A credit score is a rating of how well you repay borrowed money.

The most popular credit score model is FICO.

Your FICO credit score will be a number between 300 and 850.

Your credit score is based on the information in your credit reports, including your payment history and how much credit you’re currently using.

Explaining it like you’re five years old: Credit scores

Your credit score is a snapshot of how well you can repay debt.

Think of a credit score like a report card. Instead of grading you on math or history, your credit score is your grade on how well you repay borrowed money. Credit ratings reflect your debt repayment history, how much debt you owe and other things related to borrowing money.

When people say “credit score,” they’re probably talking about the FICO model, which is the most popular credit-scoring model in the US. Your credit score ranges between 300 and 850, and a higher number is better.

If you miss payments on your mortgage and have debt in collections, your credit score can go down. But if you pay all your bills on time and keep your credit card debt low, your credit score can go up.

I’m being very general here, and there is more to credit scores, but you get the idea. Manage your debt well, and your credit score is likely to increase over time.

Let’s expand: More on credit scores

Now that we’ve covered the basics, let’s get into a little more detail on credit scores and credit reports.

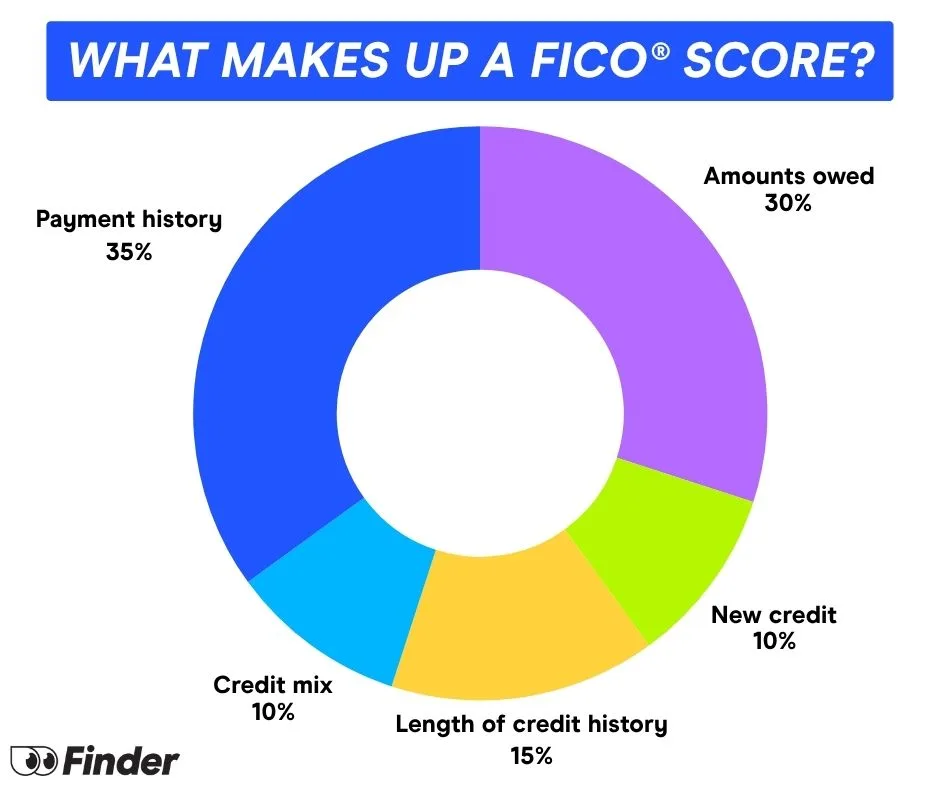

What makes up a credit score?

Payment history. Factors in your on-time, late or missed payments, and is the most important part of your overall score.

Amounts owed. Factors in the balances you owe across your accounts.

Length of credit history. Factors in the average age of your open accounts.

Credit mix. The types of credit you have, primarily revolving credit (like credit cards) and installment credit (like auto loans).

New credit. Factors in how often you apply for new credit.

If your rating is at least 700, you’re in a good spot. A score around that number means you’re likely to qualify for loans with a variety of lenders — if you meet other requirements, that is.

If your credit score is in the 800s, congratulations, because that’s considered excellent credit.

Just like report cards, you can get a bad “grade” on your credit score. The exact number considered a poor or bad credit score depends on who you ask. FICO considers scores under 580 as poor, while many lenders have a 620 to 650 cutoff for loan qualifications.

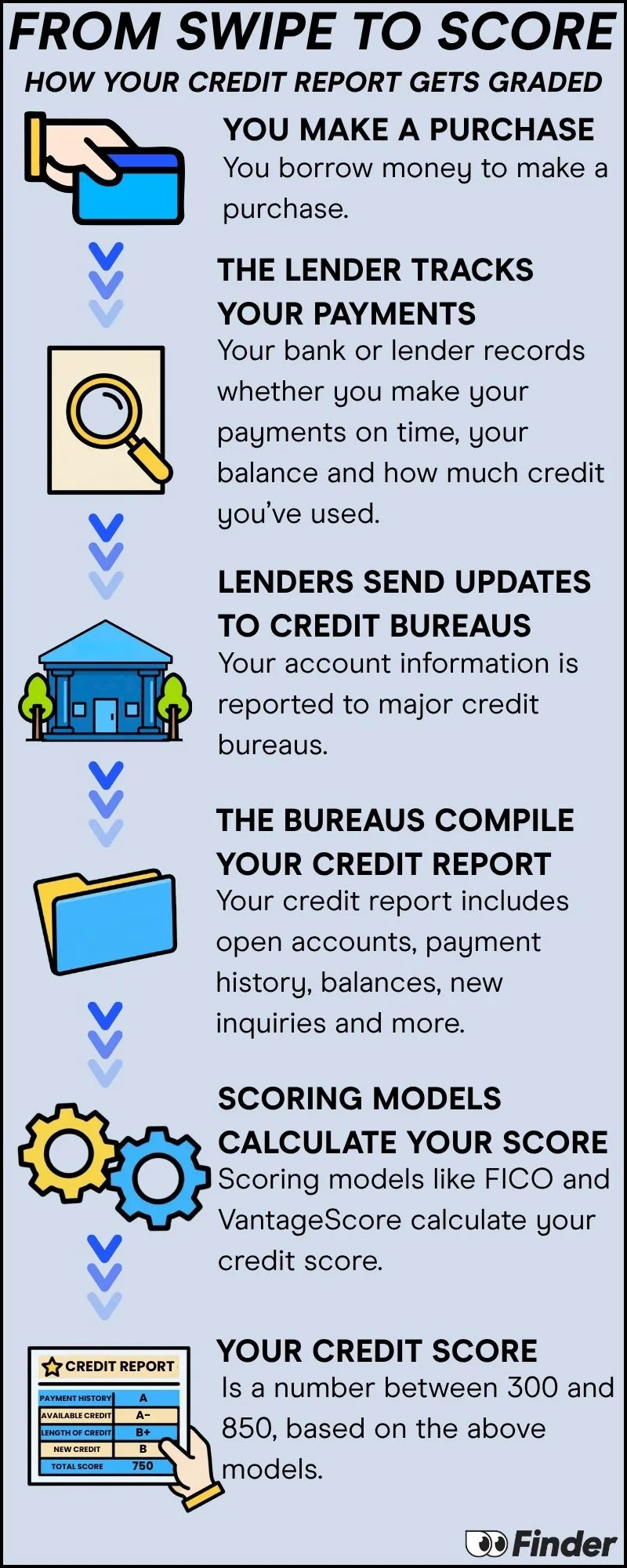

Credit history is tracked with your credit reports— not to be confused with credit scores.

Your credit score is generated by the information on your credit report. Your credit report tracks your open lines of credit, like your credit cards, mortgage payments, auto loans and so on. Credit reports do not track your banking history — that’s on a different report.

There are three main credit bureaus that lenders use to pull your reports: Experian, TransUnion and Equifax.

How do I start improving my credit?

The best thing you can do to improve your credit score is to make your payments on time — payment history is the biggest factor in your credit score, making up 35% of it.

You can check your credit reports for free at the government site AnnualCreditReport.com. You can check your credit score in various ways, but you can go right to the source at myFICO or visit the credit bureaus’ sites.

After reviewing your reports and scores, you can see if you have any mistakes that need correcting, accounts in collections, missed payments that need to fall off or other ways your history may be lacking.

You can now build credit without a credit card. Debit cards that build credit let you build credit with everyday purchases. Compare a few of the most popular options below.

No credit check, interest charges or security deposit

Build credit plus earn up to 4% on savings

Bottom line

Credit scores can sound complicated, and there are certainly a lot of myths surrounding credit scores. But at the end of the day, if you pay your bills on time, keep credit card debt low, avoid debt in collections, avoid repossessions and defaults and don’t need to file for bankruptcy, your credit score is probably in good hands.

The best thing you can do to improve your credit score is maintain an on-time payment history — this category makes up 35% of your entire rating. Keep that in check, and you’re nearly halfway there to a good credit rating.

Bethany Hickey is the banking editor and personal finance expert at Finder, specializing in banking, lending, insurance, and crypto.

Bethany’s expertise in personal finance has garnered recognition from esteemed media outlets, such as Nasdaq, MSN, Yahoo Finance, GOBankingRates, SuperMoney, AOL and Newsweek. Her articles offer practical financial strategies to Americans, empowering them to make decisions that meet their financial goals. Her past work includes articles on generational spending and saving habits, lending, budgeting and managing debt.

Before joining Finder, she was a content manager where she wrote hundreds of articles and news pieces on auto financing and credit repair for CarsDirect, Auto Credit Express and The Car Connection, among others.

Bethany holds a BA in English from the University of Michigan-Flint, and was poetry editor for the university’s Qua Literary and Fine Arts Magazine.

See full bio

Bethany's expertise

Bethany

has written

460

Finder guides across topics including:

The Extra debit card is a debit card that builds credit without charging interest like traditional credit cards do. Review Extra’s features, fees and more.

Step banking accounts help kids and teens learn to manage their money while building their credit scores.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.