Whether you use your van for work or recreation, you’ll want to find the right cover for you. Compare cheap van insurance and keep all four wheels rolling smoothing.

Over the last decade, the number of vans on British roads has increased by 37%. And while insurance premiums have risen over the last few years, there are a number of ways you can save whilst still getting the right policy for you.

What is van insurance?

Van insurance is a separate type of cover specifically designed to protect your van. Third party cover is the minimum legal requirement for van insurance in the UK, and you will need to take out a different type of cover if you use your van for commercial purposes as opposed to recreation.

How to compare van insurance

Consider how you use your van. Start by thinking about what you use your van for. Do you use it for work purposes (including driving to business locations) or as courier? Perhaps your van is solely for shopping trips and visiting family.

For social use, compare regular policies. If you only use your van socially, for example, shopping or visiting family and friends you’ll need private van insurance, which comes in three cover levels: third party, third party fire and theft and comprehensive.

For business use, compare commercial policies.commercial van insurance comes in three levels: carriage of own goods, carriage of goods for hire or reward and haulage. Depending on how you use your van for work, research the level of cover that best suits you.

Shop around. Whatever your policy needs, research as many policies and providers as possible to find the best deals. According to Finder research, comprehensive policies can at times be cheaper than third party cover, so check the full range of policies to see if you can get a cheaper deal with a more extensive policy.

Weigh up cost versus cover needs. The trick to finding the right policy is to balance the overall cost against your specific cover needs.

Do I need van insurance?

Yes. If you use your van strictly for recreation or as a substitute for a car, you are legally required to have at least third party cover in the UK. If you use your van for business purposes, you may need a form of commercial cover for your van — though commuting to a single place of work can often be covered under social, domestic, pleasure and commuting (SDP&C).

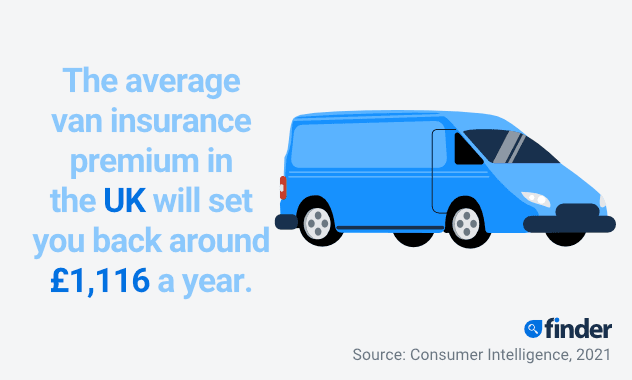

How much does van insurance cost?

Van insurance premiums have been rising in the last few years. Your premium will be affected by a number of personal and situational factors, but the average van insurance policy in the UK will set you back around £1,116 in 2021, according to insurance data specialist Consumer Intelligence.

How can I save on my van insurance?

Don’t auto-renew. Make sure you compare quotes from other providers before allowing yours to renew each year. If you find a cheaper quote you might find that your current provider will match it or even offer a cheaper deal.

Pay a higher excess. An excess refers to the amount you’ll contribute if you make a claim. As well as compulsory excess set by the insurance company there is voluntary excess. Increasing your voluntary excess signals to your insurer that your less likely to make a claim, helping to bring down your overall premium.

Try a black box. Fitting your car with a blackbox or using a telematics app can significantly reduce your premium as long as you drive well. Poor and dangerous driving however will cause it to go up.

Limit usage. If you’re able to do so, restricting certain high-risk drivers such as under 25s, seniors and learners from driving your van can lower your premium. Some insurers will also reduce your premiums if you cap the amount of time you’ll be using your van – in theory, less time of the road, means less risk.

Add a named driver. Listing a more experienced driver can help to reduce your premium, particularly if they’re listed as the main driver. It’s important that you don’t list them as the main driver if they are not.

Choose the right vehicle. The type of van you drive can significantly impact the cost of insurance. It’s worth spending time shopping around and comparing which vans you can get the cheapest premiums with.

Build up a no claims bonus. Your driving record and no claims history are used to determine how likely you are to be involved in an accident. If you haven’t made any claims in the last 4-5 years insurers may offer you a ‘no claims bonus’, granting you a discount on your premium.

Increase your van’s security Reducing the risk of your van being damaged or stolen is a great way to reduce your premium. Installing anti-theft devices or parking in a garage instead of on a main road is a great way to secure cheaper insurance.

Compare, compare, compare. It pays to do your research. Shop around and compare quotes from different providers. If you find a better offer don’t be afraid to switch. Make sure that when comparing that the policies are like for like. Cheaper premiums may just reflect less cover.

Take advantage of discounts Do your research and see if there are any deals on offer. Some providers might provide loyalty discounts or cheaper rates for new customers.

What types of van insurance are there?

Private. If you only use your van for social purposes like seeing friends and family or doing the weekly shop, you will need to take out private van insurance.

Carriage of own goods. This type of cover is for business vehicles in circumstances where you transport your own goods related to your trade, such as tools and equipment if you were a plumber, for example. You’ll also be covered for recreational and social use.

Carriage of goods for hire and reward. This type of cover includes the transport of goods for payment and would be suitable for delivery drivers.

Haulage. Haulage is similar to carriage of goods for hire and rewards, except that it does not cover you for the carriage of passengers for hire, say if you need to transport a team of workers to a site.

Given the new, recent tighter restrictions placed on areas all over the country, times still remain uncertain and so may well impact driving habits and, in turn, premiums. As always, though, premiums will be impacted by claim frequencies and severity.”

What are the different levels of van insurance cover?

There are three main types of cover for van insurance, as well as any driver insurance if your van is shared by multiple people. Each type offer different levels of coverage. It’s important you pick an options that suits your individual needs and aren’t just lured in by the cheapest one.

Third party

It is a legal requirement for all divers to at least be covered with Third Party insurance. This is the most basic form of protection and covers any damage or injury you cause to another party in an accident.

What is covered?

Injuries to others, including those in your van, other vehicles and pedestrians.

Damage to property or other vehicles.

The cost of legal claims against you.

What isn’t covered?

Accidental damage to your van.

Personal injury.

If your van is stolen.

If your van is damaged by fire.

Third party, fire & theft

This policy offers all the same as third party, plus any claims made against you as a result of an accident, protection of your van against fire and theft.

What is covered?

Injuries to others, including those in your van, other vehicles and pedestrians.

Damage to property or other vehicles

The cost of legal claims against you

Replacing your van if stolen

Damage to your van as a result of attempted theft or fire

What isn’t covered?

Other damage to your van

Cover for your personal injuries

A pay-out if your van is written off

Comprehensive cover

This is the most complete form of van insurance you can get. Comprehensive van insurance covers you for pretty much everything, except for that outlined in your policy exclusions. Some insurance companies offer a cheaper ‘stripped down’ comprehensive cover, which may exclude things such as windscreen cover.

What is covered?

Injuries to others, both in your van and other vehicles.

Damage to property or other vehicles.

The cost of legal claims against you.

Replacing your van if stolen.

Damage to your van as a result of attempted theft or fire.

Damage to your van.

Cover for your personal injuries.

What isn’t covered?

There may be some exceptions outlined in your policy exclusions.

Any driver

An alternative option is to get an ‘any driver policy’, often called fleet insurance. With this policy you don’t need to add any specific driver details as long as the driver has a clean driving history.

Most insurers will also require the driver to be over 25, however some providers will allow younger drivers. This is an ideal option if your van is is shared within a business.

The bottom line

You are legally required to have at least third party cover for your van in the UK. And, depending on what you use your van for, different types of cover will also apply. The average van insurance premium has increased by 197.9% since April 2014, but if you implement a few of our savings tips you could potentially save big on your cover. The key thing is to research as many policies and providers as possible to find the best cover at the best price for you.

Frequently asked questions

Drivers as young as 17 can take out van insurance, but their premiums are likely to be very high. Some providers will only insure drivers aged 21 and older so check with your provider before taking out a policy.

There are a number of optional extras you can add to your van insurance such as courtesy vehicle cover, breakdown cover, tool and equipment cover, goods in transit cover, any driver cover, legal protection and excess reimbursement cover.

This will depend on your policy and provider. Check with your provider for a specific list of countries where you’ll be insured. You could also take out European breakdown cover if you’ll regularly be driving in that region.

Some providers will include cover for business abroad in their commercial policies, check with your specific provider to make sure the level of cover is suited to your personal circumstances.

Much like car insurance, many providers will offer multi-van insurance which often works out cheaper than taking out individual policies for each van you intend to cover.

Yes. Either add courtesy cover as an optional extra to your van insurance or check with your provider to see if it’s already included.

No. Car insurance and van insurance are two different entities. Your van insurance only covers you to drive specific vehicles that you are listed as a named or main driver for.

Yes. If it is owned by the company, a van can be insured under your business’ name.

Yes. Generally, if you use your van for business purposes commercial insurance would come under a business expense.

If several people need to use one van, any driver van insurance will cover multiple people without them needing to be named drivers on your policy.

This will depend on your policy and what contents you need to insure. Typically, comprehensive policies will include contents insurance. But you may need additional cover to insure big ticket items like sporting goods or leisure equipment.

Contact your insurer to cancel your policy at any time or to specify a date in the future for when you want your policy to end. Some providers will have cancellation windows where you can cancel your policy with a full refund and no additional fee. Check with your provider for their specific terms otherwise you may be charged a fee and denied a refund.

It is possible to get temporary insurance. Whether you need to use a van for a few hours or a few weeks, taking out temporary insurance is much cheaper than paying for an annual policy. Unfortunately with temporary insurance you can’t build up a no claims bonus.

If you’ve got a van you’ve probably had family and friends ask to borrow it for a few hours or the day. If you’re happy to share with them or run a business which requires multiple drivers to be insured on your van then there are options out there.

Your first option is to name up to four drivers individually on to your insurance policy. It’s possible to get temporary insurance so drivers can be insured just for the period they need the van.

An alternative option is to get an ‘any driver policy’, often called fleet insurance. With this policy you don’t need to add any specific driver details as long as the driver has a clean driving history. Most insurers will also require the driver to be over 25, however some providers will allow younger drivers.

Private van insurance covers you to use your van for social purposes such as going to visit a friend.

Commercial or business van use allows you to use your van as part of your job, such as for making deliveries or transporting work tools. Even if you only commute to one place of work in your van you’ll need commercial insurance.

No, claims bonuses apply to a single vehicle, so can only be transferred to a new vehicle. It’s not possible to apply your no claims bonus to more than one vehicle.

In some rare cases providers may allow you to mirror your bonus to a second van or car.

Van insurance may be more expensive than regular car insurance for a number of reasons. As van drivers may also be more likely to use their vehicle in busy areas and drive more than regular drivers, they are also at more risk of accident, meaning their premiums will be higher. The cost of repairing a van is also likely to be more expensive than a normal car, which will also be factored into the cost of insurance.

If you are transporting your own belongings and are not receiving payment for doing so you will not need commercial insurance, and can instead drive on your normal private insurance.

The offers compared on this page are chosen from a range of products we can track; we don't cover every product on the market...yet. Unless we've indicated otherwise, products are shown in no particular order or ranking. The terms "best", "top", "cheap" (and variations), aren't product ratings, although we always explain what's great about a product when we highlight it; this is subject to our terms of use. When making a big financial decision, it's wise to consider getting independent financial advice, and always consider your own financial circumstances when comparing products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Louise is an editor and spokesperson at Finder, specialising in a broad range of financial topics from first-time buyers to financial wellness. Her personal finance expertise has been featured in Closer Magazine, The Sun, The Daily Mail, The Independent and more, and she has appeared on ITV News. You can check out her work across 500+ videos on Finder's YouTube channel, which has over 3 million views. In her free time, Louise can be found performing in comedy clubs across the UK or figuring out how to justify having a hot tub in her garden.

See full bio

Louise's expertise

Louise

has written

14

Finder guides across topics including:

Could a black box fitted to your van save you money on your insurance? Read our guide to learn more about telematics insurance and compare deals on your van cover now.

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.