Lendio business loans

Submit one simple application to potentially get offers from a network of over 75 legit business lenders.

Apply now

on Lendio's secure site

| Features |

|

|---|

Lendio business loans Submit one simple application to potentially get offers from a network of over 75 legit business lenders.

Apply now

Features

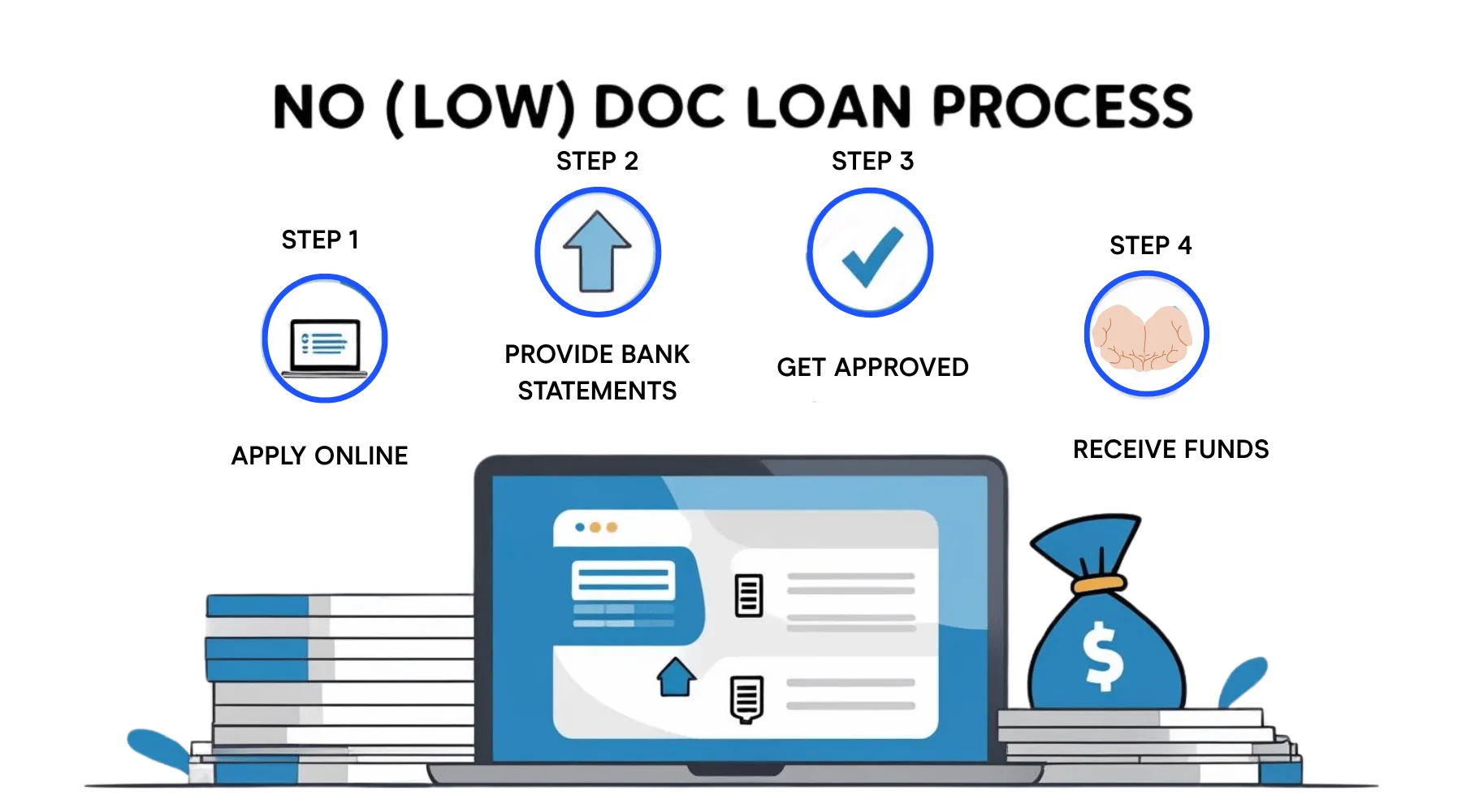

What is a no doc business loan?

A no doc business loan provides fast access to capital with minimal paperwork. Instead of tax returns or full financial statements, lenders evaluate your business using recent bank activity or revenue history. They’re designed for speed and simplicity, especially for borrowers who can’t produce standard paperwork or need to move quickly. These loans are faster to fund, but costlier and more restrictive in repayment terms.

No doc loans aren’t truly “documentation-free.” Lenders still need to assess risk. But instead of reviewing detailed financials, they may rely on bank statements, revenue history or collateral. The pitch is simple: faster funding with less scrutiny.

These products can be useful in a few situations:

Here are some examples of situations where a no doc loan may make sense:

"We were in a fast-growth phase and needed capital to expand into new markets. A no-doc loan seemed like the quickest way to secure funding without getting bogged down in paperwork.

The process was fast. We filled out a short application, shared bank statements and got approved within a few days. The downside was the interest rate, it was higher than traditional loans and the repayment terms were strict. But for short-term needs, it worked.

We had explored traditional bank loans and also spoke with a few VCs. Banks were slow and wanted a ton of documents. The VCs were more focused on long-term equity deals, which didn’t fit what we needed at the time. That’s when we pivoted to no-doc options.

Watch the repayment terms and interest rates closely. A lot of them require daily or weekly payments, which can hit your cash flow hard. Also, make sure the lender is reputable — some in this space are not transparent about fees."

Yes, LLCs can get approved for no doc business loans. Watch our short video to learn more about how they work and what you should know before applying.

No doc business loans offer more flexible eligibility criteria than traditional loans, but lenders still need enough data to assess repayment ability. Approval depends on alternative documentation and business performance, not tax returns or formal financial statements.

To improve your chances of qualifying, focus on the following:

Lenders prioritize speed and automation, so real-time access to your bank or sales platform data may be required as part of the application process.

No doc loans are not a low-cost financing option. Lenders price in the added risk through higher interest rates and shorter repayment terms. Some may require daily or weekly payments. Others secure the loan against business assets or future receivables.

No doc business loans are typically offered by online lenders and alternative financing platforms. These providers specialize in fast decisions and revenue-based underwriting. Traditional banks and credit unions rarely offer no doc options.

Examples of no doc or low documentation lenders include:

Most of these lenders use alternative data like bank transactions, sales platform integrations or POS history to make decisions without requiring full financial statements.

No doc business financing comes in a few different forms. Each uses different repayment structures and underwriting criteria, but all share a streamlined documentation process.

| Loan Type | APR Range | Typical Use Case |

|---|---|---|

| Traditional Bank Loan | 6.13% – 12.36% | Established businesses with strong credit |

| SBA 7(a) Loan | 10.5% – 15.5% | Government-backed loans for various purposes |

| Online Term Loan | 14% – 99% | Faster funding, less stringent requirements |

| Merchant Cash Advance | 40% – 350% (factor rate) | Quick access based on future sales |

Since no doc loans cover several types of financing options, you can generally expect to pay a higher rate compared to traditional business loans.

| Years remaining | Principal remaining |

|---|

Lenders use alternative underwriting methods when documents are limited. These may include:

No doc loans can become costly quickly, especially if repayment is daily or based on fluctuating sales. Evaluate the total cost of capital, not just interest rates. Some lenders use factor rates, which mask true APRs. Others may include fees for early repayment, origination or account maintenance.

Check the fine print on:

Business owners shared their unfiltered experiences with no doc loans with us. Here’s what they had to say in their own words:

Weigh your business loan options by amount and requirements to see which fits your needs best. Tap Go to site to get started on your application. Or, visit our review page by choosing More info.

We currently don't have that product, but here are others to consider:

How we picked theseThe Finder Score crunches 12+ types of business loans across 35+ lenders. It takes into account the product's interest rate, fees and features, as well as the type of loan eg investor, variable, fixed rate - this gives you a simple score out of 10.

To provide a Score, we compare like-for-like loans. So if you're comparing the best business loans for startups loans, you can see how each business loan stacks up against other business loans with the same borrower type, rate type and repayment type.

All responses are collected anonymously and used for internal data purposes only.

What is your primary need for a business loan?

If you can afford to wait, a traditional business loan or SBA microloan may be more affordable long-term. Other flexible options include:

No doc business loans offer a fast, flexible option for entrepreneurs with documentation gaps or urgent cash needs. But that convenience comes at a premium. If you can produce even basic financials, better terms may be available elsewhere. For time-sensitive situations or newer businesses, no doc loans can be a practical bridge, so long as repayment obligations are clearly understood.

No. While they don’t require full financial statements or tax returns, lenders still need to assess risk. Most will ask for bank statements, proof of revenue, or basic business details.

Funding can happen in as little as 24 to 72 hours, depending on the lender and the information you provide. Speed depends on how quickly you can verify your revenue or bank activity.

Yes, many lenders report loan activity to credit bureaus. Some may do a soft pull during prequalification, but a hard credit inquiry usually occurs before final approval.

Yes, especially if they have strong bank activity or collateral. Some lenders specifically market to new businesses or sole proprietors with limited documentation.

Yes, but it’s rare. Most lenders require more than just an EIN (Employer Identification Number) to approve a no doc business loan. While an EIN is necessary to identify your business, lenders typically also want to see recent bank statements, proof of revenue, or access to your sales platform. Some fintech lenders may approve small loan amounts based primarily on business activity tied to your EIN, but expect to provide additional data like:

No doc loans that accept EIN-only applications are typically secured with daily repayments, higher interest costs and may require a personal guarantee even if your Social Security number isn’t used up front.

Compare the best commercial real estate loans for buying, refinancing or renovating business property.

Compare the best franchise financing options, from SBA lenders to marketplaces and retirement-fund financing.

Taycor Financial offers equipment, term and working capital loans but keeps pricing off its website.

Compare top lenders offering working capital, equipment financing and microloans for plumbing businesses in 2026.

Compare food truck financing options, from 0% microloans to fast term loans, and find the right fit for your mobile kitchen.

Bank of America offers secured and unsecured business loans and lines of credit for established small businesses.

Compare the best HVAC business loans for equipment, SBA funding, working capital and seasonal cash flow gaps.

The best retail business loans for inventory, renovations and cash flow — compared.

Delta Capital Group offers same-day unsecured business funding from $5,000, but rates aren’t disclosed up front.

Compare the best business cash flow loans in 2023.