Warning: Late repayment can cause you serious money problems. For help, go to moneyhelper.org.uk.

Please note: High-cost short-term credit is unsuitable for sustained borrowing over long periods and would be expensive as a means of longer-term borrowing.

Payday loans are designed for borrowing money in the short term. They typically come with high interest rates and should be used with caution. Read our guide to find out more about how payday loans work and what you should know if you are considering applying for one.

Calculate the cost of your loan

Table: promoted deals, sorted by total payable

How much do you need to borrow?

How long do you need to borrow for?

Important information: You should always refer to your loan agreement for exact repayment amounts, as they may vary from our results.

What are payday/short term loans?

Payday loans are high-interest loans over relatively short periods of up to a month. As the name suggests, they are designed to tide you over until you receive your pay cheque.

Payday loans, along with other short term, unsecured personal loans where the APR (annual percentage rate) is 100% or higher are defined as “high-cost short-term credit” by the Financial Conduct Authority (FCA). You generally won’t see high street banks providing these – a number of predominantly online companies like the now-defunct Wonga and QuickQuid found success in the early 2000s offering payday loans over the internet.

Are they a good idea?

Payday loans are a very expensive method of borrowing and should only be considered as a last resort. They may not solve your money problems, and they’re not a good idea for borrowing over longer periods or for sustained borrowing.

Before you apply for one, make sure you’ve considered other options, such as a credit card or a personal loan. Is the expenditure absolutely essential? If you can defer a purchase, then you could save yourself money in the long run. If you’re struggling to pay a bill, talk to your electricity, gas, phone or water provider to see if you can work out a payment plan. Read more about alternatives to payday loans at MoneyHelper.

How are payday loans different from other types of credit?

Shorter loan terms. Payday loans are designed to be short term solutions to financial shortfalls. Although lenders are starting to move towards longer loans, the norm is around 1 to 6 months. A few lenders still offer loans as short as 1 week.

Smaller loan amounts. How much you can borrow depends on the particular lender, but payday loans typically range from £50 to £1,000. For new customers, the maximum is likely to be at the lower end of the scale.

Less strict eligibility criteria. While payday lenders will always conduct a credit search before approving you, they’re often less interested in your credit rating and more interested in whether you can afford to repay the loan.

Higher rates. Payday loans come with much higher APRs than almost all other forms of credit. In the UK, the interest and fees are capped at 0.8% per day, but it’s always important to take into account the full cost of the loan before you apply.

How do payday loans work?

Like most lenders, payday or short term loan providers charge interest on the money they lend to you. Interest is a fee for borrowing and is normally a percentage of the amount you borrow – so if you borrow more money, you pay more interest. If you decide to take out a payday loan, you can expect to pay up to 0.8% interest each day – that’s £4 for every £500 borrowed, every day.

For loans of 1 month or less, you’ll generally repay the money borrowed (plus interest) in 1 payment, but for loans of more than 1 month, you’ll generally pay 1 “instalment” each month. In the majority of cases, with each instalment you pay off part of the capital (the amount you have borrowed) as well as the interest you have accrued so far. This means that your first instalment would mostly go towards paying interest, while your last instalment would mostly go towards clearing the capital.

Some lenders, however, provide short term loans on an “interest-only” basis. That means that each month, you pay only the interest that your capital has accrued, and then in the last instalment, you’ll pay the interest and clear the capital. This might seem like a good idea, because all but the final instalment will be smaller than if you were steadily chipping away at the capital. However, you’ll pay more interest overall with an interest-only loan (compared to an interest and capital repayment loan at the same rate).

Although the majority of lenders do not charge a fee to apply for these loans, heavy fees can be incurred if you don’t make payments on time. Late payments are also likely to damage your credit rating and, therefore, your ability to borrow money in the future. Only consider a payday or short term loan if you’re certain you can meet the repayment schedule.

How to compare payday loans or short term loans?

When you’re in urgent need of money, even a bad deal can look good. Be sure to compare lenders to get a loan with the best rates that fits your needs. Here are some things to consider:

Loan amounts and durations. Does the lender you’re considering offer the loan amount and term you require? Don’t forget that new customers are unlikely to get approved for a lender’s maximum available loan. Choosing a longer loan term reduces monthly repayments but also means you pay more in interest overall.

Eligibility. If you don’t meet the required eligibility criteria, there’s no point in applying and doing so might damage your credit rating. Checking the eligibility criteria ahead of time minimises the chance of a rejected application. To be eligible for a short term loan, you will usually need to be a UK resident, be at least 18 years old, have a UK bank account and have a steady income.

Interest rates. Interest rates for payday loans can be eye-wateringly high, so compare them carefully.

Fees. Generally, payday lenders don’t charge any upfront fees such as “product” or “application” fees (although it’s still smart to make sure), but many charge up to £15 for late repayment. There are plenty of other good reasons not to miss a payment, however – not least the damage to your credit score.

Total payable. Perhaps the single most important factor to consider is the total amount the loan will cost you (provided you don’t miss any repayments). The amount consists of the original amount borrowed plus the interest. Because different lenders structure their loans in different ways, the total payable helps consumers to easily work out which lender is cheapest.

Money processing. Check how quickly you will receive your funds. Online lenders can often transfer the money on the same day, but in some cases, it could take 1 to 2 business days for the funds to reach your account.

When considering any loan, it’s a good idea to work out the total amount you’ll need to repay. Lenders should be upfront about this figure, and in many cases, it’s a more useful figure than the interest rate. A lower rate might not benefit you if the loan term is longer than you need. If there are no penalties for repaying the loan early and you think you can, then a better rate could outweigh a shorter term.

Why should I read a short term loan review?

There are still dozens of short term lenders across the country. However, while many are trustworthy and follow all the rules and regulations, others are predatory and use payday loans as a way to take advantage of borrowers.

By reading reviews and comparing lenders, you’ll help make sure you find the short term loan that’s best for you and save yourself a lot of time and money.

A good review covers the benefits and drawbacks of the lender without too much bias. If the review is too positive or negative, watch out. It could be someone paid to leave a good review or someone with bad budgeting skills leaving a bad one. The more moderate a review is, the more trustworthy it may be.

If you think there might be a chance the lending company you’re looking at is a scam, then avoid them at all costs.

What can you find out from a short term loan review?

A good short term loan review gives you all the information you need to make an informed decision and should cover these aspects:

Interest rate and APR. While you have to pay interest on a short term loan, the APR represents the true cost. It includes the interest as well as all associated fees. The amount varies considerably from 1 lender to the next.

Fees. Short term loan reviews should give you a clear indication of all the fees and charges you could end up paying throughout your loan, including early repayment and late payment fees.

Repayment options. There are a number of ways you can repay a loan, but some lenders don’t allow all of them. Read reviews to find out what the company you’re looking at prefers.

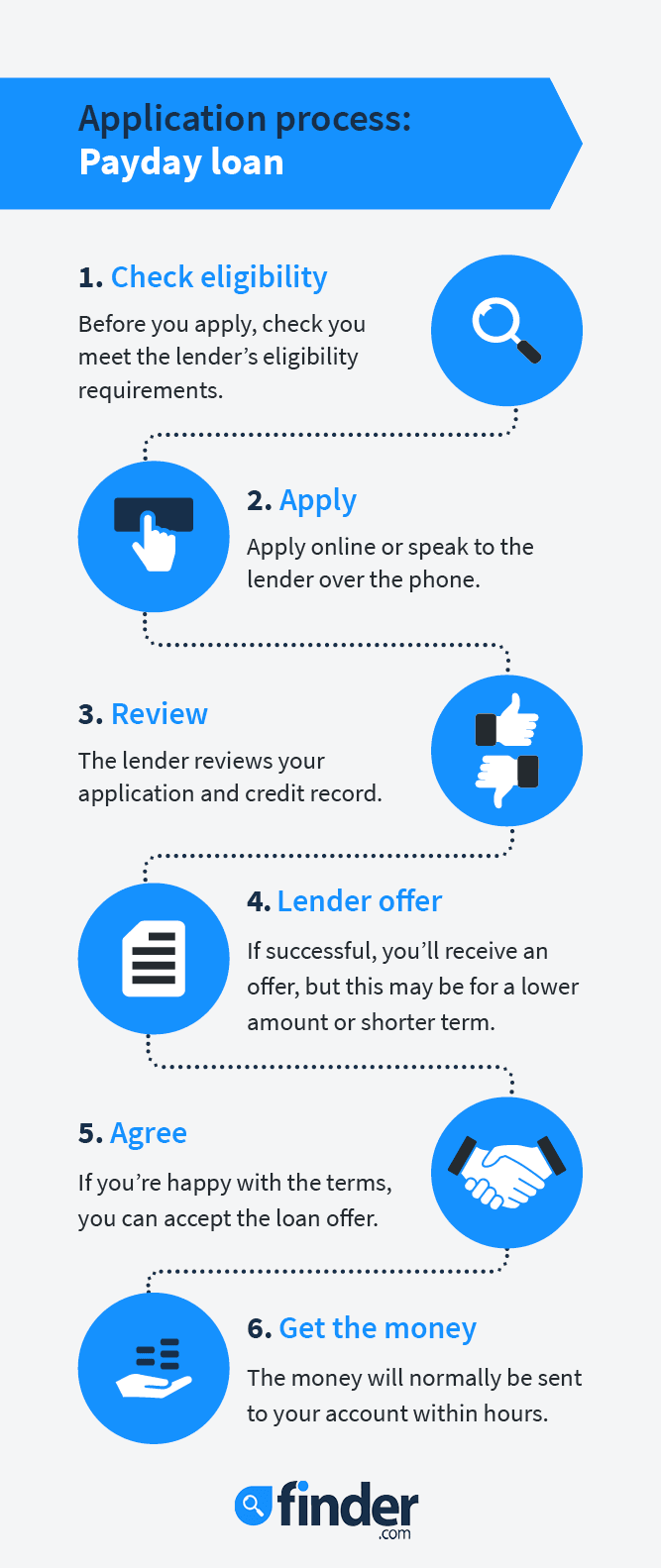

Application process. A good review should tell you how simple or complicated the application process is and how long it might take to complete.

About the lender. Reading a short term lender’s review should give you some idea about the company’s history and the other products the lender offers.

How to tell if a short term lender is legitimate

The following should help you find legit short term loans easily:

It has FCA authorisation. If the lender you are borrowing from is legitimate, it should be in the FCA register.

It gives various active contact details. Take some time to find a lender’s contact details – typically in the footer of its site. If a lender provides no more than a contact form or an email address, see how responsive it is before you apply. A legitimate short term lender shouldn’t shy away from providing a physical address, phone support or live chat.

It’s upfront about costs. Direct lenders of legit short term loans should be upfront about the fees and charges you have to pay during the loan term, and to adhere to all given maximum limits (if a lender’s quoting a rate higher than 0.8% per day, steer clear). The loan contract should clearly set out all applicable fees and charges.

It doesn’t require money upfront. One of the biggest red flags when researching a lender is if it requests money upfront. You shouldn’t have to pay anything before you borrow.

How are payday loans repaid?

The majority of lenders will insist on debiting your account on the day you get paid, using a “Continuous Payment Authority” (CPA). However, some lenders accept payments by other means, such as direct debit or a manual transfer.

What is a Continuous Payment Authority (CPA)?

A CPA is a payment arrangement in which you give a company permission to withdraw money from your account on a recurring basis. CPAs differ from direct debits because they give the company being paid the ability to withdraw money from your account whenever they wish and take payments of different amounts without consulting you.

Most payday loan companies use CPAs to collect your repayments. However, you can cancel this at any time by consulting with either your lender or your bank. If you do cancel a CPA, make sure you arrange to make repayments by another means. If you miss a repayment, it will affect your credit score and potentially cost you extra in fees and additional interest.

Can I use a payday loan broker?

You may wish to consider using a payday loan broker. Brokers will usually have a panel of lenders that they refer applicants to, so if you’re not successful with one, your application is passed to the next, then the next, and so on. You’ll only have to complete a single application form with the broker rather than going through the process several times with different lenders.

What is APR?

The annual percentage rate (APR) is a measure designed to help consumers compare loans from different providers.

All payday or short term loan providers must calculate the APR of their products and services using the same calculation. It’s calculated based on a 1 year term (even if the loan is only for 1 month), which can make already-high rates seem even higher. It also takes into consideration both the interest and charges.

While APR is certainly useful to compare short term loans and makes it clear how they are much more expensive than other kinds of loans, it doesn’t really tell the whole story. It’s important to consider other factors besides the representative APR, namely the total amount repayable.

How much your loan costs depends on how much you borrow, the interest rate charged and the term of the loan. Payday loans are, by design, an expensive form of credit and are usually geared towards people who have trouble finding credit from more mainstream sources, such as banks and credit unions. It’s always important to be clear about the fees and charges involved when taking out a short term loan.

What will I definitely have to pay?

Interest. This is calculated as a percentage of the amount borrowed and is usually charged daily for payday loans.

What might I have to pay?

Late payment fees. If you’re late on a payment, you may be charged a fee by your lender. These fees are regulated by the government.

Fees charged by your bank. If the lender attempts to withdraw money from your account and there are insufficient funds, your bank may authorise the payment but charge you an unauthorised overdraft fee. Make sure you have enough money to cover your repayments on the day they are due.

What can I use my payday loan for?

Though payday loans can be used for a wide range of purposes, they’re generally designed to cover unexpected expenses. Common uses for payday loans include forgotten bills, car repairs, emergency medical expenses or any other sudden event. Payday loans are unlikely to help when it comes to ongoing financial issues, however.

Here are some common scenarios:

You need…

Could a payday loan help?

To fix a fault on your car, costing around £400

Potentially

To fix your laptop, costing around £100

Potentially

To replace a broken heating element, costing around £100

£50 each month to top-up your income and tide you over

No, it wouldn’t be suitable

To spread the cost of a new £600 sofa over 10 months

No, it wouldn’t be suitable

Are payday lenders regulated by the government?

The rise of payday loans brought about a number of unscrupulous lenders that were exploiting borrowers with extortionate interest rates, fees and penalties. In 2014, the Financial Conduct Authority (FCA) took over regulation of this area and brought in new rules to rein in outrageous lending practices.

Interest cap of 0.8% per day. Interest and fees must not exceed 0.8% per day of the amount borrowed. That’s £4 per £500.

Fixed default fees capped at £15. If borrowers fail to make a payment on time, the default charge must not exceed £15.

Total cost cap of 100%. Borrowers must never have to pay back more in fees and interest than the original amount borrowed.

Rollover cap. Under the new FCA rules, you can only roll over your loan twice.

Frequently asked questions

First off, make sure you’ve exhausted all other borrowing options before deciding to take out a payday loan.

Next, you should compare lenders and loan durations to find the cheapest loan that would be affordable for you. You can get an idea of the repayments using the table above.

Once you’ve chosen a lender (and checked that you’re eligible to apply), the entire application usually takes place online. You’ll need to give the lender enough details to run a credit search (like your address history for the last 3 years), and you’ll then find out whether or not you’ve been accepted.

If you’re formally offered the loan, make a note of the terms and the repayment amounts (and dates) and ensure you have enough in your account to repay your loan.

Speak to your lender if you have any questions, and always contact them as early as possible if you are struggling to make a repayment.

When applying, you’ll need to provide your full name and date of birth, as well as up to 3 years of address history to enable a credit check, plus details of your income and outgoings.

Payday and short term loan companies often look beyond poor credit but will need to make sure they only offer you a loan that would be affordable.

In rare cases, you may be asked to provide additional documentation.

Some short term lenders in the UK will request access to your online banking. This sometimes requires you to provide your login details (if you don’t trust the lender, then don’t do this) or may alternatively require you to log in to your internet banking to give your bank permission to legitimately share transactional data with a specific third party. (Your bank will verify that the lender is authorised before securely sharing your data).

Payday and short term loans are typically for sums of between £50 and £1,000. One of the main factors that dictates how much you can borrow is how much you can afford to repay each month (or week or fortnight). Lenders might not be dissuaded by bad credit, but they will care about affordability.

If you opt to borrow over a longer timeframe, you can usually reduce the size of each repayment – potentially making the loan more affordable – but this will push up the overall cost. Bear in mind that if it’s the first time you’re using a lender, they’ll want to start fairly small. Similarly, lenders may see a longer loan term as a greater chance for a borrower to default.

The majority of lenders will take the necessary funds from your account on the same day you get paid but won’t take the money directly from your pay. In other words, it won’t show up on your payslip – your pay will land in your account, and then shortly after, the payment will be deducted from your account.

It’s usually incredibly quick, with some lenders promising “instant” loans. Realistically it can take as little as 15 minutes, although some lenders are slower outside of office hours.

Many payday lenders allow you to pay off your loan early without incurring any extra fees. Contact your payday loan credit provider if you need to organise an early payment.

This is often possible at the lender’s discretion. Payday loans are regulated by the government and designed to be a “stop-gap” solution to financial problems. There are restrictions around “rolling over” loans. If you find yourself needing more than 1 payday loan, you should consider other forms of credit or seek debt counselling. You can read more about alternatives to payday loans at moneyhelper.org.uk and also in our own comprehensive guide.

If you make all your repayments on time, a lender may approve you for another loan. Some lenders have benefits for repeat borrowers, such as increased borrowing amounts, quicker funding or slightly better rates. But keep in mind these loans are not a long-term solution, and if you frequently need to borrow money, you may need to consider a longer term borrowing option or a more stable line of credit.

UK payday loan companies use a secure online system. Payday loan applications are generally carried out on a secure online application form to help protect your privacy. The system uses a 128-bit secure server and SSL encryption to ensure your personal information cannot be stolen.

To verify your income, some payday lenders need a snapshot of your account for the past 90 days. The services involved are safe and secure and only provide a “read-only” view of your account. There are no personal details transmitted, and no access to any other information besides your financial history is needed.

It’s possible to get a payday loan on a Sunday from a few online lenders that may be able to get your application approved quickly, and the funds sent to you on the same day, no matter what day it is.

Other lenders may let you apply and approve your loan on a Sunday, but won’t send you the funds until Monday – the next business day.

We compare payday/short term loans from

Sources

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Chris Lilly is Head of publishing at finder.com. He's a specialist in personal finance, from day-to-day banking to investing to borrowing, and is passionate about helping UK consumers make informed decisions about their money. In his spare time Chris likes forcing his kids to exercise more.

See full bio

Chris's expertise

Chris

has written

516

Finder guides across topics including:

Rachel Wait is a freelance journalist and has been writing about personal finance for more than a decade, covering everything from insurance to mortgages. She has written for a range of personal finance websites and national newspapers, including The Observer, The Mail on Sunday, The Sun and the Evening Standard. Rachel is a keen baker in her spare time.

See full bio

Fund Ourselves (formerly Welendus) offers flexible and transparent peer-to-peer loans of –, repaid over to . Compare its interest rates, total borrowing costs and eligibility terms against a range of lenders.

A payday loan gives you the money you need quickly, even if you have bad credit or low income. But which one is best for your situation?

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.