Flat-rate fees are on par with competitors, but premium tiers are expensive.

Minimum deposit requirement

★★★★★5/5

There are no minimum deposit requirements for any of its service tiers.

Account selection

★★★★★5/5

Blooom is equipped to manage a wide range of investment accounts.

Tax advantages

★★★★★2/5

It supports retirement accounts but doesn’t offer tax-loss harvesting.

Customer support

★★★★★2.5/5

Support is only available by email — unless you’re a premium user.

Customer feedback

★★★★★3/5

Very little feedback is available for this platform.

To learn how our star ratings are calculated, read the methodology at the bottom of the page.

How does Blooom work?

Blooom provides basic recommendations on how to diversify your account, including the percentage of large-cap, mid-cap and small-cap U.S. equity it thinks you should hold. International and emerging market equity estimates are also included, along with real estate, commodities, and long- to intermediate-term bonds. Finally, Blooom provides a fee target, to help investors determine how much they should pay for their investments. The service also provides portfolio rebalancing. Accounts are reviewed within three months of an adjustment to determine if another shuffling of assets is needed.

How easy is it to use?

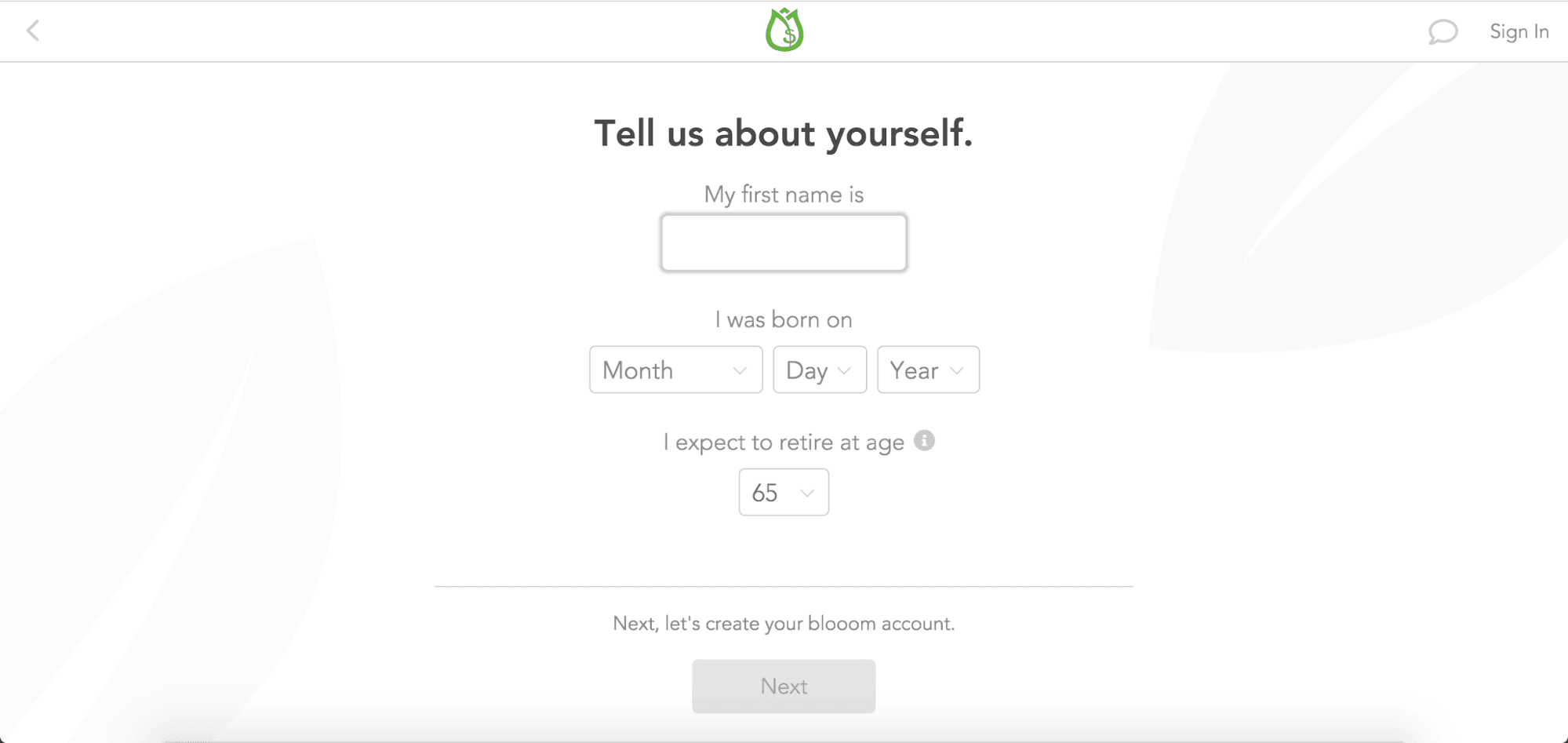

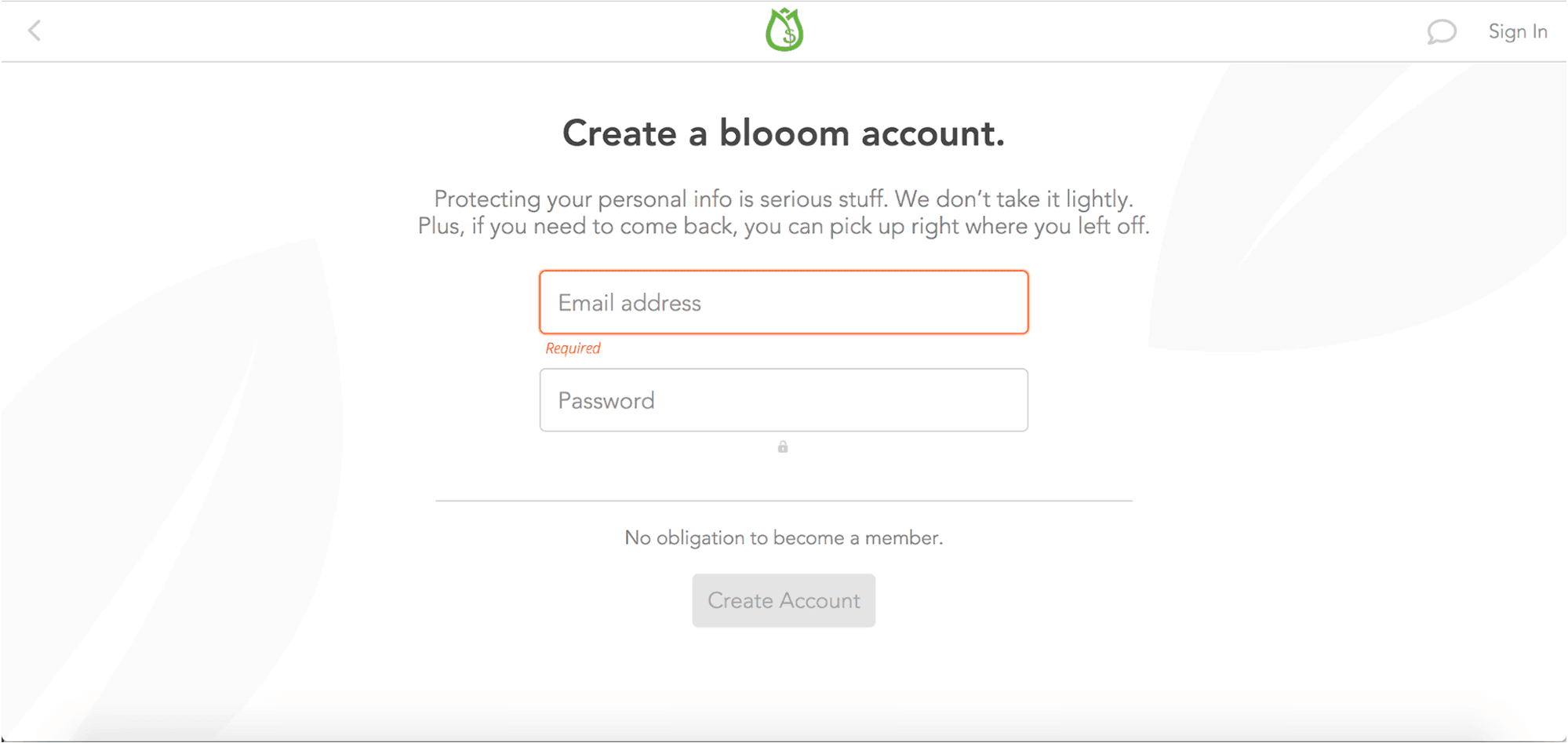

Blooom is easy to navigate and signing up only takes a couple of minutes. After entering your email address and creating a password, you’ll be asked to enter your age and the age you want to retire. After that, you’ll be asked to answer a five-question risk assessment to help you assess your risk tolerance. Once you’ve entered your information and answered Blooom’s questionnaire, you’ll receive basic recommendations about how to best diversify your portfolio. From here, you have the option to buy into one of Blooom’s paid service plans.

Who is Blooom Financial Planning best for?

Blooom differentiates itself from other robo-advisors by creating and managing portfolios that are specifically designed for retirement planning. It’s typically best suited for:

Investors with employer-sponsored plans. Blooom only works with employer-sponsored plans like 401(k), 403(b), 401(a), 457 and TSP, so you’ll need to create a plan if you don’t already have one.

Hands-off investors. While you’ll still have control of your plan, Blooom is designed to let customers sit back while the company does all the research, investing, management and rebalancing.

How does it approach investing?

Blooom’s straightforward approach allows customers to get a quick analysis of their retirement plan before moving forward with their investments:

Start. Answer a few introductory questions, set up a password and connect your existing retirement account.

Analyze. Get a free analysis of your investments and the adjustments Blooom would make, along with a breakdown of the potential fees you could save.

Sign up. If you’re satisfied with the service, you can sign up and set up an account to start investing with Blooom.

Invest. Blooom will develop a personalized investment strategy based on research and diversification, then build your portfolio according to your situation.

Manage. Your portfolio will be managed and adjusted by Blooom, and you can log in any time to get a simple or in-depth look at your investments.

How does the free analysis work?

Before you commit to a paid Blooom plan, you can use the service’s free analysis tool to assess your portfolio. Start by creating an account with a username and password. Next, answer some questions about your investment habits and goals. Complete the process by securely linking your employer-sponsored retirement account. Blooom combs through your funds and delivers a personalized analysis of your portfolio. This analysis offers suggestions for portfolio diversification and asset allocation to help you get the most out of your money. If you like what you see, you can sign up for one of Blooom’s paid plans.

Prices and fees

Blooom offers its initial portfolio analysis for free. But for an annual fee, it will manage your portfolio for you. Its bare-bones Essentials account starts at $45 annually, offering personalized portfolio allocation but not much else. The Standard account is $120 per year and comes with access to a financial advisor and active account alerts. For $250 annually, you can add as many accounts as you’d like and gain priority access to a financial advisor. You can drop any of Blooom’s plans whenever you’d like without a cancellation fee.

Essentials

Standard

Unlimited

Annual fee

$45 per account

$120 per account

$250

Features

Personalized portfolio allocation

Personalized portfolio allocation

Placing trades

Withdrawal alerts

Access to a financial advisor

Personalized portfolio allocation

Placing trades

Withdrawal alerts

Unlimited accounts

Priority access to a financial advisor

Blooom can be proportionately expensive for beginning investors. If you have only $2,000 saved, its standard tier at $120 a year means you’re paying a 6% fee for its services. Of course, Blooom becomes a better deal as your assets grow. For instance, if you have $400,000 in retirement assets, Blooom’s Standard account works out to 0.03% in annual fees — or a minuscule three one-hundredths of 1% of your assets.

Is Blooom legit?

Blooom was founded in 2013 and is headquartered in Leawood, Kansas. By 2016, it announced that it had $300 million under management and a former FDIC chair serving as its first advisory board member. Blooom is a fiduciary financial advisor – which means it is legally obligated to act in its clients’ best interests. This is in contrast to a non-fiduciary financial advisor — as you might find at your local bank or mortgage provider — which is held to lower standards. Non-fiduciary advisors might recommend investments that are better for their wallet (through compensation arrangements) than your wallet. A fiduciary is compelled by federal law to act in your interest. Blooom announced that it had $4 billion under management as of September 29, 2020. That’s not bad for a startup, but it’s a pittance compared to financial giants. Fidelity, for instance, reports $8.3 trillion in assets under management — nearly 2,100 times as much.

What are the benefits of Blooom Financial Planning?

Many robo-advisors help you invest and manage your money, but Blooom’s retirement-focused plans stand out for a number of reasons:

Stay in control. While Blooom will build and manage your portfolio for you, you’ll still be able to make adjustments on your own.

Financial advice. You can get financial advice whenever you need it, even on investments outside of Blooom.

Free analysis and personalized plans. Answer a questionnaire to get a free investment analysis, then sign up to get a personalized investment plan.

Flat, transparent fees. Unlike many robo-advisors, Blooom only charges a flat fee. Plus, fees are paid from your debit or credit to avoid cutting into your earnings.

No account minimums. You can start investing with Blooom no matter how much you have saved.

No conflict of interest. Blooom is a fiduciary and is not associated with any of your investments, so it will only suggest funds that actually benefit you.

What can Blooom’s advisors help with?

Blooom’s financial advisors don’t just provide retirement guidance — they can help you assess your day-to-day finances, too. By filling out a secure online form on Blooom’s website, you’ll be connected with one of Blooom’s human advisors, able to field questions about milestone purchases, debt, budgets and more. You can also connect with one of Bloom’s advisors through the live chat feature after signing up for one of its paid plans.

What to watch out for

Blooom could be an effective way to build up your retirement savings, but there are still a few things you should watch out for:

Employer-sponsored plans only. Blooom only works with 401(k), 403(b), 401(a), 457 and TSP plans.

Limited support. Blooom doesn’t have brick-and-mortar branches for in-person help. And, it only offers live chat with an advisor to premium account holders.

High fees for low balances. Blooom’s flat fee will have little impact on larger balances, but could account for a higher percentage of accounts with lower balances.

Stock-heavy investments. Blooom tends to invest heavily in stocks — so if that differs from your preferred investment style, it may not be right for you.

Doesn’t consider other investments. Your other investments won’t be considered when creating your portfolio, which could be an issue since retirement accounts are often only a portion of a long-term financial strategy.

Blooom reviews and complaints

Customer feedback on Blooom is scarce. On its Better Business Bureau (BBB) page, it sports an A+ rating but lacks accreditation status. As of March 2022, only one official BBB complaint was filed against the platform but the details of the complaint are unavailable. Four reviews on its Trustpilot page rank it 3.7 out of 5 stars, and it has no complaints on the Consumer Financial Protection Bureau. On Reddit, a few Blooom investors expressed frustration with the platform, citing a low frequency of rebalancing that resulted in portfolio losses.

How do I get started?

Creating a Blooom account is free and the entire process takes less than two minutes. Anyone with a self-directed retirement plan — like an IRA or 401(k) can sign up.

Visit the Blooom website and click Start now.

Enter your name, birth date and expected age of retirement, then click Next.

Enter your email address and create a password, then click Create account.

Answer questions about your existing accounts and investment preferences and click Next.

View your recommended mix of stocks and bonds, then link your account if you’re satisfied.

View your analysis and recommended adjustments then submit your application.

Required information

Name

Birthdate

Address

Email address

Social Security number

Employment information

State-issued ID

Eligibility

Be at least 18 years old

Have a valid state-issued ID

Have a valid Social Security number

Have an employer-sponsored retirement plan

In order to create an accurate financial strategy, you’ll be asked for the following information:

Risk tolerance

Investment goals

Expected retirement age

How do I contact Blooom support?

A downside of this robo-advisor is its limited support options:

Email. Bloom promises a response to email within three business days.

Live chat. If you pay for a Premium membership, you can chat with a rep live online on weekdays from 10 a.m. to 5 p.m. ET.

Bottom line

Blooom might make sense if you are serious about saving for retirement but unsure how to properly allocate your money. However, its $120 standard annual fee could be a heavy burden for smaller portfolios. And more experienced investors may be better off doing their own research and asset allocation. If you’re still not sure if Blooom is right for you, you can compare other financial planning options to see what else is out there.

For a limited time, NextSeed is waiving fees to open an IRA along with annual fees on new accounts. Normally, partner bank GoldStar charges $25 to open the account. It also charges a $64 annual fee and $100 account closing fee.

Yes. You'll still maintain control of your portfolio, so you can make additional trades whenever you'd like.

A fiduciary is a person who's legally responsible for another person's assets and is obligated to make financial decisions that would benefit you.

No. Blooom is simply an advisory and management service, so transferring your account is unnecessary.

Yes. You can open your own retirement account to get started with Blooom.

How we rate trading platforms

★★★★★5/5 — Excellent

★★★★★4/5 — Good

★★★★★3/5 — Average

★★★★★2/5 — Subpar

★★★★★1/5 — Poor

We analyze top online trading platforms and rate them one to five stars based on factors that are most important to you. These factors include fees, securities available for trade, customer support, customer feedback, platform resources and overall reliability. For a complete breakdown of how we score each category, read the full methodology of how we rate robo-advisors.

Blooom is not currently available on Finder

Have you considered Tastytrade?

Competitive, capped options commissions, with a reliable trading platform designed for serious traders.

Trade options, futures, options on futures, stocks, ETFs

Peter Carleton is a freelance writer that covers banking and investing, breaking down what you need to know about where you put your money. When Peter's not thinking about cutting-edge banking apps and robo-advisors, he runs a creative agency and spends his spare time cooking or reading. See full bio

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Advertiser Disclosure

finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which finder.com receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. finder.com compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.