Credit cards

Credit cards picked for you

You'll get your credit score and report in just 2 minutes, and it's absolutely free. You can come back and check it as often as you like and you'll even get automatic updates when your score changes.

Use your credit score and Finder's 'chance of approval' rating to understand your likelihood of getting accepted for a credit product like a loan or credit card.

This can help you protect your credit score by avoiding applications for products you might not be eligible for.

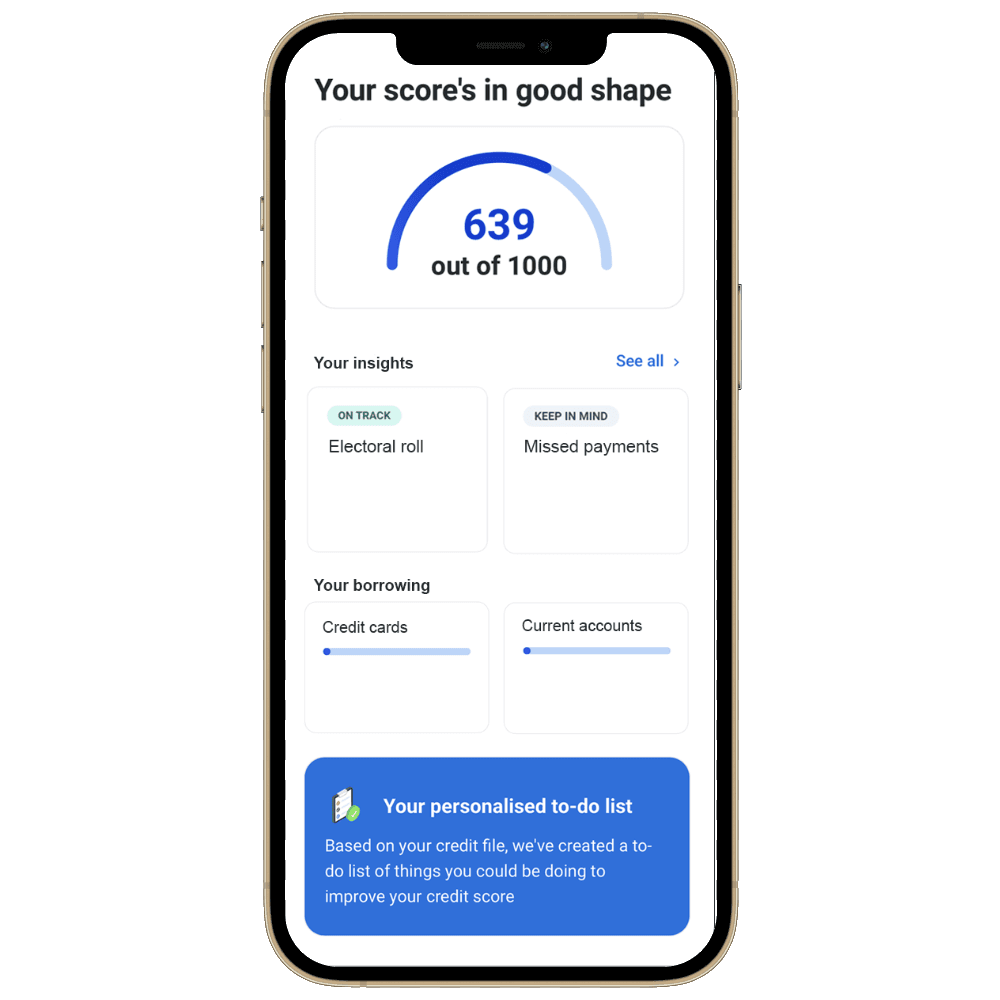

Get smart, personalised insights about your financial wellness plus expert guides on how to improve it.

Answer a few quick questions, and get completely free credit reports for life.

With Finder, you're in safe hands. We'll keep an eye on your credit file and notify you of any suspicious activity.

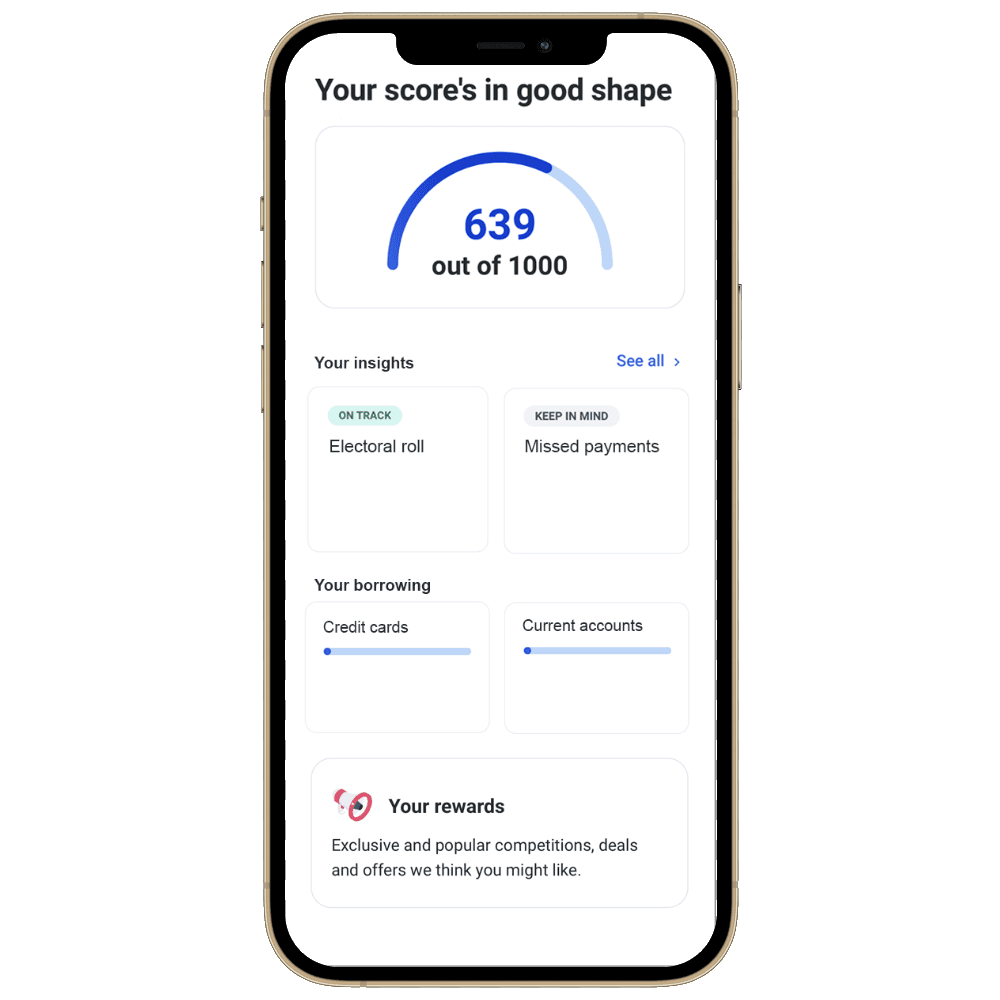

Your credit score is a number that represents how creditworthy you are - it demonstrates your reputation as a borrower and is calculated based on your financial activity and credit history.

Credit scores are produced by specialist credit reference agencies (CRA), and each agency uses its own scoring method to determine your credit score. Though, across all CRAs, the higher the score, the more creditworthy you appear.

The higher, the better when it comes to credit scores and, based on the scoring system you'll receive through Finder, above 670 is a very good score and above 810 is considered excellent.

Whenever you apply for credit, a potential lender will look at your history of borrowing and repaying to determine how much of a risk you are – in other words, how likely they are to get their money back. The better your credit history, the easier you will find it to obtain credit and the better the rates available to you.

Your credit history is stored by credit reference agencies. The biggest ones in the UK are Equifax, Experian and TransUnion.

Whenever you make an application for credit (e.g. a mortgage, credit card or personal loan), the lender will turn to these agencies to look at your score and history, which will play a major role in the success or failure of your application.

By looking at your credit report in conjunction with its own assessment of your circumstances, the lender will decide on whether to lend to you, how much to lend to you and how much interest to charge you.

Your credit report or history is a detailed record of your borrowing history, with information such as the loans you have held and applied for. It also includes personal information such as your name and address.

Your credit score is a number that is calculated using the information on your credit report. Your score determines your credit rating which could be "very poor", "poor", "fair", "good" or "excellent".

When deciding whether to take you on as a customer, lenders will usually look at your more recent financial history to determine their decision. However, your financial decisions, both good and bad, will remain on record for up to six years.

There is no single, definitive credit score for an individual. Each credit reference agency (CRA) uses a different scale. Lenders will normally check with one or more of these agencies when assessing your application for credit. These are the scoring ranges employed by the main UK CRAs (the higher the number, the better the score).

Depending on your score, you're said to have excellent, good, fair, poor or very poor credit:

| Agency | Score | Rating |

|---|---|---|

| Experian |

0 - 560 561 - 720 721 - 880 881 - 960 961 - 999 |

Very poor Poor Fair Good Excellent |

| Equifax |

0 - 438 439 - 530 531 - 670 671 - 810 811 - 1,000 |

Poor Fair Good Very good Excellent |

| TransUnion (formerly Callcredit) |

0 - 550 551 - 565 566 - 603 604 - 627 628 - 710 |

Very poor Poor Fair Good Excellent |

Our research found that 1 in 10 Brits (10%) would be classed as credit invisible in 2023, meaning they have no recent credit activity on record. This equates to around 5.6 million UK adults. If you are credit invisible or have a limited credit history, credit applications may take longer because lenders have to complete a manual and detailed risk assessment. The rates you are offered may also be higher.

All the content may be republished with a link to this page. Finder commissioned Censuswide on 27/11/2023 to carry out a nationally representative survey of adults aged 18+. A total of 2,000 people were questioned throughout Great Britain, with representative quotas for gender, age and region.

Press enquiries