Loans for Single Moms: How to Use Personal Loans Strategically

Personal loans can offer fast breathing room when life doesn't. But the right choice for single mothers depends on the timing, tradeoffs and total cost.

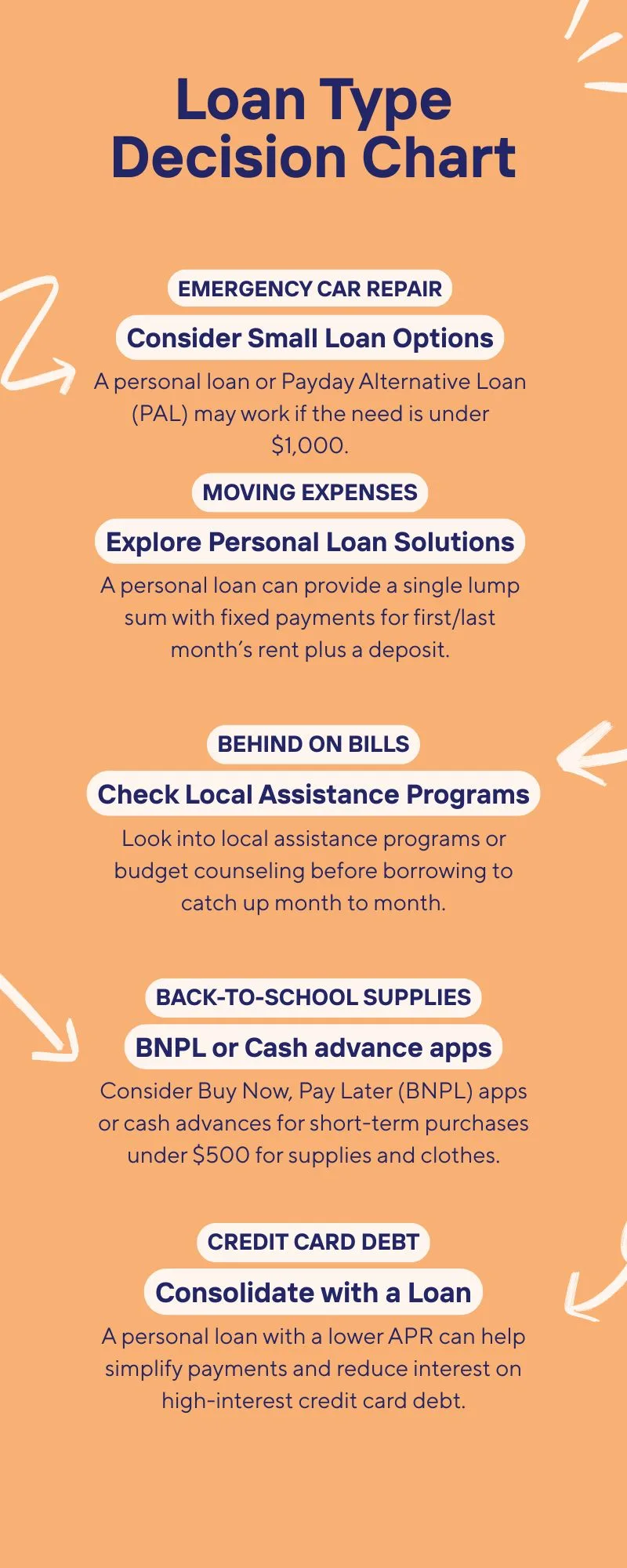

Personal loans work best for one-time, defined expenses — medical bills, car repairs, moving costs — not as a patch for ongoing income shortfalls.

APRs range from 7% to 36%, and most online lenders require a credit score of 580 or higher; a score above 670 unlocks the best rates.

Credit unions and reputable online lenders are often the most flexible options for borrowers with imperfect credit — child support and alimony income typically counts toward your application.

An APR above 30% is a red flag — before signing, explore 0% intro credit cards, local assistance programs, or payday alternative loans from credit unions first.

This summary was generated by AI and may contain errors or omissions.

For single moms juggling income, expenses and emergencies on their own, personal loans can offer short-term relief — but they come with tradeoffs. The right loan can stabilize your budget with fixed terms and predictable payments. The wrong one can add financial pressure you didn’t plan for.

When a personal loan may make sense for your situation

Single moms often manage both household budgets and income alone, with little room for unexpected costs or long-term financial juggling. Personal loans can serve as stopgaps for:

Medical bills not covered by insurance

Car repairs or transportation needs

Childcare transitions

Moving costs or security deposits

Debt consolidation with a clearer payoff timeline

Unlike credit cards, personal loans provide a lump sum up front, repaid in fixed monthly amounts over a set period. That stability makes them easier to budget around.

Hot tip

If the expense has a clear end date, like a move or medical bill, a personal loan can give you control without the spiral of revolving credit.

Best types of personal loans for single moms

Not every loan structure fits every situation. These common options offer different tradeoffs depending on how much you need, how fast and how predictable your budget is.

Loan Type

Best For

Key Tradeoff

Unsecured Personal Loan

Flexible use, no collateral needed

Higher rates if credit is poor

Credit Union Loan

Lower interest if you qualify

Membership may take time

Payday Alternative Loan (PAL)

Small, short-term borrowing

Capped amounts, slower application

Secured Personal Loan

Larger loans if assets are available

Risk of losing asset if unpaid

Cash advances

Smaller expenses like school supplies

Borrowing amounts may start low

Lenders to compare

These lenders stand out for their flexibility, speed and range of borrower profiles, including those managing on one income or rebuilding credit.

The right lender isn’t just the one that says yes, it’s the one that matches your timeline, credit profile and comfort with digital or in-person service.

Lender Type

Pros

Cons

Credit Unions

Lower APRs, member-focused policies, more flexible

May require in-person visit or membership process

Traditional Banks

Trusted, established, may offer bundled products

Higher credit standards, slower approval

Online Lenders

Fast decisions, prequal options, tailored to subprime

Higher APRs, heavy marketing, more variation in terms

What lenders look for

Lenders focus on financial basics, not family status, when deciding whether to approve a personal loan. Here’s what they typically look for:

Requirement

What It Means

Credit Score

580+ for most online lenders, 660+ for lower rates

Debt-to-Income (DTI)

Ideally below 36%. Child support can count as income or obligation, depending.

Employment or Income

Steady income from a job, benefits, or self-employment is usually required

Loan Purpose

Some lenders favor certain uses, like consolidation or emergencies

Single moms who receive child support, alimony, or government assistance may be able to list these as part of total monthly income. Not all lenders allow it, so checking their policies matters.

Can single moms get a loan with bad credit?

Yes, but expect tradeoffs. Single moms with low credit scores, typically below 580, may still qualify through lenders that specialize in subprime borrowers. These loans usually come with higher interest rates, lower borrowing limits and shorter repayment terms.

Options worth exploring:

Online lenders like Avant and OneMain Financial, which cater to borrowers with less-than-perfect credit.

Credit unions, which may consider your relationship and income rather than relying solely on credit score.

Co-signed loans, where a trusted person with stronger credit adds their name. This improves approval odds but puts their credit at risk if you miss payments.

Secured loans, backed by savings or a vehicle, which reduce risk for the lender and can lower your rate.

Credit Score Range

Loan Access

APR Range

Best Channels

300–579

Limited, high-interest loans

28%–36%+

Subprime online lenders

580–669

Moderate access, stricter terms

18%–32%

Credit unions, Avant, LendingPoint

670+

Broad access, better rates

7%–20%

SoFi, LightStream, major banks

Hot tip

If your credit is under 600, prequalify with multiple lenders to compare rates before committing. A soft credit check won’t hurt your score.

How to improve approval odds

Getting approved for a personal loan isn’t always about perfect credit. Small, targeted moves can improve your chances and possibly lower your rate — especially if you’re working with a tight income or rebuilding your financial footing.

Pay down credit cards. Reducing your revolving balances can lower your debt-to-income (DTI) ratio, a key number lenders use to gauge risk. Even a few hundred dollars can make a difference.

Prequalify first. Many lenders let you check potential rates with a soft credit pull, which won’t impact your score. This helps you compare offers and avoid unnecessary rejections.

Add a co-borrower if it’s safe to do so. A trusted family member or partner with stronger credit may improve your approval odds. But if you miss payments, their credit — and your relationship — could take a hit.

Consider secured options. If you have a car title or savings account, using it as collateral can reduce the lender’s risk and result in better terms.

Typical costs and what to expect

Most personal loans come with APR ranges between 7% and 36%, depending on your credit profile. Additional costs may include origination fees and late payment charges, though some personal loans come with no fees.

Factor

Typical Range

APR

7% to 36%

Origination Fees

0% to 8% of the loan amount

Loan Term

12 to 60 months

Monthly Payment

Based on amount, APR, and term

Example: A $5,000 loan at 16% APR for 36 months would result in:

Monthly payment: ~$176

Total interest paid: ~$1,346

Total cost of the loan: ~$6,346

Hot tip

If you’re offered a loan with an APR above 30%, pause. That’s often a sign of financial strain that another solution might better resolve.

Calculate your monthly loan payment

Use our personal loan calculator to compare monthly loan payments and the loan’s total cost based on different interest rates and loan terms.

A personal loan isn’t always the best tool. If the need is small, short-term, or specific, these options may fit better.

0% APR credit card offers. Good for planned expenses if you can pay off during the promo window.

Local assistance programs. City or county offices may offer emergency grants for single parents.

Cash advance app. Get small advances with no credit check or interest.

Payday Alternative Loans (PALs). Offered by some credit unions, these are cheaper than payday loans and capped in interest.

BNPL apps (like Affirm or Klarna). Spread out smaller purchases with BNPL, though not great for essential bills.

Hardship loans or programs. Some lenders may offer hardship loans, or you may look into hardship programs that offer payment deferments without interest or penalties.

Borrowing from family or friends (with an agreement). Can help avoid interest, but only if the repayment plan is clear.

Final questions to ask before you apply

Here are a few questions to help guide you on whether now is the right time for a personal loan:

Is this loan solving a one-time problem or masking a recurring shortfall?

Will I still be able to cover rent, groceries and childcare once payments start?

What happens if I lose income for a month?

Good loans solve real problems without putting your stability at risk. If the math works and the terms are clear, a personal loan can be a clean financial tool, not a burden.

Bottom line

Loans can provide crucial support for single moms managing unpredictable expenses, but success depends on choosing terms that fit your budget and repayment ability. Prioritize understanding the full cost, compare lenders carefully and avoid borrowing for ongoing expenses until your finances are steady. Credit unions and reputable online lenders often offer the most flexible options, especially if your credit isn’t perfect.

Megan B. Shepherd is a personal finance expert and editor for loans and insurance at Finder.

Her personal finance expertise has been featured on Forbes, Nasdaq, MediaFeed, Fox News, Time, Reviews.com, and carinsurance.com, adding invaluable information related to personal loans, financial strategies and smart borrowing tactics.

Megan graduated from the University of Texas at Dallas with a BS in Business Administration with an entrepreneurial focus. She's worked as a certified financial adviser and has earned certificates of completion from A.D. Banker & Company.

See full bio

Megan B.'s expertise

Megan B.

has written

105

Finder guides across topics including:

The passing of a loved one is a tough time. Learn if a funeral loan could help ease the financial burden so you can focus on planning a deserved farewell.

Wondering whether to choose a 3-year or 5-year personal loan to consolidate your credit card debt? We compare both terms side by side to help you decide.

Personal loans offer quick cash for Home Depot trips and contractors, but larger renovations may require a different type of loan.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.