Sponsored by

Customers Bank High Yield Savings through Raisina free savings platform where you can find, fund, and manage top rated products from federally insured banks across the nation, all from one single account.

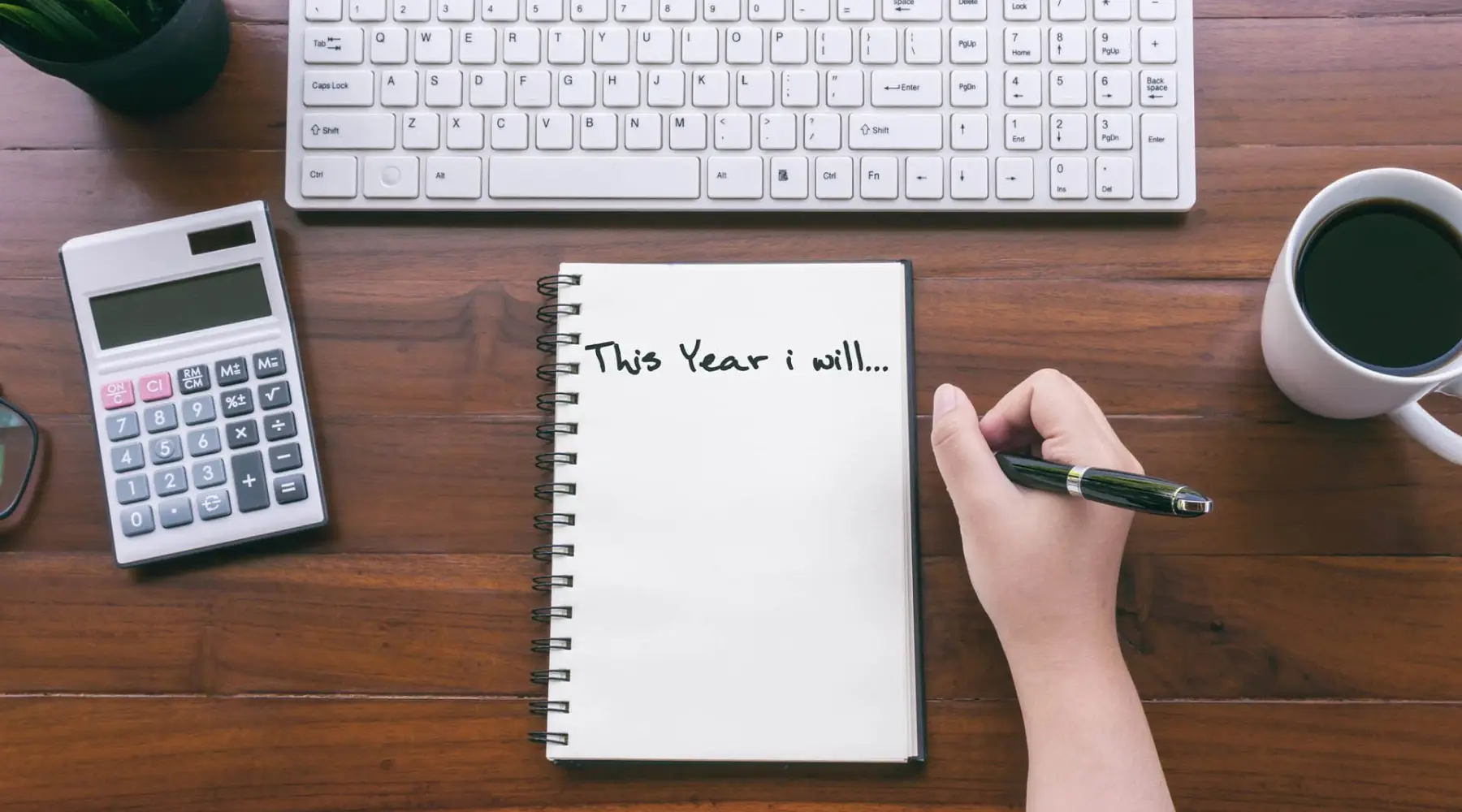

A lot of people attempt to make financial resolutions for themselves, but it’s easy to fall short. Life happens, things don’t pan out the way they should, or you simply forget. But one way to really set yourself up for success is by getting as specific as possible with your resolutions, and turning them into an actionable plan. Here are five financial resolutions you can check off this year:

1. Set a real savings goal

Making the generic New Year’s resolution of “save more money” isn’t helpful. Make an actual goal that’s measurable, take advantage of tools and set a realistic contribution amount that won’t break your bank account.

For example, make the resolution: “Save over $1,000 for my emergency fund by saving at least $100 per month with automatic deposits into my savings account.”

By creating specific and realistic goals, you can set yourself up for success in 2024.

If you already have a savings account and you didn’t shop around, there’s a good chance it has a rate as low as 0.01%, which is common among the largest traditional banking institutions and lower than then

0.45% national average as reported by the FDIC.

Your savings interest rate and how much you keep in your account can make a big difference. For example, if you keep $5,000 in a 0.46% APY savings account, you’ll end up earning about $23 in 12 months. It’s not nothing, but you could earn more.

In a 5% APY savings account, that same $5,000 could earn you about $256 in just 12 months. Stack that with regular contributions and a higher starting deposit and you’ll really boost your savings.

If you’re looking to snag the best rates, look at Raisin, a free savings platform, featuring some of the highest yielding savings accounts in the market, all of which only require a $1 opening deposit, are FDIC insured, and have no monthly fees or withdrawal limitations.

Savings calculator

Calculate how much you could earn with a high-yield savings account.

3. Review your budget

You’ve probably been told to make a budget countless times, but it really is a very important way to responsibly handle your finances. With a good budget, you can narrow down how much you really spend in expenses, how much you have leftover, and then make a plan to pay off your debt.

Making a budget with pen and paper can feel like a pain, but budgeting apps can help you budget like a pro in no time.

4. Consider a fixed-rate CD

A certificate of deposit (CD) is a type of savings deposit account. These accounts earn a guaranteed amount of interest over the course of the term, and typically offer higher APYs than traditional savings accounts. Your funds are locked away for the set term, so it’s a solid investment option if you have some savings you don’t need to access for months at a time.

Unlike savings accounts, your rate is fixed, so it won’t suddenly decrease over the course of the term. Interest rates are expected to drop in the coming months, so locking your rate with a CD is worth considering.

You can take advantage of some of the highest CD rates available with Raisin, which offers exclusive APYs, a low $1 opening deposit requirement and a range of terms that allow you to tailor your savings strategy to your specific goals.

5. Don’t splurge your tax refund

With tax season around the corner, now is the time to make a plan on how you’ll use it. The temptation to splurge with your refund is real, but it may be more useful paying off high-interest credit card debt, making an extra loan payment, or any other debt you may have lingering after the holidays.

The average tax refund for 2022 was $2,899, according to the IRS. With that mind, make a plan on how you’ll carefully spend your estimated tax refund if you’re owed one.

Remember that by paying off debt faster than expected, you’re saving yourself money in interest charges. This can include things like mortgages, credit cards and auto loans. The quicker they’re paid, the more you can save. Or you can simply deposit your tax refund into a high-yield CD or savings account that you open on the Raisin platform.

Bottom line

From prioritizing savings to paying off debts, make 2024 the year to recenter. One of the major keys in financial wellness is having a solid plan, realistic goals and the right tools.

If you’re like the 68% of Americans who report having less than $100,000 in their savings, or the 14% who report not having a savings account at all, make 2024 the year to change that. Savings accounts are protected under FDIC or NCUA insurance up to $250,000 per individual, per institution, and can passively grow your funds to fight inflation and keep your funds earning passively.

If you’re not sure where to start saving with the highest savings or CD rates, check out Raisin’s easy-to-use marketplace featuring some of the best APYs in the country.

If you’re not sure where to start saving, check out Raisin’s free platform, which makes it easy to find, fund and manage savings products with some of the best APYs in the country.

{"visibility":"visibilityTable","ctaLabel":"Calculate","tableCode":"savings_calculator_table","nicheCode":"USFSA","fields":[{"name":"PERIOD","value":"1","options":"","label":"Years to save","suffix":"","useSuffixAsPrefix":false,"useDropDownOption":false,"tooltip":""},{"name":"INITIAL_DEPOSIT","value":"1000","options":"","label":"Initial deposit","suffix":"$","useSuffixAsPrefix":true,"useDropDownOption":false,"tooltip":"Select Calculate to see your estimated total balance based on the current APY for each product below"}]}

Bethany Hickey is the banking editor and personal finance expert at Finder, specializing in banking, lending, insurance, and crypto.

Bethany’s expertise in personal finance has garnered recognition from esteemed media outlets, such as Nasdaq, MSN, Yahoo Finance, GOBankingRates, SuperMoney, AOL and Newsweek. Her articles offer practical financial strategies to Americans, empowering them to make decisions that meet their financial goals. Her past work includes articles on generational spending and saving habits, lending, budgeting and managing debt.

Before joining Finder, she was a content manager where she wrote hundreds of articles and news pieces on auto financing and credit repair for CarsDirect, Auto Credit Express and The Car Connection, among others.

Bethany holds a BA in English from the University of Michigan-Flint, and was poetry editor for the university’s Qua Literary and Fine Arts Magazine. See full bio

Bethany's expertise

Bethany has written 400 Finder guides across topics including:

Invoice financing can help your business meet immediate cash flow needs based on your unpaid invoices.

Feedback

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Advertiser Disclosure

finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which finder.com receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. finder.com compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.