nimbl review

Our verdict

nimbl has a unique feature to get your kids into the savings habit.

nimbl has all the key features you would expect from a kids’ card and app, such as regular pocket money, recurring tasks, savings goals and parental controls. But it sets itself apart with its micro-saving feature, which works like a round-up function. Kids can automatically save between 5p and £5 every time they spend on their card, helping to grow their savings pot over time.

The card does come with an annual fee, but there are no other charges for its services. It’s available from the age of 6 right through to teens. However, it’s worth pointing out that, unless your teen is really reliant on nimbl’s features, by then you can save yourself money by getting a regular children’s account from a traditional bank.

Get started by visiting nimbl's website and ordering a card. If you have read this review and decided that nimbl's card is not for you, you can also discover other prepaid cards for kids on the market.

Pros

-

Full control on how children spend their money thanks to spending control settings and instant notifications.

-

Children as young as six years old can use it.

-

It helps you to educate your children to manage their finances.

-

You can turn off online payments or cash withdrawals.

-

Safe and secure. The card can be blocked online or via the app.

-

You can manage more than one Child Account from the same Parent Account.

-

No fees for topping up the Parent Account or child’s card, or for “Gifting”.

Cons

-

While most mainstream bank accounts for children are for free, nimbl charges a monthly fee.

-

You cannot top up the account using cash.

-

With nimbl, children earn no interest on any savings.

nimbl’s fees and features

| Monthly fee | £2.67 |

|---|---|

| Card delivery fee | £0 |

| UK card transaction fee | £0 |

| UK cash withdrawal fee | £0 |

| Loading fee | £0 |

| Replacement card fee | £5 |

| Network | Mastercard |

| Account type | debit |

| How many child accounts | 4 |

| Other fees | £0 |

| Freeze/unfreeze card |

What are nimbl’s features?

- Card customisation

- Automated pocket money

- Instant top ups

- Parent and child app

- Savings goals

- Parental controls

- Spending alerts

- Tasks and rewards

- Gifting links

- Age-restricted sales

Card customisation

Children and teens can choose their card design.

Automated pocket money

Parents can set up and automate weekly or monthly pocket money.

Instant top ups

Parents can transfer money to their children’s cards instantly, whether they are out at the local shops or travelling somewhere overseas.

Parent and child app

nimbl comes with a parent app and a child app. This means your child has their own login and can manage their money safely, while you can track everything they do via your own app.

Savings goals

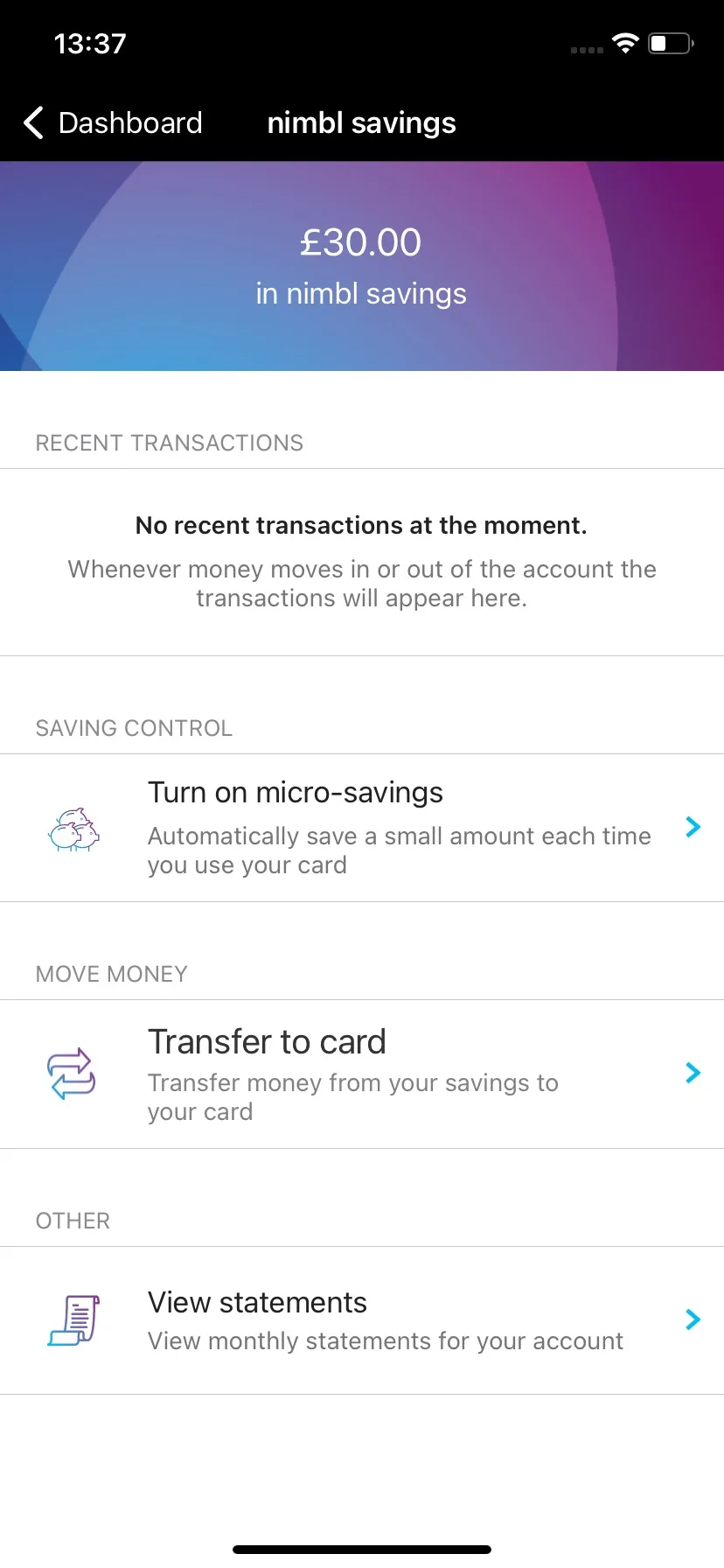

Children can save weekly or with one-off payments, or they can use micro-savings that round up every purchase and automatically save between 5p and £5.

Parental controls

Parents can decide where and when their children’s nimbl cards can be used, with limits available to set on cash machines, online and in-store spending.

Spending alerts

Receive real-time notifications every time your child uses their card.

Tasks and rewards

Parents can add tasks for children to do and pick a payment value. Once the task is completed, they can tick it off and the money will be transferred to the child.

Gifting links

With the “Gifting” function, family and friends can transfer money directly to a child’s nimbl card via a web link, if they’d like to send some pocket money or a birthday gift, for example.

Age-restricted sales

Your child can’t use their card to spend at certain places, such as pubs, gambling sites, casinos and off-licences.

How do I apply?

You can get started with nimble in 3 easy steps.

- Sign-up online. Fill in your and yours child’s details, pick a card design and choose your subscription plan.

- Activate their card. Download both the parent and child app, then when the card arrives activate it in-app or online.

- Top-up their card. Use your parent app to schedule their pocket money, top-up their card instantly and set up tasks where they can earn some extra money.

You’ll need to be the legal parent/guardian for the children you’re applying for and a UK resident. nimbl will also need to verify your identity and confirm your address during the sign up process.

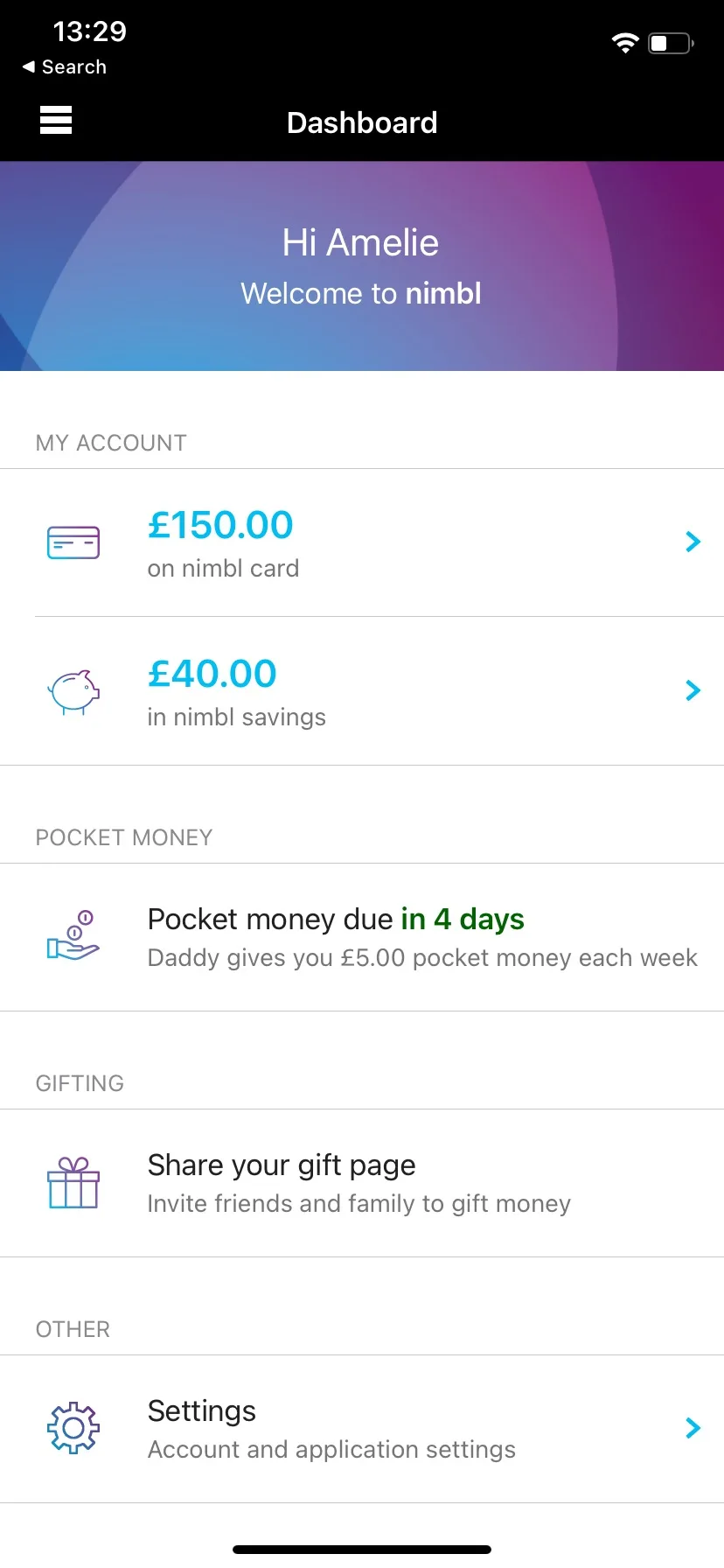

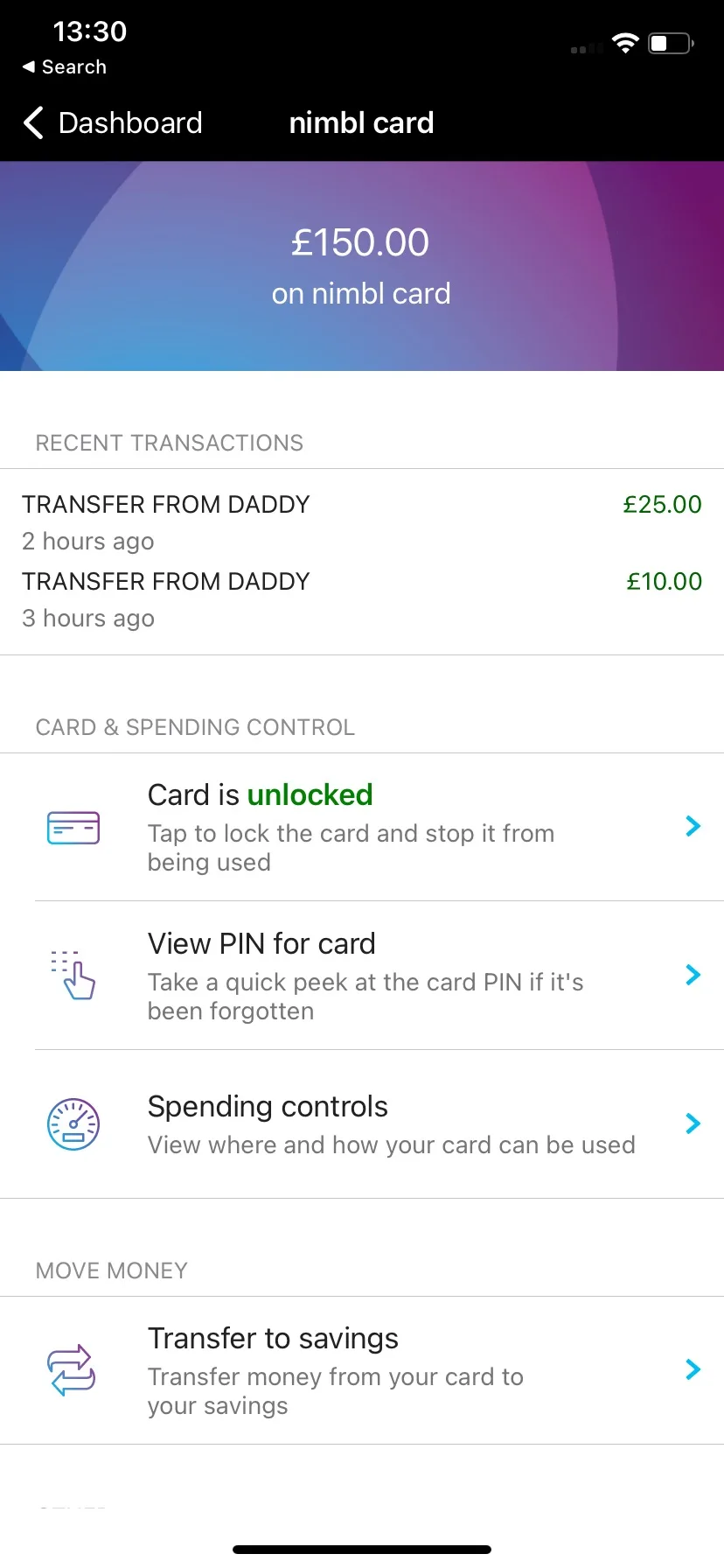

What does the nimbl app look like?

What do customers say about nimbl?

95% of customers we surveyed in 2026 would recommend nimbl to a friend.

It's praised for being a highly reliable, secure, and user-friendly way to teach children money management. Parents love the robust parental controls, the ease of topping up, and the independence it affords their kids.

While the vast majority find it incredibly useful and a great tool for setting savings goals, a small number of users expressed frustration over having to pay a fee when free alternatives exist, and a few mentioned inconsistent customer service.

AI-generated summary from the text of customer reviews on Finder.

nimbl and Finder Awards

Our Finder Awards celebrate brands that truly stand out in their field. nimbl was named our 2026 Kids' Cards Customer Satisfaction Award winner!

Customer service information for nimbl

| Email support | |

|---|---|

| Telephone support | |

| In-app or live chat | |

| Contact form | |

| Branch support |

Frequently asked questions

Sources