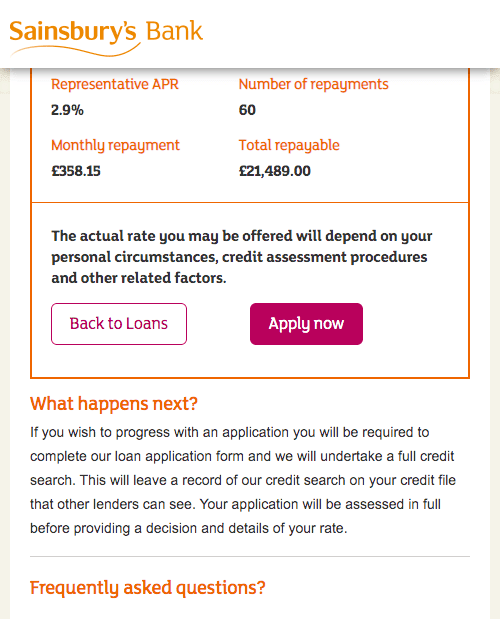

Please note: You should always refer to your loan agreement for exact repayment amounts as they may vary from our results.

Late repayments can cause you serious money problems. See our debt help guides.

Sainsbury’s Bank are no longer accepting new loan applications from new or existing customers. Sainsbury’s Bank have stated that if you are an existing customer, no immediate changes will be made to your current products or services. Compare alternatives below.

We currently don't have that product, but here are others to consider:

How we picked theseTo make it even easier to compare and evaluate unsecured loans we came up with the Finder Score. Speed, features and flexibility across 60+ lenders are all weighted and scaled to produce a score out of 10. The higher the score the better the lender – simple.

Read the full methodologyPlease note: You should always refer to your loan agreement for exact repayment amounts as they may vary from our results.

Late repayments can cause you serious money problems. See our debt help guides.

Sainsbury’s Bank offered unsecured personal loans, meaning they were based on creditworthiness, rather than using property, vehicles and other assets as collateral. While Sainsbury’s rates were definitely competitive, the advertised representative APR may not be the rate you would receive: Sainsbury’s would offer you a rate based on assessment of your personal financial circumstances.

Here was the typical process for taking out and repaying a Sainsbury’s loan:

The Annual Percentage Rate (APR) is a figure that all lenders have to calculate in the same way, which is designed to provide an annual summary of the cost of a loan. It takes into account both interest and any mandatory charges to be paid (for example an arrangement fee) over the duration of a loan.

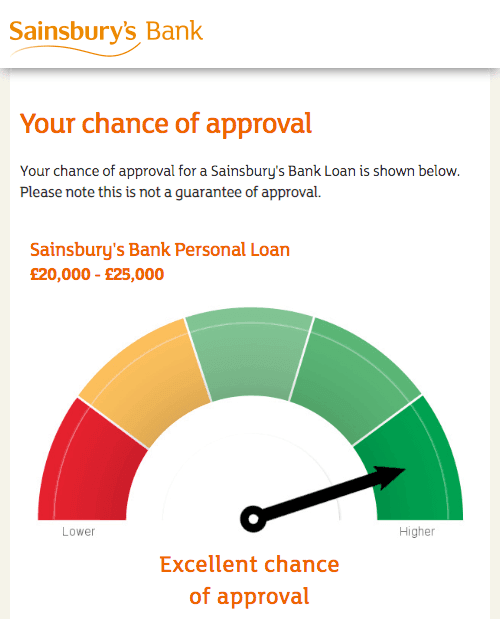

Though Sainsbury’s loans tend to have a very competitive APR, this is usually a sign that you’ll need a decent credit score to get approved, especially for larger loans.

The APR can provide a handy benchmark for comparison (alongside other factors like the monthly and overall cost), but there is a catch. Sainsbury’s is only obliged to award this rate to 51% of its borrowers – the other 49% could pay more. That’s why it’s often referred to as the “representative” APR. The rate you’re ultimately offered will depend on factors like the amount you apply for, the term of the loan, your credit rating and your income.

Sainsbury’s Bank are no longer accepting new loan applications from new or existing customers. If you are an existing customer, no immediate changes will be made to your current products or services.

87% of customers we surveyed in 2026 would recommend Sainsbury's Bank to a friend.

It provides a clear and transparent loan experience with no hidden charges. Customers value the straightforward online application and the easily understandable repayment details. The bank is praised for treating its customers fairly and offering flexible, long-term repayment plans.

While many users secured low interest rates, a few felt their personal APR was higher than they had hoped for.

AI-generated summary from the text of customer reviews on Finder.

You can contact customer support on 0800 056 0565. Lines are open Monday to Friday 8am – 8pm and Saturday 8am – 4pm. If you’re struggling to pay, you can call 08085 405060. Lines are open Monday to Friday 8am – 7pm, and Saturday and Sunday 8am – 5pm.

Find out whether a personal loan from Finio Loans could work for you.

Here are 4 personal loans myths that we have busted.

Calculate the cost of an MBNA personal loan and see how much you can borrow today.

The super-popular UK challenger bank Monzo now offers flexible personal loans to existing users.

Looking to build your credit score at no cost? Loqbox is an innovative new service designed to do just that.

Looking for a personal loan? Read the definitive guide to find out how to compare interest rates, fees and features to find the right loan for you. There’s a range of loans available to apply for – we’ll help you find the right one.

Find out more about Admiral unsecured personal loans of between £1,000 and £25,000. Get an instant decision and enjoy a fixed rate with no setup fees.

Novuna (formerly Hitachi) Personal Finance is not a bank – it’s a simplified, online finance provider from Japan that makes instant decisions on personal loans. Check out whether Novuna could be the yin to your financial yang.

See how to get a personal loan with the innovative lender Zopa, and get the latest Zopa loan rates, in our review.

Find out all you need to about personal loans from 118 118 Money. Fast simple comparison with a range of UK lenders.