Finder makes money from featured partners, but editorial opinions are our own.

Advertiser disclosure

How to find the cheapest mortgage rates

Save thousands by knowing how to compare rates, fees and more.

Positioning yourself for the lowest interest rate you’re eligible for is among the best ways to save on your loan. Even a difference of less than 1% can save you thousands over a 30-year mortgage.

Positioning yourself for the lowest interest rate you’re eligible for is among the best ways to save on your loan. Even a difference of less than 1% can save you thousands over a 30-year mortgage.

When looking for the most competitive rates, consider:

The Federal Reserve implements monetary policies that can sometimes affect mortgage interest rates, such as its target for the federal funds rate — the rate used by commercial banks to borrow and lend their excess reserves overnight — which can affect variable rate loans, such as adjustable-rate mortgages. Fixed-rate, long term mortgages may not see a direct effect from the federal funds rate, but may be affected by other Federal Reserve policies that impact the cost of credit.

As you shop around for the right loan, use these tips to help you get the best deal possible:

Find the best mortgage lender for you

Compare mortgage lenders to get the best rate and terms for your needs.

Most mortgages come with fees separate from your interest rate and repayments. They’re often calculated into a loan’s comparison rate. Upfront, one-time fees — like origination or application fees — can sound expensive. But smaller, ongoing fees often cost you more in the long run.

Not always. To find out how much a loan will cost you, you need to crunch the numbers. If a loan has a low rate and features you need, then it might be worth paying a small ongoing fee.

Some fees come due only at the end of the loan or when switching lenders. Keep this in mind if you’re planning to refinance your mortgage for a lower rate or shorter term down the road.

Most mortgages require a down payment of 5% to 20% of your property’s value. Generally, the bigger your down payment, the less you’ll need to borrow to cover your home’s purchase price.

It pays to save up as much as you can for your down payment. You’ll not only land lower monthly repayments, but if you put down less than 20% of your property’s value, you’re also required to pay private mortgage insurance — or PMI — on top of your loan.

In some cases, a bigger down payment of 30% or more can unlock lower rates, though that kind of upfront payment may be unrealistic for many first-time homebuyers.

Your repayment structure greatly affects the cost of your mortgage or home loan. Loans on which you’re repaying your principal and interest result in bigger monthly repayments, though they’re often cheaper in the long run.

Interest-only loans tend to result in much cheaper repayments during the interest-only period but higher repayments afterward — which costs you more over time.

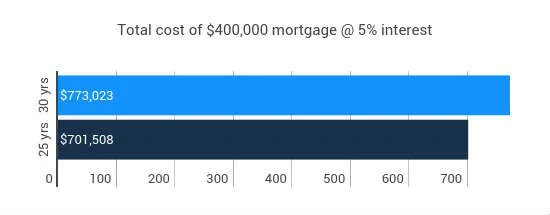

The faster you pay off a mortgage, the less interest you pay over time. So even though repayments for a 25-year home loan might look high compared with those of an identical 30-year home loan, you’ll likely save more with the shorter loan.

Here’s what you’d end up paying for a $400,000 mortgage over 25 years and 30 years at 5% interest:

A 25-year mortgage requires higher repayments, but it’s cheaper in the long run because you’d pay less interest.

A mortgage is a big commitment. But by knowing what to look for, find the cheapest rates, lowest fees and best terms on your home loan, potentially keeping thousands in your pocket.

Image: Shutterstock

Extending a loan that large can mean paying over double the interest, so it’s probably not in your best interest.

Step-by-step guide to mortgage relief, refinance programs and down payment help for homeowners and buyers.

Academy Mortgage offers faster-than-normal closing times, but it’s not available in New York.

United Wholesale Mortgage is a loan wholesaler that partners with mortgage brokers and financial institutions.

Ameris Bank has a wide range of loans and multiple branches but only in the Southeast.

Neat Capital offers faster than normal closing times, but it’s only available in specific states.

This lender specializes in financing mobile homes, but customer support can be difficult to contact.

This lender offers a wide range of mortgage products, but branch locations are limited.

This lender offers a wide variety of mortgage products, but your experience may vary.

A top lender of FHA and VA loans, but customer reviews are very mixed.