It’s tempting to focus purely on the “front end” of sales when you’re starting out, but the real growth bottlenecks often hide in the back end of global operations. When your business needs to pay suppliers in China or settle software fees in Singapore, you want everything to work as efficiently and cost-effectively as possible.

We’re here to walk you through 5 global payment roadblocks – and how to navigate them with the help of WorldFirst.

1 “Slow SWIFT”, the relationship killer

The roadblock

The roadblock

SWIFT payments can slow things down. Late and delayed payments that arrive 5 days after sending create bottlenecks – and frustration. This can lead to slower shipments and fractured supplier relationships. When you’re trying to grow and expand your business on a global scale, trust and speed are 2 key elements that you want to nail.

The fix

The fix

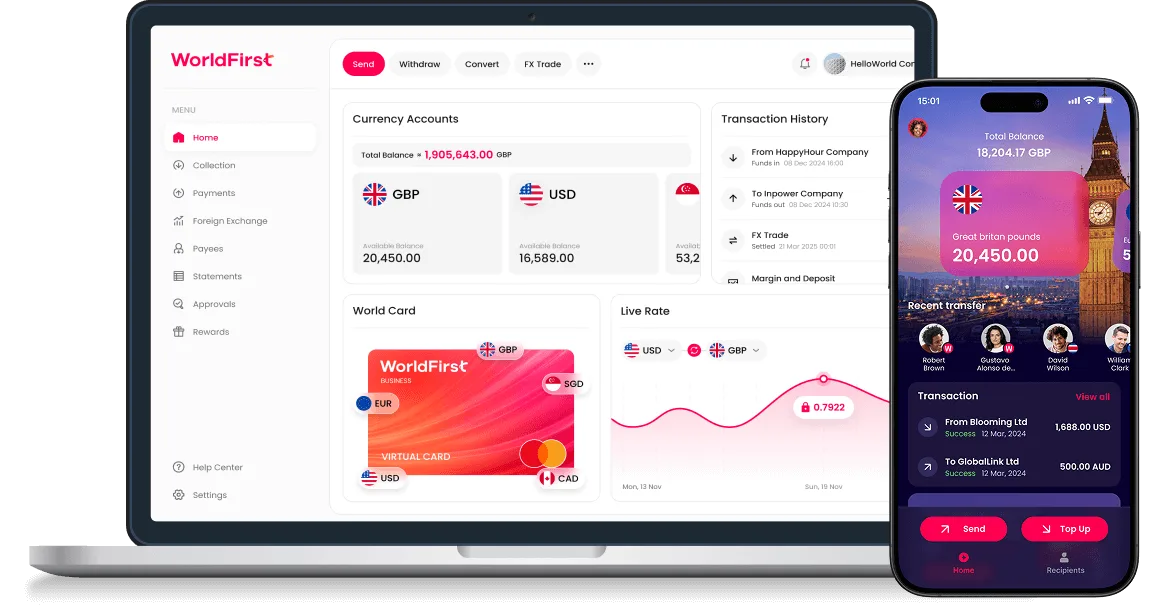

Use the power of local currency accounts. These enable you send payments that can arrive the same day (around 90% do) using local payment networks, keeping your suppliers happy and goods moving. Services like WorldFirst offer local accounts for major currencies, including USD and CNY.

If you want things to move even faster – and your suppliers also have a WorldFirst account – you can make free and instant peer-to-peer payments. This is especially useful if you’re sourcing from China, as 150,000+ Chinese suppliers currently use the platform.

2 Cracking China’s payment maze

The roadblock

Navigating China’s banking system, the Cross-Border Interbank Payment System (CIPS), can be the ultimate test for UK exporters. There’s strict documentation required, and it’s easy to get trapped in “compliance” reviews for days if the purpose codes or invoice data don’t align with mainland regulations, causing unnecessary delays.

The fix

Find a business payments platform that has direct payment routes with China’s top banks. WorldFirst has close partnerships with local Chinese banks, built from existing relationships via their parent company, Ant International. This means you can make same-day payments with real-time payment tracking (if made within the local bank’s processing time, between 09:30-15:00 China Standard Time).

WorldFirst is also the official payment partner to 1688.com (part of Alibaba), where businesses can source goods directly from Chinese suppliers at local wholesale prices. Payments here are free and instant – just like paying the 150,000+ suppliers who also use WorldFirst.

3 The double conversion trap

The roadblock

The double conversion trap is a silent margin killer. If you operate with a single currency account, but sell in Singapore Dollars (SGD), your bank will force a conversion to Pounds Sterling so that the value can be deposited. This means you lose a percentage on the exchange markup. Then, if you need to pay a Singapore-based partner or supplier, you’ll have to buy SGD back from your bank, losing out once again.

The fix

You can sail right through this roadblock with the help of local currency accounts. Set one of these up, and you’re free to receive money from international customers to your own unique account number in the local currency of your choice.

WorldFirst has local currency accounts for 20+ currencies, including GBP, EUR, SGD, HKD, CNY and USD. Plus, they can be set up online without the need for a local address or visiting a branch. And for new WorldFirst customers opening a World Account in 2026, they can enjoy an exclusive FX rate of just 0.3%.

4 The Brexit payment penalty

The roadblock

In a post-Brexit Europe, many EU banks now treat euro transfers coming from UK businesses as “international” transfers and apply an “intermediary fee” as a result. Or, in some cases, they reject the payment because the sender’s IBAN is marked as “non-EU”. Where businesses used to enjoy seamless cross-border transactions, now they can face increased fees and administrative costs.

The fix

As a UK SME, it pays to have a reliable payment partner to navigate post-Brexit international payments. With WorldFirst, you can get a local European IBAN with its World Account. You can then use this to make your Single Euro Payments Area (SEPA) payments and remove the post-Brexit payment headache. Setting up an account is totally free, and there are zero monthly fees.

5 When payments don’t add up

The roadblock

For many UK businesses, payments aren’t the biggest headache; it’s balancing the books at the end of the month. When you’re operating on a global scale and receiving international payments from various sources, you can end up with invoice numbers stripped out or batch payments that don’t match your records. All of this can require hours of detective work just to reconcile everything.

The fix

You can reduce errors and streamline your accounting process by connecting your accounting software to your global payments solution. WorldFirst connects to Xero or NetSuite, both of which help you to keep accurate and automated data and can save you time and money. You can reconcile transactions in 20+ currencies and sync transactions automatically.

WorldFirst can also provide an API to provide easy and flexible integrations to larger businesses that want to give their customers direct access to global currency accounts and payments from their existing platform.