Finder maintains full editorial independence to ensure for our readers a fair assessment of the products, brands, and services we write about. That independence helps us maintain our reader's trust, which is what keeps you coming back to our site. We uphold a rigorous editorial process that ensures what we write and publish is fair, accurate, and trustworthy — and not influenced by how we make money.

We're committed to empowering our readers to make sound and often unfamiliar financial decisions.

We break down and digest information information about a topic, product, brand or service to help our readers find what they're looking for — whether that's saving money, getting better rewards or simply learning something new — and cover any questions you might not have even thought of yet. We do this by leading with empathy, leaning on plain and conversational language that speaks directly, without speaking down.

Employer-sponsored retirement plans like the 401(k) offer some of the best ways to save for retirement. Contributions are automatic, contribution limits are relatively high and employer matches can help grow your money faster.

But sometimes, it makes sense to move the money from your employer’s retirement plan to an individual retirement account (IRA). Known as a rollover IRA, let’s explore when you might consider a rollover and what you need to do to complete the process.

What is a rollover IRA?

A rollover IRA offers a non-taxable and penalty-free way to transfer money to an IRA from an old employer-sponsored retirement plan, such as a 401(k), 403(b) or 457(b). A rollover IRA preserves your money’s tax-deferred status and lets you still make contributions toward your retirement without paying taxes on the distribution or early withdrawal penalties at the time of transfer.

Why choose a rollover IRA?

You might consider a rollover IRA if you’re in a 401(k) or other employer-sponsored retirement plan with limited investment choices and high fees or want to consolidate and track your retirement money in one place. Another reason to choose a rollover IRA is if you’ve left an employer, either through a job change or retirement.

Compared to a 401(k), which primarily invests in mutual funds, rollover IRAs can offer access to more securities with few or no fees. For example, the average equity mutual fund expense ratio was 0.40% in 2025, whereas the average index equity exchange-traded fund (ETF) expense ratio was 0.14%.(1) The exact costs and fees depend on your investment choices, so compare the fees of what you might invest in to your current holdings in your employer retirement plan before making the transfer.

How to roll over an employer-sponsored retirement plan to an IRA in 4 steps

If you’re ready to roll over your 401(k) or another employer-sponsored retirement plan to an IRA, you have a few steps to complete. The process is generally straightforward once you choose an IRA provider and consider the tax implications of your options.

1. Choose a rollover IRA account type

If you don’t already have an IRA, you’ll need to open one. Transferring to an IRA of the same structure — pre-tax 401(k) to pre-tax IRA or Roth 401(k) to Roth IRA — is the easiest way, as it preserves the tax structure of the money. Here are the IRAs you should consider for your rollover depending on the money in your old retirement plan:

If your account has …

Then consider …

Only pre-tax contributions

Opening a traditional IRA

Both pre-tax contributions AND post-tax contributions

Opening a traditional IRA for the pre-tax money AND a Roth IRA for the post-tax money

Only post-tax contributions

Opening a Roth IRA

Pre-tax contributions, but you would like to convert your money into post-tax contributions

Opening a Roth IRA, but know that rolling pre-tax money into a Roth IRA is a Roth conversion and is a taxable event

2. Compare and select an IRA provider

Banks, brokers and other financial institutions can act as IRA custodians, but not all accept rollover contributions.

In choosing an IRA provider, consider who you want to invest the money in your rollover IRA: you or a financial advisor. If you want to take a hands-on approach to building your portfolio and pick stocks and other investments, a regular IRA will do. However, if you want professional help to determine your investment plan or manage your portfolio on your behalf, you might consider an IRA provider that offers financial advisory services, whether that’s from a human or robo-advisor. A robo-advisor is an algorithm that constructs and manages an investment portfolio on your behalf based on your responses to questions about your financial goals, time horizon and risk tolerance.

3. Contact your old retirement plan provider and request a rollover

You need to contact your retirement plan provider to request a rollover. If you’re unsure who your old 401(k), 403(b) or 457(b) provider is, the name should be on your account statements. If you can’t access your account statements, consider a 401(k) search service like Beagle to locate all your old 401(k)s.

Call your old plan provider or initiate the rollover process online. You’ll need to complete paperwork, and different providers may require different documents. You then have two options to complete the rollover:

Direct rollover. Your old retirement plan servicer makes the payment directly to your rollover IRA provider. You’ll need to supply the name of your rollover IRA provider and your rollover IRA account number.

60-day rollover. Your old retirement plan provider issues the payment to you, less a mandatory 20% withholding for taxes, and you deposit all or a portion of the funds in your rollover IRA within 60 days. You will need to make up the 20% that was withheld when you deposit the money to avoid paying taxes. If you fail to deposit the money within 60 days, your retirement funds will be subject to income taxes and a 10% penalty if you’re under the age of 59.5. A check sent to you that’s payable to the rollover IRA provider is not subject to taxes.(2)

4. Invest the money

The rollover process technically ends once the money is deposited into your IRA. However, unless you choose a financial advisor or robo-advisor to manage your IRA, you’ll need to invest your money.

Review your asset allocation across your entire investment portfolio — all your IRAs and employer-sponsored retirement plans — to determine what securities to purchase. Many financial experts recommend a portfolio of 60% stocks and 40% bonds. However, an optimal portfolio allocation for you will depend on your age, risk tolerance and financial goals.

Rollover IRA considerations

Before initiating a rollover IRA, consider the tax structure of the money you’re transferring so you aren’t surprised by any tax consequences that may come in the process. Unless you want to convert pre-tax contributions to post-tax contributions, roll over pre-tax funds to a traditional IRA and post-tax funds to a Roth IRA. A direct rollover, where your old plan provider sends the money directly to your rollover IRA provider, will let you avoid taxes and penalties on the transfer.

There’s no limit to how much you can roll over into an IRA. Rolling over funds from an old employer-sponsored retirement plan to an IRA does not affect your annual IRA contribution limit.(3)

What else you can do with an old 401(k) or retirement plan

A rollover IRA is one option you have when it comes to managing the money in your old employer-sponsored retirement plan. Depending on your situation, you may consider these other options:

Leave the money where it is. If your previous employer’s 401(k) or other retirement plan lets you maintain your account after leaving your job and you’re satisfied with the plan’s investment options, you can leave the money alone.

Roll it into a new retirement plan. If you’ve started a new job that offers a retirement plan and the new provider accepts rollover contributions, you can consolidate your employer-sponsored retirement plans under one roof.

Cash it out. You can cash out your retirement plan, but the IRS will tax the distribution, and you may incur early withdrawal penalties. Your money will also lose any future compound growth, which can significantly impact your ability to reach your retirement goals.

Compare brokerages that offer IRA accounts

Narrow down top brokers by annual fee, stock trade fee and more to find the best for your budget and financial goals.

7 of 7 results

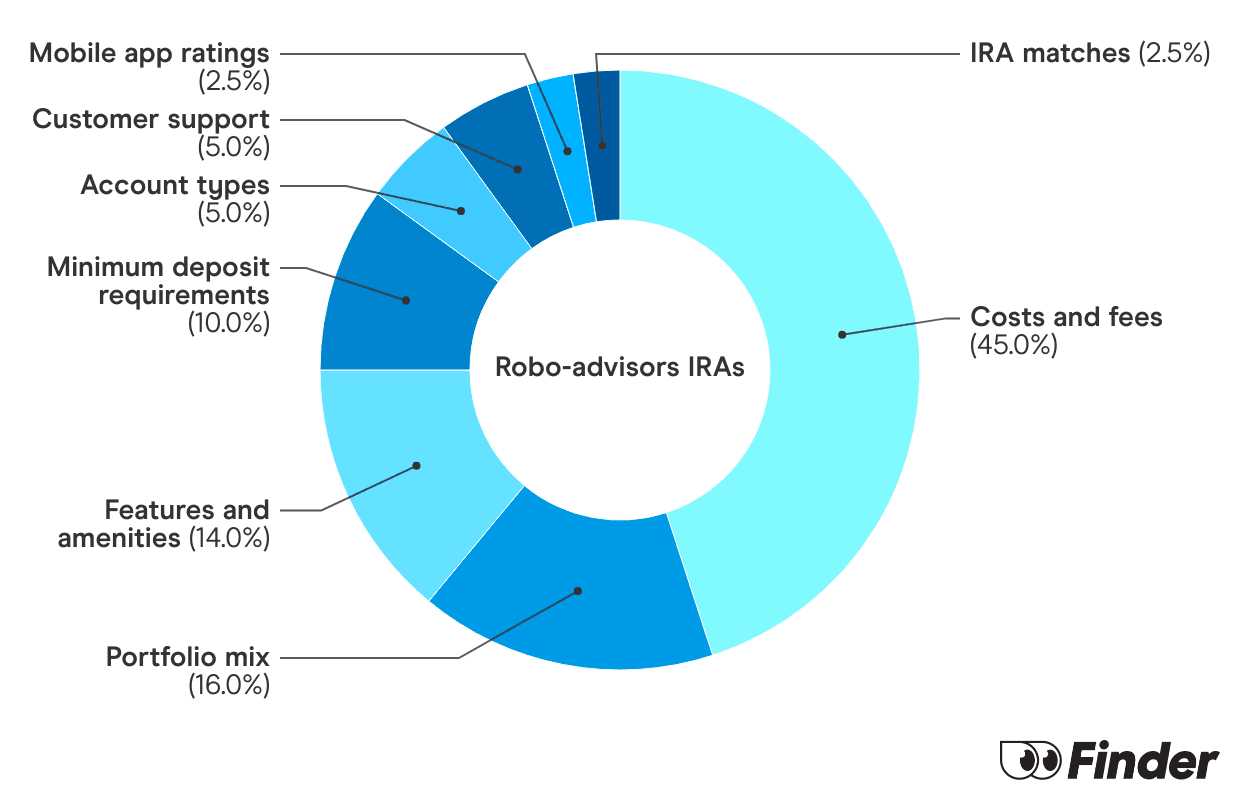

What is the Finder Score?

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Bottom line

A rollover IRA lets you transfer money from an old employer-sponsored retirement plan such as a 401(k), 403(b) or 457(b) to an IRA without taxes or penalties. This can be a good idea if you want more flexible investment options or to consolidate your retirement money in one account after leaving a job. But stick with an IRA of the same tax structure to avoid paying taxes on the rollover.

Not all IRA providers accept rollover contributions, so compare the best Roth IRA accounts and the best IRA accounts to see which provider offers rollover IRAs and the services you’re interested in.

Frequently asked questions

A rollover IRA is the process of moving an old employer-sponsored retirement plan, such as a 401(k), to an IRA and maintaining the account's tax-deferred status.

A rollover IRA may be a good option if you've left your employer and want to manage all your retirement money in one place. A rollover IRA might also be a good option if you want more flexibility in terms of investment options.

A direct rollover, where your old retirement plan issues the payment directly to your rollover IRA provider, is the best way to roll over funds to an IRA without penalty.

A rollover IRA can be structured as a traditional IRA, where the account is funded with pre-tax dollars.

Matt Miczulski is an investments editor and market analyst at Finder. With over 450 bylines, Matt dissects and reviews brokers and investing platforms to expose perks and pain points, explores investment products and concepts and covers market news, making investing more accessible and helping readers to make informed financial decisions.

Before joining Finder in 2021, Matt covered everything from finance news and banking to debt and travel for FinanceBuzz. His expertise and analysis on investing and other financial topics has been featured on Yahoo Finance, CBS, MSN, Best Company and Consolidated Credit, among others. Matt holds a BA in history from William Paterson University.

See full bio

Matt's expertise

Matt

has written

282

Finder guides across topics including:

Invest in your retirement while enjoying tax breaks and peace of mind.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.