Twine app review

Twine isn't available on Finder right now.

- Stock trade fee

- N/A

- Minimum deposit

- $100

Summary

A saving and investing tool designed to help couples reach individual and joint goals.

Developed by John Hancock,Twine offers savings and investment options to help you and your partner tailor your strategy for short and long term goals. But it doesn’t offer cash deposits and can take up to three days to access your money.

How much does Twine cost?

The service doesn’t charge many fees, but there are still a few you should look out for:

| Type of fee | Savings account | Investment account |

|---|---|---|

| Annual | None | 0.6% |

| Other | Wire transfers, paper statements, insufficient funds (varies) | ETF fees (varies) |

How do I fund my Twine account?

There’s only one way to fund your Twine account, and that’s by linking your bank account, which is required during the application process.

How do I open a Twine account?

Twine operates entirely online, so the application process begins on the Twine website:

Online

- Go to the provider’s site and follow the steps to apply.

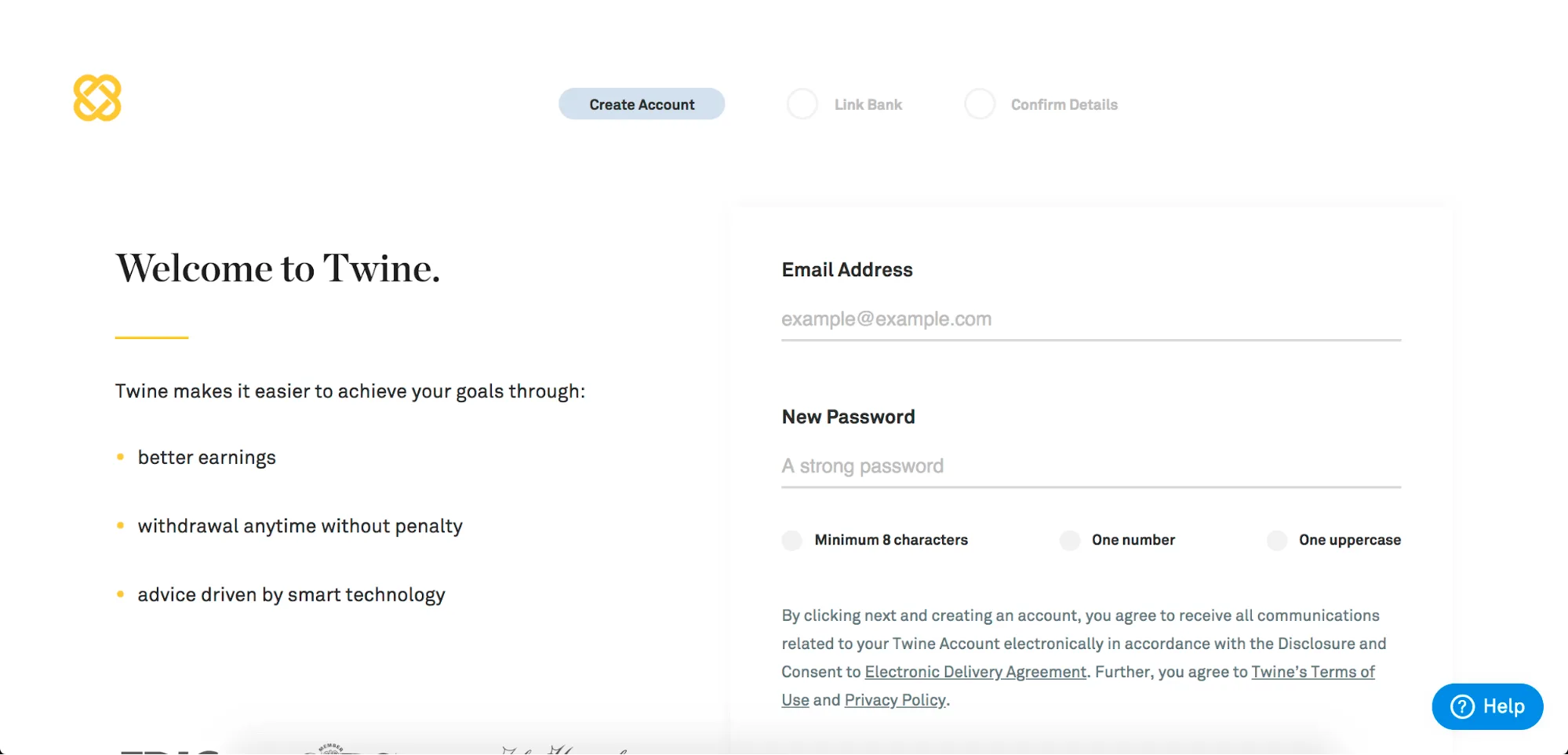

- From Twine’s website, click Sign up in the top right corner.

- Enter your email address, create a password and click Next.

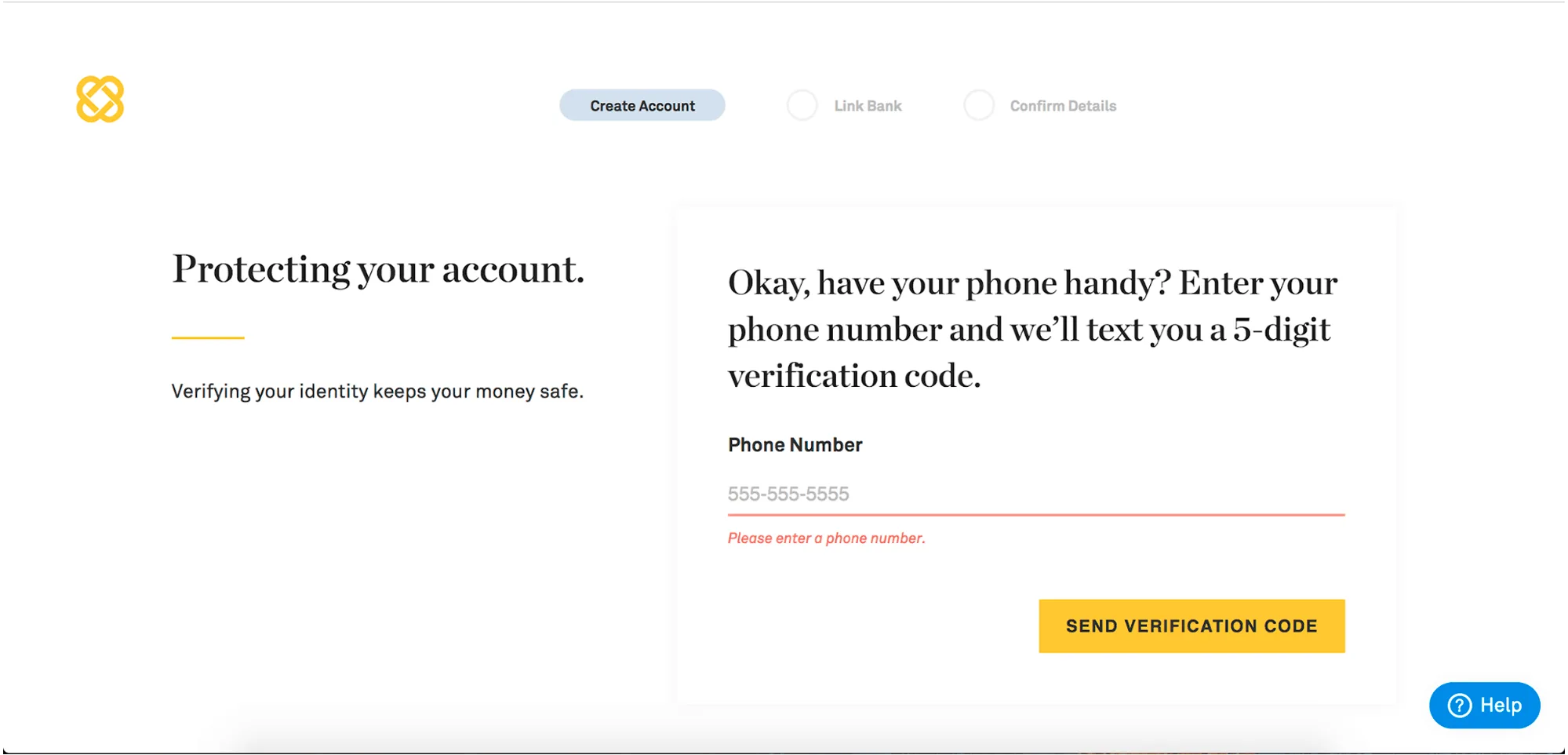

- Enter your phone number and click Send verification code.

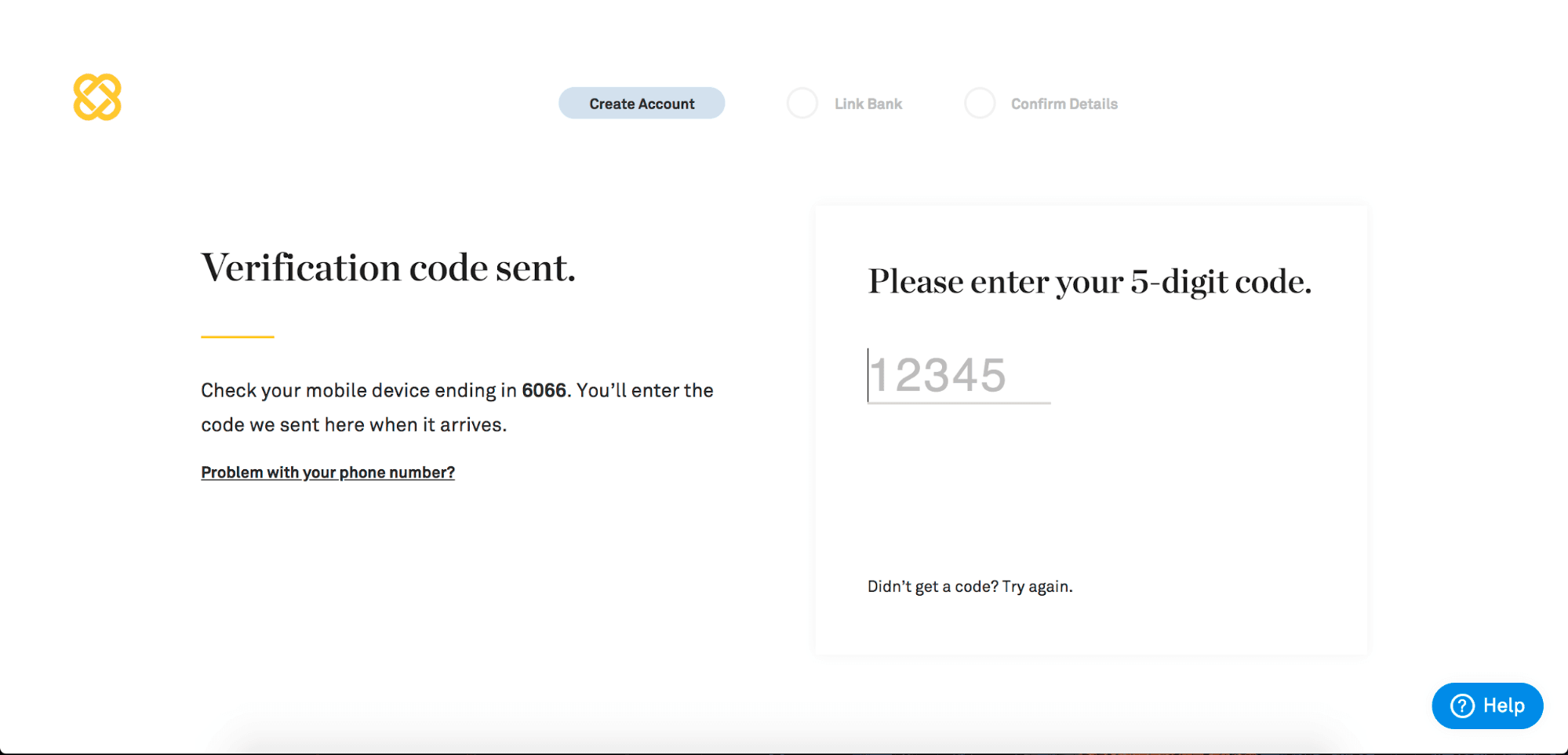

- Enter the five-digit verification code.

- Select your avatar, then click Next.

- Link your bank account.

- Enter any other requested information and adjust your preferences.

- Your application is complete.

Eligibility

To open either type of account, you’ll need to meet a few eligibility requirements:

- US Social Security number

- US mailing address

- US citizen

- Social Security number

- At least 18 years old

Required information

Whether you apply online or on the app, you’ll be asked for the following information:

- Social Security number

- Government-issued ID

- Investment preferences and goals

Benefits of Twine savings

Twine’s free savings account has low minimums and fees, and pays a competitive interest rate. Here’s what makes it stand out from the competition:

- No fees. The Twine savings account is free to open and charges no monthly service fees.

- Access when you need it. Use the dashboard or mobile app to access your money anywhere.

- Low minimum balance. You can open an account with as little as $5 and you won’t pay fees for low balances.

- Security. Twine uses bank-grade encryption and is covered by both FDIC and Securities Investor Protection Corporation (SIPC).

- Savings goals. Set up as many individual or joint savings goals as you’d like.

- Set it and forget it. Set up recurring deposits from other bank accounts to build a saving and investing habit that can help you reach your financial goals.

What should I look out for?

The Twine savings account offers strong features with virtually no fees, but there are still a few things to look out for:

- No interest. Unlike other savings accounts, you won’t earn anything when you stash your money with Twine.

- No branches. Twine operates entirely online, so you won’t be able to visit a branch for assistance.

- No cash deposits. Since Twine doesn’t have ATMs, you won’t be able to make cash deposits.

- No ATM card. Unlike some other savings accounts, the Twine savings account doesn’t come with ATM access.

- Withdrawal wait times. You’ll usually have to wait two to three business day to process your withdrawal.

Benefits of Twine investing

Once you’re ready to invest, Twine uses robo-advising to diversify your money in a mix of exchange-traded funds. Its dashboard allows you to easily manage your money, which is protected by FDIC and SIPC. Other benefits include:

- Few fees. Other than ETF management fees, the only fee you’ll pay is 25 cents monthly for every $500 in your account, which works out to 0.6% annually.

- ETFs. Twine invests your money in a diversified portfolio with a selection of stocks and bonds.

- Personalized. Your investment portfolio reflects your risk tolerance, preferences and more. Plus, you can set up custom recurring deposits to grow your savings faster.

- Dividends. Some ETFs pay cash dividends that are moved into your savings account.

- Goals. Create individual or joint goals to save for short and long term financial plans.

What should I watch out for?

While Twine is a unique platform that encourages couples to work together, it does have a few drawbacks:

- Online only. You can only access your portfolio online or on the app — there are no physical branches.

- Slightly higher fees. Twine’s 0.6% annual fee is slightly higher than some of its competitors.

- No retirement accounts. Unlike some other robo-advisors, Twine doesn’t allow you to open retirement accounts.

- Minimum opening deposit. To move from the savings to the investment account, you’ll need to have a balance of at least $100.

- ETF fees. Twine only charges a 0.6% management fee for invested accounts, but the underlying ETFs in your portfolio may charge small fees.

- No human advice. While you can get personalized tips and investment advice from Twine’s algorithms, there’s no human financial advisor to assist you.

Customer reviews and complaints

Based on its Apple App Store rating, Twine is well-liked by its customers.

As of April 15, 2020, Twine has a 4.5 out of 5-star rating based on over 4,400 reviews. Customers enjoy the ease and simplicity of Twine’s goal feature, allowing them to create individual or collaborative goals with a spouse or partner to save for a future milestone.

As far as complaints go, slow processing seems to be a common concern among Twine investors. Customers making a withdrawal from their Twine account cited wait times in excess of 10 business days before gaining access to their funds. Others reported a three-week waiting period to have their account application processed.

Unfortunately, this is the only Twine feedback we could find. It doesn’t have a Better Business Bureau or Trustpilot page, and no complaints have been lodged against it on the Consumer Financial Protection Bureau.

Compare Twine to other options

Compare other products

We currently don't have that product, but here are others to consider:

How we picked theseWhat is the Finder Score?

The Finder Score crunches over 250 savings accounts from hundreds of financial institutions. It takes into account the product's interest rate, fees, opening deposit and features - this gives you a simple score out of 10.

To provide a Score, Finder’s banking experts analyze hundreds of savings accounts against FDIC-reported national averages as a baseline. Accounts with rates well over the national average are scored the highest, while accounts with rates well below are scored low.

How can I get in touch with customer service?

You can contact Twine customer service using:

- Email: Support@Twine.com

- Instagram: @Twine

- Facebook: Twine USA

- X (formerlyTwitter): @Twine

I’ve signed up. Now what?

Now that your account is open, here’s how you can get the most out of it:

- Review your investment preferences. Line them up with your risk tolerance, income and goals.

- Log in. Use the online dashboard or mobile app to monitor and manage your accounts.

- Set up investment goals. Set up as many individual or joint investment goals as you need.

- Recurring deposits. Set up recurring deposits from one or both of your linked accounts to reach your savings goals faster.

Bottom line

Unlike other robo-advisors, couples can organize their money according to joint short and long term financial goals. Plus, you can fund them manually or with recurring deposits.

However, you can’t open a retirement account and investing is done solely online. Compare your options to find the robo-advisor that meets your needs.

Frequently asked questions

Finder Scores: What they mean

If you want peace of mind, this rating will give it to you. These products offer the best value and outcomes considering various product features, terms, conditions and price.

Well-balanced products that provide what you need, offering a healthy mix of competitive features at a good price. However, they're not quite the best in class.

Bottom line: You can find better, but these products still offer reasonable value and have the basics sorted.

These products may not offer much value in the long run, and there are better options available.

Twine is not currently available on Finder

Have you considered SoFi Active Invest?

Trade stocks, ETFs, and options with zero commissions, invest in IPOs or automate your portfolio, with exclusive perks available through SoFi Plus.

- Trade stocks, options, ETFs, mutual funds, alternative asset funds

- $0 commission on stocks, ETFs and options with no options contract fees

- Get up to $1,000 in stock when you open & fund a new Active Invest account.

- Access to a financial planner

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Your reviews

Peter Finder

Writer

You are about to post a question on finder.com:

- Do not enter personal information (eg. surname, phone number, bank details) as your question will be made public

- finder.com is a financial comparison and information service, not a bank or product provider

- We cannot provide you with personal advice or recommendations

- Your answer might already be waiting – check previous questions below to see if yours has already been asked

Finder only provides general advice and factual information, so consider your own circumstances, or seek advice before you decide to act on our content. By submitting a question, you're accepting our finder.com Terms of Use and Privacy and Cookies Policy.

This site is protected by reCAPTCHA and the Privacy Policy and Terms of Service apply.