Blockchain is being heralded as a revolutionary new technology. But beyond its use in cryptocurrency, very few people understand what they can use it for or what industries it could change. This guide aims to demystify blockchain technology and explain what it is, what it’s used for, how it works and where its future might be.

Disclaimer: This page is not financial advice or an endorsement of digital assets, providers or services. Digital assets are volatile and risky, and past performance is no guarantee of future results. Potential regulations or policies can affect their availability and services provided. Talk with a financial professional before making a decision. Finder or the author may own cryptocurrency discussed on this page.

What is blockchain?

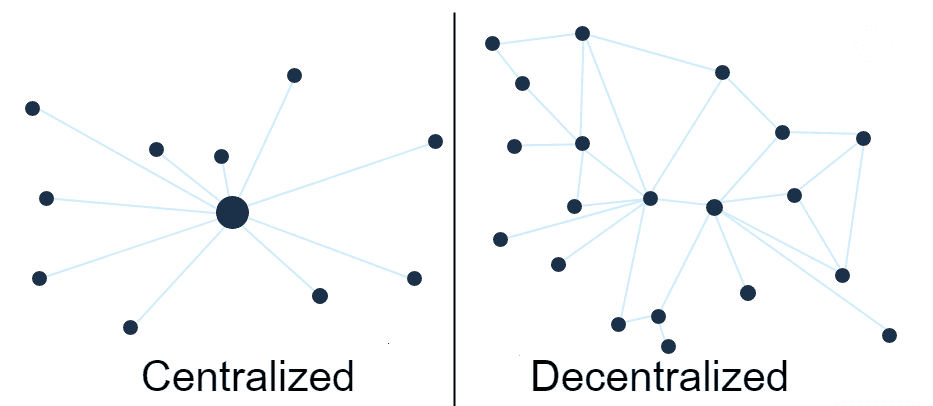

In essence, a blockchain is a database where you can add information, but not remove it. The data stored on a blockchain can be anything, including money (such as bitcoin), insurance claims or even shares of physical property such as real estate. Instead of being stored on a single server, the database is spread out and stored on a vast network of computers known as nodes. This means that the system is distributed and that there is no central point of failure.

These nodes work together to add new information to the blockchain. This information is added in bundles known as blocks, and each time a new block of information is added, it is chained to the previous one in a linear fashion resulting in the blockchain.

Compare this to a traditional server setup where a central server stores a copy of the information that you then access through external servers. Whoever controls the central server is in charge of adding information as well as changing or removing it. If the central server is damaged or hacked, the data is compromised. This is one of the problems that blockchain can solve.

Because of the decentralized nature of a blockchain, it means that there is no one single entity with the power to change the state of the blockchain ledger and do things like shut down accounts or seize funds, unlike banks.

Another problem that blockchains solve is the issue of trust.

When parties make a transaction via the blockchain, they only need to place trust in the underlying infrastructure of the blockchain rather than in each other. Since a decentralized computer network can record and verify each transaction as well as make the transaction transparent, trust is created by default.

This means that a blockchain allows for “trustless” transactions. The transacting parties do not need to worry about trust because they give total trust to the network. In other words, using a blockchain means putting your trust in computers, rather than people who could have bad intentions or might simply make a mistake.

How does blockchain work?

A blockchain works by keeping an unchangeable (immutable) record of transactions. It does this by reaching a consensus between all the computers, or nodes, on the network. Because blockchains consist of a distributed network of computers with no central authority, the majority of the nodes must agree to any addition to the blockchain (adding the next block). No one party can make any changes, which is what makes a blockchain a decentralized system. The more nodes that join the network, the more decentralized it becomes, which in turn improves security.

Consensus refers to the agreement between the nodes on the blockchain’s true state of affairs. If one node tries to lie, then its record of the blockchain won’t match that of the other nodes, and it will be automatically ignored. This system of consensus is fundamental to the security of the blockchain.

You control your personal data on a blockchain by using private keys. A private key is like a lengthy password that gives you access to a digital wallet where your personal data is stored. This data could be anything from money to details about your last medical checkup. The benefit of a private key is that it doesn’t have to be stored on a central server, unlike passwords for regular websites like Google or Facebook, which are prone to hacks.

What problems does blockchain solve?

On a trustless network like a blockchain, you can ask for payment from someone you’ve never met, and when the payment arrives, you can be sure that it is legitimate and verified, all within a matter of minutes. Existing systems such as the SWIFT banking network currently take two to three days to do this.

Another issue blockchains solve is the double-spend problem. The double-spend problem centers around the idea that on a database, someone can make an entry and then go back and change it if they have the power or authority to do so. This would essentially allow someone to spend the same money twice.

Blockchains solve this through a combination of factors that all prevent double spending:

Each transaction is time-stamped and kept in the correct order.

Every node must have a copy of the same ledger to reach consensus and to continue the blockchain.

Any node with a copy of the ledger that doesn’t match the majority of the other nodes will be ignored. That is, if someone tries to spend the same money twice by sending it to two different nodes, then only the node that matches the rest of the nodes on the network will be accepted in the next block of data.

What else can a blockchain do?

Blockchains belong to a group of technologies known as distributed ledger technologies (DLT). DLTs as we know them today have only been around for a decade or so, but are already receiving a lot of attention and development. Much like the Internet, additional protocols and technologies are being built on top of blockchains to further their abilities.

Let’s take a look at some of the most popular ones used today.

No article discussing blockchain technology would be complete without mention of cryptocurrency. Cryptocurrencies are digital “coins” that are native to their blockchain and can be used to reward node operators that help to secure the network and verify transactions.

Because blockchains require computing power to operate, cryptocurrencies were created as a way of rewarding network participants for their efforts. Cryptocurrencies also double as a store of value. The world’s first cryptocurrency, bitcoin, was created in 2008 and has since spawned a revolution in digital assets and finance, with over 1,000 cryptocurrencies now existing today.

Much like their big brethren cryptocurrencies, tokens are also digital assets that are stored and traded on a blockchain. However, unlike cryptocurrencies, tokens are programmed “on top” of an existing blockchain, allowing them to piggyback the existing network infrastructure in the process. This means that tokens can be created easily, can be programmed for an even bigger variety of uses than their underlying cryptocurrencies, and can be used to represent almost anything, including gold, fiat currency and even electricity usage.

Pioneered by the Ethereum blockchain, smart contracts are digital contracts that you can program to perform a specific set of functions. Like a physical contract, fulfillment of the contract requires that participants meet certain conditions, but unlike a physical contract, smart contracts can then execute the terms automatically once these conditions are met, such as paying out an insurance claim once you have paid the premium. Furthermore, smart contracts can do this without the need for middlemen, reducing cost while increasing speed and accuracy. According to financial services company PwC, smart contracts may even eliminate the need for lawyers.

If smart contracts were the second revolution of blockchain technology after cryptocurrencies, the digitization of real-world assets on the blockchain could be the third. The ability to digitally render ownership of a real-world asset on a blockchain has huge implications for transparency, efficiency, ease-of-use and fundraising for traditional securities markets. Moving securities onto the blockchain via the use of security tokens has the potential to shake up legacy markets like the NASDAQ, NYSE and ASX in the same way cryptocurrencies shook up banking and finance.

Blockchain has a wide variety of uses within the emerging Internet of Things. For the uninitiated, the Internet of Things refers to the network of Internet-enabled devices, such as smartphones, TVs, cars, consumer appliances, etc. Blockchain is able to assist the way these devices communicate with each other, transact, stay secure and automate processes. For example, distributed ledger platform IOTA is working with several car manufacturers, such as Volkswagen, to integrate microtransactions, which will allow electric vehicles to autonomously charge their batteries as well as pay for parking and tolls.

A report by financial services firm PwC notes that in regards to blockchain and IoT, “There is huge potential here: in 2015, there were already over 5 billion connected devices; this should rise to 20 billion by 2020.” Contrast this with another report by corporate analysis firm IDC which predicts that “By 2019 … 20% of all IoT deployments will have basic levels of blockchain services enabled” and you can see why blockchain, distributed ledger technologies and IoT are going to be a big deal.

Digital identities are nothing new, but blockchain promises to bring existing disparate systems together to create a product that is greater than the sum of its parts. Thanks to the efficiency and privacy of blockchains, governments and organizations could safely record an individual’s details on a blockchain while giving ultimate control of that data to the end user.

Another advantage is that unlike physical documents, a distributed ledger is immutable and cannot be lost or easily destroyed. While each implementation of digital identities will no doubt vary, several existing uses of blockchain for digital identity demonstrate how it can be used. Australia has already begun trials of a digital driver’s license stored on smartphones and secured by a blockchain. As the refugee crisis continues, the World Food Program is using blockchain to manage food vouchers and ensure aid is reaching those who truly need it. And industry heavyweight Microsoft began testing a decentralized blockchain ID system in 2018 for a broad range of applications.

Global supply chains are another industry that blockchain looks set to disrupt in a big way. Giants of industry such as Maersk, Amazon, Walmart and DHL are all exploring ways to improve their existing systems with blockchain technology. Blockchains have the ability to add a level of authenticity and trust to supply chains that is sorely missed by legacy systems. Startups such as VeChain, WaltonChain and veteran companies like IBM are all applying blockchain in innovative ways to improve the supply chain industry.

Public vs. private blockchains

Despite the world’s first distributed blockchain being a public affair, several companies have entered the space and found ways to commodify the technology, leading to the creation of permissioned private blockchains.

Private blockchains differ to public blockchains in that the nodes which operate and secure the network are privately chosen. This means that the network is effectively centralized due to the ownership of nodes by a single entity or a consortium of private parties.

Blockchain purists argue that this goes against the fundamental purpose of a blockchain, which is to be decentralized. Because decentralization is a cornerstone of blockchain security and integrity, the argument is that by centralizing all the nodes there is almost no point in running a blockchain.

Private blockchains, of course, have a place — otherwise, people wouldn’t use them. Despite the concerns around centralization, they are often faster and can process more transactions per second than public blockchains. Furthermore, the organizations using them may have less need for the benefits that a decentralized network confers.

For example, the privately operated Red Belly Blockchain can reach speeds of 30,000 transactions per second, whereas the highly popular public blockchain, Ethereum, currently transacts at a speed of roughly 15 transactions per second, although improvements are planned.

Public blockchains are also, by their very nature, public. This means that anyone can see the transactions, anyone can join the network and anyone can see the code. Allowing the public to view everything helps ensure compliance, transparency and security but can also lead to exploitation. Furthermore, anyone can host a program on the network, which may cause the network to slow down if it becomes too popular.

So as you can see, public and private blockchains each come with their own set of strengths and weaknesses, which again differs depending on the particular blockchain at hand. Therefore companies, developers and users must choose which system they would prefer to run, depending on the task at hand.

Who uses blockchains?

Anyone can create a blockchain, although certain blockchains are more popular than others. Bitcoin was the first public blockchain created, and it was designed for the transfer of wealth without a trusted third party. Since then, many different developers, companies and hobbyists have created their own blockchains for all sorts of purposes.

Let’s take a look at some of the biggest companies using or exploring blockchain technology this year.

IBM. IBM has quickly taken the lead in developing blockchain solutions for private enterprises and the news about partners keeps growing. So far clients include banks, logistics firms, international money transfer groups and insurance providers.

The World Bank. The World Bank recently employed the Commonwealth Bank of Australia (CommBank) to issue bonds on its behalf using CommBank’s blockchain. CommBank issued the bonds digitally using a blockchain, making the process much faster than legacy systems which still use phones and sales staff.

American Express. Payments provider American Express is tapping into blockchain to improve their customer rewards experience. The company uses the Hyperledger platform to enable merchants to create their own customized Membership Rewards programs for American Express users.

Ford Motor Co. Car manufacturer Ford has patented a blockchain system that uses a cryptocurrency to allow vehicles to communicate and transact with each other. Ford imagines the technology could be used to allow driverless vehicles to coordinate traffic and even let cars purchase “fast lanes.”

Bank of America. Bank of America thinks blockchain is going to be the next big industry, predicting that the technology will become a billion-dollar market. They’ve invested on that prediction too, filing nearly 50 patents already, according to CTO Catherine Bessant.

Microsoft: Microsoft offers blockchain services such as Corda, Hyperledger and Ethereum through their cloud computing system Azure. While Microsoft offers blockchain services to a long list of third-party clients, they have also put their money where their mouth is. Microsoft’s video game platform — Xbox — uses blockchain to settle publisher royalties almost instantly, replacing their previous system, which typically took 45 days to settle.

Issues with blockchain

Identifying issues with blockchain technology really depends on where you sit and the particular blockchain. Critiques often revolve around speed, issues of centralization (or decentralization), adoption, complexity and privacy. Some of these issues have fairly simple solutions, such as choosing a private blockchain to increase privacy or creating a new interface to improve usability.

However, the one major issue that several of these smaller issues contribute to is the issue of scalability.

Scalability refers to the ability (or lack thereof) for blockchains to scale as more users join the network. As more users join, speed and size (bandwidth) needs to increase in order to process all the new data being added. Currently, blockchains struggle to do this without making a trade-off in other areas, namely decentralization and security.

This three-way trade-off among scalability, decentralization and security has become known as the Blockchain Trilemma.

Must read: The Blockchain Trilemma

The Blockchain Trilemma refers to the existing problem in blockchains where any improvement to scaling, decentralization or security cannot be made without a detrimental impact on at least one of the other two. Many blockchains have tried to solve the trilemma, only to improve in one area but lose out in another.

This is currently one of the biggest issues with blockchain technology, and cited by many as the reason why blockchains have not replaced existing systems like Visa and SWIFT for payments.

FAQs

Decentralization and distributed are actually two different features, but both are important to blockchain security.

Decentralization refers to there being no central authority that can make changes to the blockchain.

Decentralization is never a guarantee, but rather something that public blockchains work to ensure. Private blockchains on the other hand may actually choose to be centralized because it suits their needs.

Distributed systems refer to the fact that instead of data being stored on a central server, the data is stored across multiple servers, or nodes. All blockchains are distributed, which means there is no central point of failure if the network were ever attacked or physically damaged.

Since blockchain is a type of technology, you can’t invest in “it” per se. However, you can invest in companies or organizations that use it. Cryptocurrencies are a popular form of blockchain investment since they allow people to purchase the currency or token that powers a particular blockchain or uses the blockchain.

Another way to invest in blockchain is by choosing companies that are developing blockchain technologies and purchasing stock in those companies.

Disclaimer: Cryptocurrencies are speculative, complex and involve significant risks – they are highly

volatile and sensitive to secondary activity. Performance is unpredictable and past performance is no guarantee of

future performance. Consider your own circumstances, and obtain your own advice, before relying on this information.

You should also verify the nature of any product or service (including its legal status and relevant regulatory

requirements) and consult the relevant Regulators' websites before making any decision. Finder, or the author, may

have holdings in the cryptocurrencies discussed.

Whether products shown are available to you is subject to individual provider sole approval and discretion in accordance with the eligibility criteria and T&Cs on the provider website.

James Edwards was the global cryptocurrency editor at Finder. He coordinates a distributed team of journalists to help further Finder's mission of helping people make better financial decisions.

He has been using Bitcoin since 2013 and began working in the industry in 2017. He takes pride in boiling down complex topics into language his parents can understand.

His expertise has seen him called on to report at events such as TechCrunch Disrupt, CoinDesk Consensus and IBM Think and has coordinated a vast number of high-profile interviews with the industry's brightest minds.

He is a regular contributor to Nasdaq, The Street and is frequently called upon for market commentary in Australia and abroad.

See full bio

I have two blockchain accounts. The first one was creditied with 1000 USD, the second account was creditied with totally 3000 USD. With the exception of approx. 50,00 UISD Balances of both accounts disappeared. Apparently the amounts were sent to another wallet which is not under my control. A screenshot of my transactions can be made available. Brgds

Finder

fayemanuelJuly 20, 2019Finder

Hi Peter,

Thanks for contacting Finder.

Please note that we are a comparison website and we can not vouch for a company as we do not represent any of the providers on our page. Please contact your digital currency exchange provider to look into this. If you believe that it was a scam, you may report it to the proper authority.

Every 3 months, Finder empanels a range of industry specialists to get a pulse on what the future holds for crypto. This is a summary of those findings.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

I have two blockchain accounts. The first one was creditied with 1000 USD, the second account was creditied with totally 3000 USD. With the exception of approx. 50,00 UISD Balances of both accounts disappeared. Apparently the amounts were sent to another wallet which is not under my control. A screenshot of my transactions can be made available. Brgds

Hi Peter,

Thanks for contacting Finder.

Please note that we are a comparison website and we can not vouch for a company as we do not represent any of the providers on our page. Please contact your digital currency exchange provider to look into this. If you believe that it was a scam, you may report it to the proper authority.

Kind Regards,

Faye