Finder makes money from featured partners, but editorial opinions are our own.

Advertiser disclosure

There’s been a lot in the news about whether we’ll have a recession, when it might arrive and how long it could last. While economists have different definitions for it, a recession is a prolonged period of negative growth that can cause lower stock prices, layoffs and wage cuts.

Most agree we’re not technically in a recession since the US labor market remains healthy. However, if you’re feeling uneasy about the economy, “recession-proofing” your finances is an excellent way to prepare for any potential hardship.

Consider five ways to protect your income, boost your stability and reduce financial stress.

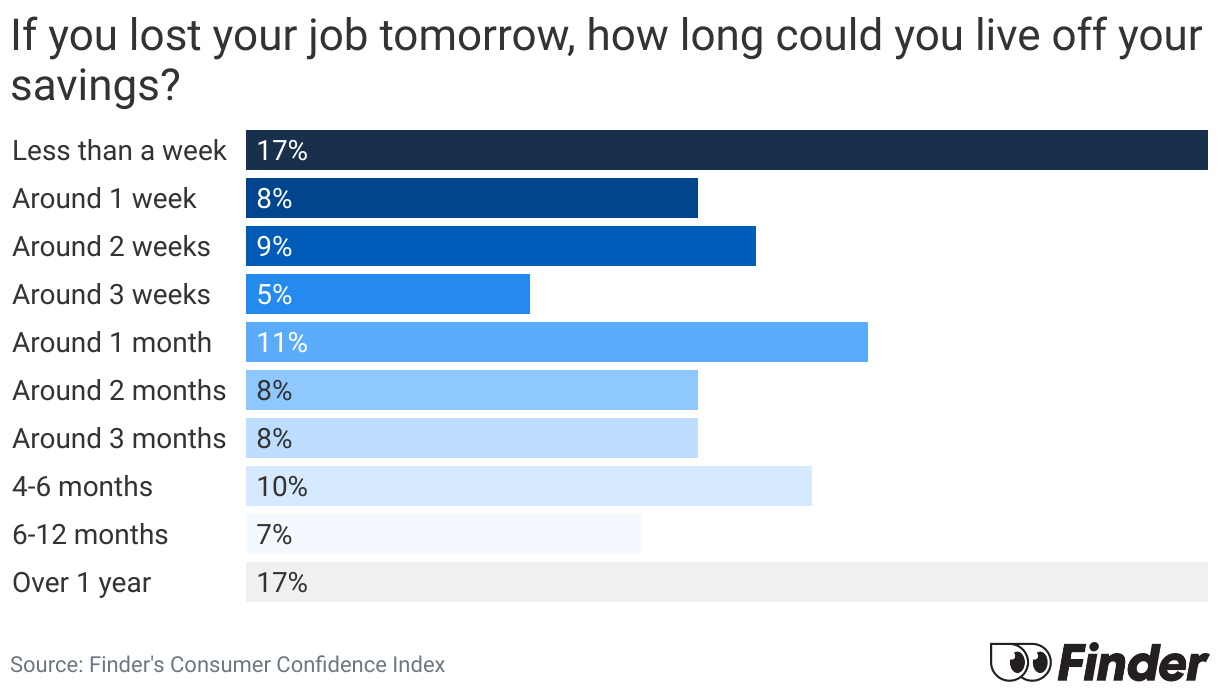

1. Increase your emergency fund.

According to Finder’s Consumer Confidence Index, 22% of Americans say they couldn’t live off their savings for more than a week if they lost their job tomorrow. While everyone should have emergency savings, it’s even more critical during a recession.

An excellent rule of thumb is to keep at least three to six months’ worth of your living expenses in an FDIC-insured high-yield savings account. However, depending on your and your family’s needs, you may need more or less. Another target is maintaining a minimum savings of 10% of your salary or household income.

A healthy cash cushion for unexpected hardships, such as losing your job or business income, should never be considered a luxury. A reserve gives you flexibility and can eliminate financial stress in an economic downturn.

2. Reduce high-interest debt.

Once you’ve got enough cash in the bank or are regularly saving for emergencies, review your debts. Make them your top priority if you have accounts charging high interest rates, such as credit cards or payday loans.

A balance transfer credit card can be an excellent solution for cutting your interest expense. You move your balance from a high-rate account to a new credit card that charges no or lower interest during a promotional period.

Not only does having less debt take the pressure off if you lose your job or get a pay cut during a recession, but eliminating high interest can free up funds for other purposes, such as retirement.

3. Have the right insurance.

An essential part of healthy finances is protecting it from potential risks, especially during uncertain times. Consider if you need the following insurance:

- Homeowners insurance is required by mortgage lenders and pays to repair or replace your home and belongings after a covered event, such as a natural disaster or theft, up to policy limits. It also covers your liability if you get involved in a lawsuit.

- Renters insurance pays to repair or replace your possessions damaged by a covered event. Note that landlords typically don’t insure your belongings or liability, so having a renters policy is a wise way to limit potential risk.

- Health insurance helps maintain your physical and financial health by limiting annual out-of-pocket medical expenses. Even if you’re young and healthy, an accident or illness could leave you with substantial medical bills.

- Disability insurance replaces a portion of your income, such as 60% or 70%, if you cannot work due to a covered illness or accident. Remember that health insurance doesn’t cover your living expenses if you can’t work due to a health problem.

- Life insurance pays your beneficiaries, such as a spouse, partner or children, after your death. It provides financial security for anyone who depends on you financially.

Remember that workplace insurance ends on the last day of the month if you lose your job during a recession unless you pay for COBRA continuation coverage.

4. Secure or increase your income.

If the economy struggles, an excellent way to recession-proof your finances is to increase your income or keep it as steady as possible. For instance, if you’ve always wanted an advanced degree, a real estate license or certification for a new career, consider pursuing it now.

Also, maintaining strong connections can set you up for success in a more competitive job market or help you find potential customers if you become self-employed.

5. Continue investing for retirement.

When the economy goes south, many people stop investing for retirement because they believe they can’t afford it. While it’s easy to get spooked by market volatility, don’t let it keep you from building a nest egg. Consider maximizing a tax-advantaged retirement account, such as a 401(k) or IRA, to build wealth and reduce taxes simultaneously.

Following these tips when times are good will put you in a solid financial position if there is a recession. It’s always a good time to reevaluate your finances and improve what you can.

About the Author

Laura Adams is a money expert and spokesperson for Finder. She’s one of the nation’s leading personal finance and business authorities. As an award-winning author and host of the top-rated Money Girl podcast since 2008, millions of readers, listeners, and loyal fans benefit from her practical advice. Laura is a trusted source for media and has been featured on most major news outlets, including ABC, Bloomberg, CBS, Consumer Reports, Forbes, Fortune, FOX, Money, MSN, NBC, NPR, NY Times, USA Today, US News, Wall Street Journal, Washington Post, and more. She received an MBA from the University of Florida and lives in Vero Beach, Florida. Her mission is to empower consumers to live healthy and rich lives by making the most of what they have, planning for the future, and making smart money decisions every day.

This article originally appeared on Finder.com and was syndicated by MediaFeed.org.

More resources on Finder

Ask a question