Both individual retirement accounts (IRAs) and 401(k)s are types of tax-advantaged investment accounts individuals use to save for retirement. But they aren’t interchangeable. Find out the differences between these two valuable retirement accounts and the advantages and disadvantages of each.

IRA vs. 401(k) at a glance

IRAs and 401(k)s are two types of tax-advantaged retirement accounts, but individuals open IRAs, whereas employers offer 401(k)s.

The 2026 IRA contribution limit is $7,500, and the 401(k) contribution limit is $24,500.

IRAs let you invest in most assets, while 401(k)s are limited mostly to mutual funds.

IRA vs. 401(k): What’s the difference?

IRAs and 401(k)s are the two main types of retirement accounts in the US. Roughly 44% of US households owned an IRA as of mid-2024, according to the Investment Company Institute (ICI), up from 34% a decade earlier.(1)

Both types of accounts are tax-advantaged, meaning they offer tax benefits for setting aside money for retirement. The main differences between these two types of retirement accounts are:

Employers offer 401(k)s, whereas individuals open IRAs on their own.

IRAs offer a greater selection of investments than most 401(k)s.

Savers can’t contribute nearly as much to an IRA as they can to a 401(k). The IRA contribution limit for 2026 is $7,500 ($8,600 if you’re age 50 or older), while 401(k) contributions top out at $24,500 ($32,500 if you’re age 50 or older).(2)

401(k)

Roth IRA

Traditional IRA

Who it’s for

You want to take advantage of employer-matching contributions

You want to pay taxes on a smaller portion of your salary since your contributions lower your taxable income

You want to invest passively through automatic elective-deferral contributions

You’ve maxed out your IRA

You’re under the income limit threshold to save in a Roth IRA

You think you’ll be in a higher income tax bracket in retirement

You don’t want mandatory withdrawals in retirement

You earn more today and think you’ll be in a lower tax bracket in retirement

You make too much money for a Roth IRA

You want an immediate tax break

Max contribution per year

$24,500 ($32,500 if you’re age 50 or older)

$7,500 ($8,600 if you’re age 50 or older)

$7,500 ($8,600 if you’re age 50 or older)

Are contributions tax-deductible?

No, you can’t take a deduction on your tax return, but your contributions automatically lower your taxable income

No

Yes

What is an IRA?

An IRA is a tax-advantaged investment account individuals can use to save for retirement. Congress created the IRA in 1974 to provide workers without an employer-sponsored retirement plan with a means to set aside money for retirement.

Unlike the 401(k), individuals open IRAs on their own. They come in several types, but the two most common are the traditional IRA and Roth IRA. Most major banks and brokerages offer these retirement accounts, and anyone with earned income can open one.

Compared to a 401(k), IRAs let you invest in most assets. These include:

Through a self-directed IRA, which offers even greater flexibility in terms of permitted investments, you can invest your retirement funds in alternative assets. Examples of alternative assets include real estate, cryptocurrencies and commodities like physical gold.

IRAs come in two main types: traditional and Roth. Other types of IRAs include SEP and SIMPLE IRAs, though these are facilitated by business owners.

You can have a traditional IRA, a Roth IRA, or both, but your total contributions across both are capped at $7,500 in 2026.

Traditional IRA

Traditional IRAs are funded with pre-tax dollars, and contributions to this type of account are typically tax-deductible. The amount you can deduct depends on whether you or your spouse participates in a retirement plan at work. Come retirement, you pay taxes on both your contributions and the earnings on your investments.

Traditional IRAs have no income limits, but, like traditional 401(k)s, they do have RMDs. You’re required to begin taking distributions from your IRA at age 73 if you were born between 1951 and 1959, or at age 75 if you were born in 1960 or later.(3)

Roth IRA

Contributions made to a Roth IRA are made with after-tax dollars, and contributions to this type of account are not tax-deductible.

However, since you already paid taxes on the money, you can withdraw your contributions at any time without taxes or penalties. And when you take qualified distributions of earnings from your Roth IRA, you do not have to pay taxes on the withdrawals. Aside from certain exceptions, a distribution is considered qualified when you reach the age of 59 and a half and have held your Roth IRA for at least five years.

Roth IRAs do not have RMDs, so you’re not required to make withdrawals at any point.

In 2026, you can contribute up to $7,500 ($8,600 if you’re 50 or older) total across both your traditional and Roth IRAs.(2)

While traditional IRAs have no income limits, you’re limited to how much you can contribute (or if you can contribute at all) to a Roth IRA based on your modified adjusted gross income. For example, married couples filing jointly with a MAGI of $242,000 or less can make a full Roth IRA contribution in 2026; the amount phases out between $242,000 and $252,000, and contributions aren’t allowed above $252,000.(2)

IRA pros and cons

Pros

Traditional IRA contributions are tax-deductible

Qualified Roth IRA withdrawals are tax-free

Anyone with earned income can contribute to an IRA

Wide range of investment options

Cons

Roth IRAs have income limits

Relatively low contribution limits

Early withdrawal penalties apply

Required minimum distributions for traditional IRAs starting at 73 or 75, depending on your birth year

Compare brokers that offer retirement accounts

Narrow down top brokers by annual fee, stock trade fee and more to find the best for your budget and financial goals.

3 of 7 results

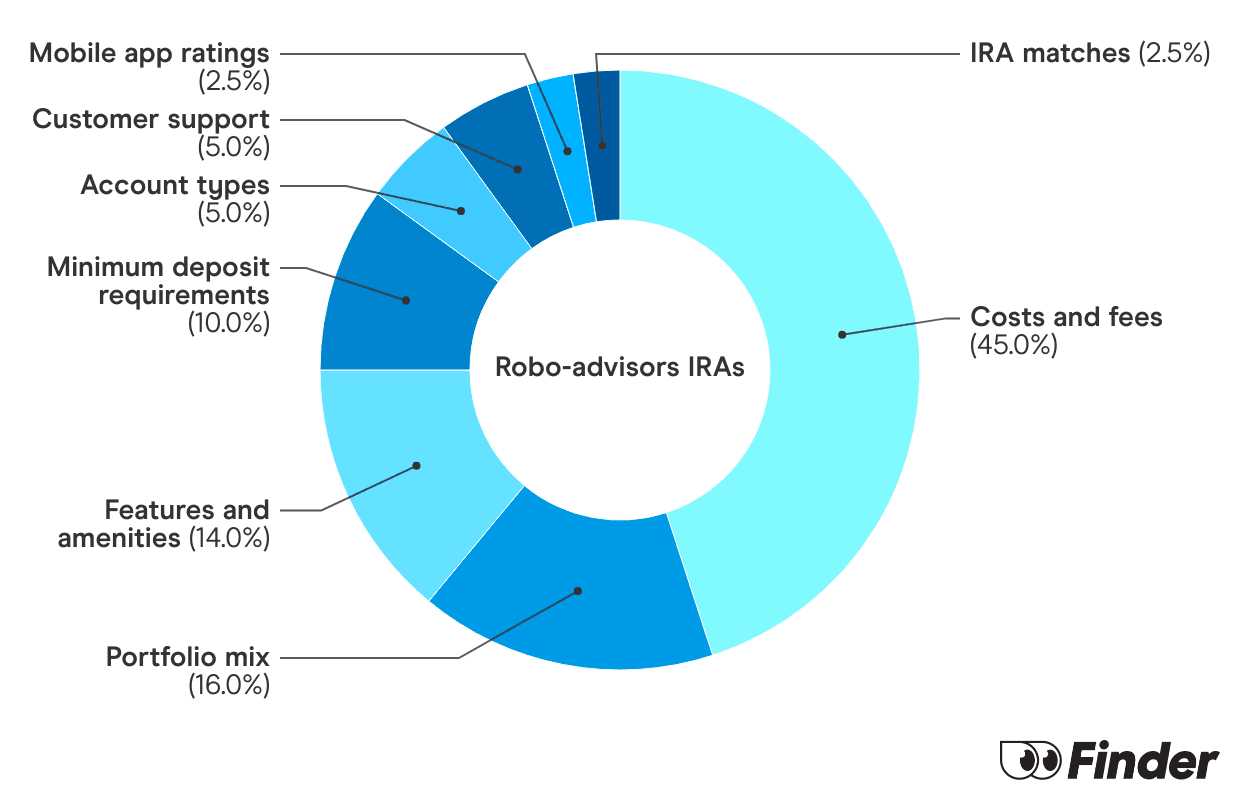

What is the Finder Score?

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

What is a 401(k)?

A 401(k) is a retirement plan employers offer that qualifies for tax breaks under the Internal Revenue Code (IRC).

Employees contribute to a 401(k) via elective deferral, meaning a percentage of their salary is withheld and contributed to the account each pay period. Employers can also contribute to employees’ accounts.

There are two types of 401(k) accounts: traditional 401(k)s and Roth 401(k)s. It’s possible to split your contributions between both, but the maximum you can contribute is $24,500 for 2026 ($32,500 if you’re age 50 or older).(2)

The two most common types of 401(k)s are traditional and Roth 401(k)s. However, there are also safe harbor 401(k)s, SIMPLE 401(k)s and solo 401(k)s.

Here’s more on the two most common types.

Traditional 401(k)

Traditional 401(k) contributions are made using pre-tax dollars. While you don’t claim a tax deduction for your 401(k) contributions when you file your taxes, your contributions reduce your overall tax liability at the end of the year.

Your contributions and any earnings from your investments are tax-deferred. That means you pay taxes on contributions and earnings when you withdraw money at retirement. You can begin withdrawing money from your 401(k) without penalty once you reach age 59 and a half. Distributions before the age of 59 and a half will incur a 10% early withdrawal penalty.

Traditional 401(k)s also have required minimum distributions (RMDs). You’re required to start taking distributions at age 73 if you were born between 1951 and 1959, or at age 75 if you were born in 1960 or later.(3)

Roth 401(k)

A Roth 401(k) is similar to a traditional 401(k), but employee contributions are not tax-deferred. They’re made with after-tax dollars — money you’ve already paid taxes on. Because of this, you can withdraw contributions at any time, tax- and penalty-free. Meanwhile, you can withdraw the earnings you’ve made on your investments tax-free after the age of 59 and a half.

Historically, employer matching contributions were made with pre-tax money and held in a traditional 401(k), even if your own contributions went into a Roth 401(k). Since SECURE 2.0, plans can optionally let fully vested employees elect to have employer matching and nonelective contributions treated as Roth instead — though this remains up to the employer to offer, and electing it means paying tax on that employer contribution in the year it’s made.(4) Unlike traditional 401(k)s, Roth 401(k)s have had no lifetime RMDs since 2024.(3)

d41666c6-f9bf-4b8f-8a0e-9850e2f6067c-Comprehensive 401(k) search service

Comprehensive 401(k) search service

Find all your old 401(k)s and their hidden fees

Borrow from your Beagle 401(k) or IRA with 0% net interest

Robo-advisor available if you roll over your 401(k) to Beagle

Employee contributions

Employees can contribute up to $24,500 ($32,500 if you’re age 50 or older) per year to their 401(k)s. Employee contributions to a traditional 401(k) are made with pre-tax dollars, while contributions to Roth 401(k)s are made with post-tax funds.

Employer matching contributions

Many employers offer matching contributions for their employees’ 401(k)s. These are often dollar-for-dollar matches up to a certain percentage of your salary. For example, your employer may match 100% of your contributions up to, say, 3% of your salary. If you make $50,000 per year and contribute $1,500 (3% of $50,000) to your 401(k), your employer would also contribute $1,500 on your behalf.

The 401(k) contribution limit is $72,000 for combined employee and employer contributions in 2026.(2)

401(k) withdrawals

Qualified distributions from a 401(k) are allowed after you reach the age of 59 and a half. Distributions from a traditional 401(k) will be subject to federal income tax, while Roth 401(k) distributions will be tax-free, provided you’ve held the Roth 401(k) for at least five years.

If you take a distribution from either 401(k) type before you’re 59 and a half years old, you’ll have to pay an additional 10% penalty unless an exception applies. Total and permanent disability is one such exception. Preventing eviction or foreclosure on your home qualifies as a reason for a hardship withdrawal, but a hardship withdrawal alone doesn’t waive the 10% penalty — it only does if the withdrawal also qualifies under a separate exception, such as SECURE 2.0’s emergency personal expense provision, which allows one penalty-free withdrawal of up to $1,000 per year if your plan has adopted it.(5) If you withdraw funds from a Roth 401(k) before the age of 59 and a half and before you’ve held the account for at least five years, you’ll have to pay both income taxes and the 10% early-withdrawal penalty.

401(k) pros and cons

Pros

Many employers offer matching contributions

Relatively high annual contribution limit

Tax benefits

Elective deferrals offer a great way to passively invest

Cons

Your employer may not offer a 401(k)

Limited investment options

Must pay expense ratios and potentially other fees with most mutual funds

Early withdrawal penalties apply

Frequently asked questions about 401(k)s vs. IRAs

A traditional IRA isn't necessarily better than a 401(k). Each has its own unique advantages and disadvantages. When choosing to open either a traditional IRA or a 401(k), it's best to consider your financial situation and your retirement goals to determine which account best suits your needs.

A self-directed IRA can be a good idea if you want to hold alternative assets, like real estate, precious metals or cryptocurrency, in a tax-advantaged retirement account and you're comfortable researching and managing those investments yourself. They typically come with higher fees and more complexity than a standard IRA, so they tend to suit experienced investors rather than beginners.

One advantage of an IRA over a 401(k) is that you can open and manage an IRA on your own. You may not work at a job that offers a 401(k). If this is the case, IRAs still let you save for retirement in a tax-advantaged manner.

Another advantage of an IRA over a 401(k) is that IRAs offer a broader range of investment options. With an IRA, you can invest in stocks, bonds, CDs, ETFs and more. However, with a 401(k), you often only get to select from a handful of mutual funds.

An IRA can complement a 401(k), especially if you want to reduce your tax burden once you retire. For example, you may have a lot of money saved in a traditional 401(k) and will have to pay taxes on the withdrawals you make in retirement. In this case, you could start saving more in a Roth IRA, as this account allows you to take withdrawals tax-free in retirement. Doing so lessens the taxes you'll have to pay once you retire.

Frank Corva is business-to-business (B2B) correspondent for Bitcoin Magazine and formerly the cryptocurrency writer and analyst for digital assets at Finder. Frank has turned his hobby of studying and writing about crypto into a career with a mission of educating the world about this burgeoning sector of finance. He worked in Ghana and Venezuela before earning a degree in applied linguistics at Teachers College, Columbia University. He also taught writing and entertainment business courses in Japan and worked with UNICEF in Namibia before returning to the US to teach at universities in New York City. Earlier in his career, he spent years working as a publicist and graphic designer for record labels like Warner Music Group and Triple Crown Records. During that time, he was also a music journalist whose writing and photography was in published in Alternative Press, Spin and other outlets.

See full bio

Invest in your retirement while enjoying tax breaks and peace of mind.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.