Does the sender or the receiver decide which money transfer service to use?

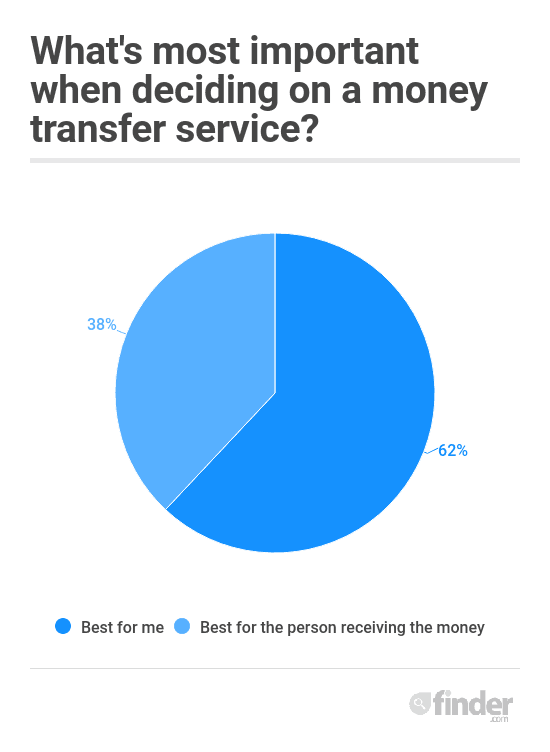

62% select options that best suit themselves over the recipient when sending from the US.

The international money transfer industry is growing more popular every day. To uncover the main reasons those in the US are transferring money overseas, we commissioned a survey of 2,245 adults in July 2017, conducted by global marketing and research company Pureprofile.

Our survey revealed that of those who transfer money overseas, the majority (62%) choose options that best suit themselves, rather than the person they’re sending money to. Decisions could be the result of considering the cheapest option, a platform that’s easy to use or the most convenient. The remaining 38% of people who transfer money overseas choose a provider that’s best for the person they’re sending money to — for instance, because a provider offers cash pickups, direct bank account transfers or faster delivery.

Our survey found that men are more likely than women to look out for themselves when transferring money overseas: 40% of women make transfers that are convenient for the receiver versus 35% of men. Generation X (those ages 35 to 54) are more likely to look out for themselves over the person receiving their money (65%), compared with 62% of millennials (ages 18 to 34) and 53% of baby boomers (ages 55 and older).

Those who are separated are more likely to choose a money transfer provider that best suits them, while widowers are the most selfless, choosing what’s best for their receiver. In terms of income, regardless of how much people earn, most still prefer to look out for themselves over the one who receives their funds. As for those who earn little to no income, they’re even less motivated to consider their recipient.

Why do people send money overseas?

People most commonly transfer money overseas to support family. This is followed by sending money as a gift, for a vacation, for an emergency, for business, to transfer funds to their own foreign accounts, to pay for their wedding and finally for shopping online. Other reasons Americans transfer money overseas include for charity, for a lover or for a friend.

Interestingly, our survey reveals that millennials (59%) are most likely to send money home to support their families over any other generation; Gen X came in at 54%, followed by 50% of baby boomers. Millennials are also more likely to send money overseas to fund their wedding, pay for a vacation, transfer to their own account and for business purposes, while Gen X is most likely to send money home for an emergency.

By marital status

Of those who are married or in a domestic relationship, 63% send money overseas for family support — 12 percentage points more than those who are single.

A full 40% of respondents who are separated say that a gift is their reason for sending a money transfer, and this group comprises the largest number (20%) of those citing business as a reason for sending funds. When it comes to emergencies, 50% of those who are widowed are sending money overseas due to unplanned urgent needs.

By income

In terms of supporting families, higher-income earners are more likely to do so than those earning less — with 31% of those with no income financially supporting their families — while double the proportion of people (62%) who earn between $75,000 and $100,000 send money home to their families.

Higher-income earners are also more generous when it comes to monetary gifts: 2 in 5 (40%) of those who earn $150,000 to $300,000 have sent money overseas as a gift, compared with 8% of those who have no income and 27% of those who earn up to $25,000 a year. The more money you have, the more likely you are to send money overseas to pay for a vacation, send money due to an emergency or to transfer money to your own account.

Senders compare before transferring money

How often do people shop around before making international payments? We looked at a survey we conducted in November 2016 with 2,005 US participants to find out. Of those that sent money transfers, 42% always compare money transfers before sending. An additional 32% often compare, and the remaining 26% said they always use their bank or the same provider every time.

Price-conscious millennials compare their options even more, with almost half (49%) saying they compare rates each time — nearly 2.5 times the percentage of those who use the same provider every time (20%). For baby boomers, loyalty outweighs the need to find a good deal, with 44% saying they are loyal to the same provider and 31% saying they always compare.

When broken down by gender, men (18%) are more likely than women (12%) to compare every time. Some senders compare online using a money transfer comparison tool like the one offered at finder.com, while others visit individual sites or even physical locations to make their decisions.

Hail for deciding factors: three case studies

What do people care about, whether they’re the sender or recipient? Olivia Chow, finder.com’s consumer trends expert, explains, “People often assume price is the only metric. But convenience and trust in the provider are just as important — sometimes more — when choosing a money transfer provider.”

To provide insight into the most popular reason people make cross-border payments, she reports on some of the key factors given by immigrant New York City Uber and taxi drivers when choosing a money transfer service for family support.

Case study #1: Hours of operation at the receiving end

Stephenson and his mother came to the U.S. from Haiti to leave behind the politics. Today, he sends money to his cousin, brother, and other family members. When asked which provider he uses, Stephenson says, “It depends when they are open for my family to go pick up the money.”

He uses MoneyGram when transferring funds to his cousin and Western Union for his brother. Stephenson prioritizes the convenience of those in Haiti who are picking it up, which makes the retailer’s hours of operation and their address the determining factors.

Case study #2: Access to customer support

Javet was the first of his family to emigrate from Indonesia 18 years ago. Most of his family have joined him since, but one sister remains in his motherland. His sister receives funds four times a year, but he doesn’t transfer funds directly to her. Rather, he transfers money to his brother in Ohio, who takes care of pooling resources and initiating the transfer altogether. To do so, his brother goes to Walmart, which has a partnership with MoneyGram. “Going to Walmart is just easier if something goes wrong,” he explains.

Case study #3: Alternative to international money transfer

Hassan is from Mali. He has a wife and three children in the U.S. but also three families back home. There, $300 a month allows them to live like royalty, he says. He used to send money through Western Union, but a family member began doing business sending goods between the U.S. and Mali. To avoid the fees, they’ve turned to the informal remittance sector: They now just package the cash with the exports, finding it cheaper and more reliable.

Chow concludes, “Whether or not the preferences of the sender outweighs the recipient’s, successfully getting the funds across borders tends to be a joint effort.”

Jennifer McDermott has been featured in Forbes, USA Today, Huffington Post, CBS and the Los Angeles Times. She is passionate about breaking down complex themes and providing actionable advice that empowers people to make better decisions about their money.

See full bio

There’s no true free B2B international money transfer service, but some are cheaper than others. See a side-by-side comparison of cost-effective options.

From bank transfers to specialist money transfer companies, there are several options available when you need to transfer money overseas from your bank account.

Xe is a leading company of currency solutions and it offers competitive international money transfer options to individuals and businesses around the world.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

from Haiti to leave behind the politics. Today, he sends money to his cousin, brother, and other family members. When asked which provider he uses, Stephenson says, “It depends when they are open for my family to go pick up the money.”

from Haiti to leave behind the politics. Today, he sends money to his cousin, brother, and other family members. When asked which provider he uses, Stephenson says, “It depends when they are open for my family to go pick up the money.”