Chase First Banking℠

- $0 monthly fee

- Financial learning tools for kids

- Flexible parental controls

- Supports chores and allowances

- For kids ages 6 to 17

- FDIC insured

JPMorgan Chase Bank, N.A. Member FDIC

On the hunt for a kids’ debit card that won’t charge you a monthly fee? We compare the best debit cards designed for children and their parents to showcase the best no-fee options. We chose the best cards based on features that matter most to families, like parental controls, savings goals and learning tools. Every card on this list charges no monthly fee and is designed to help your child spend and save safely, and each has FDIC insurance on deposits.

Chase First Banking℠

Step

Current teen banking

These debit cards for kids and teens have no monthly fees, and we specifically chose them for their standout features, safety controls and extra perks.

| Kids’ card | Best for | Age range | Monthly fee | ATM fees | Learn more |

|---|---|---|---|---|---|

| Chase First Banking | Parental controls | 6 to 17 | $0 | at Chase ATMs, $3 out-of-network ATM fee | |

| Step | Credit building | Any | $0 | $0 ATM fees (operator fees may apply) | |

| Current Teen Banking | Saving features | 13 and up | $0 | $0 in network, $2.50 out-of-network ATM fee | |

| Modak Makers | Cash-redeemable rewards | Any | $0 | None, doesn’t allow ATM access | |

| Capital One TEEN Money | Zelle access | 8 and up | $0 | $0 ATM or out-of-network ATM fees (operator fees may apply) | |

| Axos First Checking | ATM access | 13 to 17 | $0 | $0 in network, up to $12 in domestic ATM rebates | |

| Fidelity Youth Account | Investing for teens | 13 to 17 | $0 | $0 ATM fees, worldwide ATM rebates |

Finder’s experts regularly review top kids’ bank accounts, debit cards and prepaid cards from various providers to find the best options in the market.

Finder’s banking experts research over 45 kids’ cards before narrowing down the best free accounts. We consider these five factors:

"You can start talking to kids about money as early as age five. At that age, they understand trade-offs like choosing between two toys, which is the perfect way to explain saving, spending and making choices. I’ve worked with parents who used clear jars labeled Spend, Save and Give to help young kids visualize where their money goes. It becomes second nature over time.

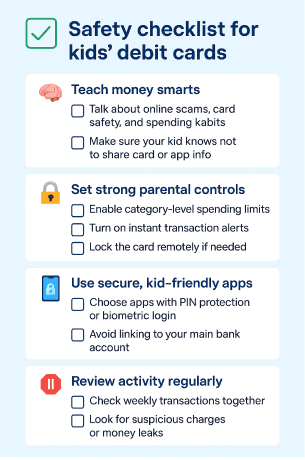

For a debit card, age 10 to 13 is usually a good window, depending on maturity. We’ve observed parents tie card access to allowance or chores, helping kids manage their spending while parents keep oversight. Look for cards with spending alerts, parental controls and the ability to lock the card remotely. It’s not just about the card — it’s about building trust and discipline in real time.

While parents and guardians compare

"Parents don’t need to have a flawless plan or scripted talking points — it’s more effective to let your child’s questions lead the way.

For instance, my four-year-old son once asked me if we pay for his activities. I used that as a starting point to explain that we pay for nearly everything in our lives — our home, his school, the water we drink and bathe in and even his activities. I added that the only thing we don’t pay for is the air we breathe. By connecting the concept of money to concrete examples from his everyday life, I was able to make an abstract idea easier for him to grasp. Starting these conversations early, guided by a child’s natural curiosity, can lay a strong foundation for financial understanding.

Minors can’t get debit cards on their own in most states. To open an account for your child, you’ll need to be on the account with them, usually as a joint owner or custodian.

Knowing that you’ll share ownership of the account can provide a lot of peace of mind. Additionally, all the best kids’ cards we chose have FDIC insurance coverage, meaning deposits are protected by federal deposit insurance up to the typical amount of $250,000.

Most other kids’ debit cards offer strong parental controls, such as the ability to lock the card with an app, set up a PIN for the debit card and block restricted merchants (such as alcohol and lottery purchases). Many also offer custom spending and ATM withdrawal limits.

It depends on the kids’ bank account you choose. With some kid checking accounts, teens are able to keep the account open until a certain age and then are required to upgrade to a standard account.

For example, with the Capital One TEEN Money account, teens have the option to upgrade to a regular Capital One 360 Checking account (also with no monthly fees). If they don’t want to upgrade to a regular 360 Checking account, the TEEN Money account can remain active.

Another example is the Fidelity Youth Account. Once the kid turns 18, that account must be converted to a standard Fidelity brokerage account.

There are plenty of free debit cards for kids that can help them learn essential financial skills, such as budgeting, saving and even investing, all without annoying monthly fees. Whether you’re looking for full parental control or a more flexible teen-friendly setup, one of these picks can help your child get started with money the smart way.

Compare more kids’ banking options.

Yes. Several options, like Modak, Capital One MONEY and Chase First Banking, charge no monthly or overdraft fees. Just watch for ATM fees or reload charges.

It depends. Some kid debit cards, like Chase First Banking, require the parent to have a Chase checking account. Others, like the Capital One TEEN Money account, let you link external accounts, and fintechs like Modak and Greenlight work as standalone apps that connect to your existing bank account.

Yes, many providers like Modak and the Chase kids’ account allow kids as young as six with a parent or guardian as a joint account holder.

Most providers let you convert the account to an adult checking account.

You have to be 18 to get a debit card in most states, but parents can open accounts for minors of nearly any age with select providers.

Teach your kids money management with these job ideas, including walking dogs, shovelings snow and teaching sports.

The base Till debit card for kids is free and includes several attractive features, but it has some limitations.

Kachinga is a kids’ prepaid card with chores and allowance features, but it comes at a cost.

A kids’ account with strong parental controls, but it requires an adult with a Revolut personal account.

Jassby lets kids earn rewards while they learn by reading financial articles, playing games and more.

Teach your child financial responsibility with this reloadable debit card that comes equipped with parental controls.

Compare the best kids’ debit cards with strong parental controls, minimal fees and fun features.

See our first-hand review of the Greenlight card to see if the $5.99 monthly fee makes sense for your family.

Compare the best four kids’ savings account options to save for their future, and learn essential things about investing and saving for kids.