember that even if you cancel the loan, the lender is allowed to charge you interest until it receives the funds back from you.

Moving a balance from a personal loan to a credit card.

Perhaps you haven’t yet taken out a personal loan, and you’re simply at the stage of shopping around. If you’re hoping to be able to make overpayments on the loan here and there, or if you have a lump sum of cash coming your way sometime soon, you should factor early repayment terms into your comparison.

Favourable early settlement terms could well be more useful to you than a slightly lower rate. Remember, if a lenders states “there are no charges for repaying your loan early” that’s not the same as saying that repaying your loan early will save you money. As well as looking for favourable terms, look at how easy it actually is to overpay.

Simply put, lenders usually prefer it if you don’t pay off your loan too soon. Sure, they get their money back safely ahead of time, but they’ve made less money than they expected to. That’s why they don’t always make it as easy as they should to overpay/repay early, and that’s why they may want to charge interest beyond the date of repayment.

Wondering which lenders charge an early repayment fee? The vast majority of banks and personal loan companies in the UK (including HSBC, Santander, Tesco Bank, Halifax and Nationwide) offer unsecured loans with no early repayment fees. However this can seem misleading, in that they are likely to charge up to two months additional interest on sums repaid early.

Loans that are secured against property are much more likely to involve early repayment charges.

Find out whether a personal loan from Finio Loans could work for you.

Abound (formerly Fintern) is a UK lender that promises to offer borrowing “reinvented”, with affordable tailored loans.

Calculate the cost of an MBNA personal loan and see how much you can borrow today.

The super-popular UK challenger bank Monzo now offers flexible personal loans to existing users.

Looking to build your credit score at no cost? Loqbox is an innovative new service designed to do just that.

Find out more about Admiral unsecured personal loans of between £1,000 and £25,000. Get an instant decision and enjoy a fixed rate with no setup fees.

Novuna (formerly Hitachi) Personal Finance is not a bank – it’s a simplified, online finance provider from Japan that makes instant decisions on personal loans. Check out whether Novuna could be the yin to your financial yang.

See how to get a personal loan with the innovative lender Zopa, and get the latest Zopa loan rates, in our review.

Find out all you need to about personal loans from 118 118 Money. Fast simple comparison with a range of UK lenders.

Compare Halifax fixed-rate personal loans against products from a range of UK lenders. Apply online and secure a competitive rate.