Finder maintains full editorial independence to ensure for our readers a fair assessment of the products, brands, and services we write about. That independence helps us maintain our reader's trust, which is what keeps you coming back to our site. We uphold a rigorous editorial process that ensures what we write and publish is fair, accurate, and trustworthy — and not influenced by how we make money.

We're committed to empowering our readers to make sound and often unfamiliar financial decisions.

We break down and digest information information about a topic, product, brand or service to help our readers find what they're looking for — whether that's saving money, getting better rewards or simply learning something new — and cover any questions you might not have even thought of yet. We do this by leading with empathy, leaning on plain and conversational language that speaks directly, without speaking down.

You’re 25 years away from retirement if you plan to start your golden years at age 65, so you’re probably wondering if you have enough to retire comfortably. You may be paying off a mortgage and saving for a kid’s college education. Saving at age 40 can be challenging, considering the different financial priorities you may have, but any money you have saved and continue to save can benefit from compound interest and investment earnings.

How much money should I have in savings at 40?

The average retirement savings for someone in the gen Y population is $91,191, according to Finder’s Consumer Confidence Index. As of 2023, the age range for millennials — gen Y — is between 27 and 42, putting a 40-year-old near the tail end of this population. Finder data shows that millennials, on average, contribute $9,498 each year toward retirement.

Is that enough? It depends on when you want to retire and how much your money can grow over time.

For instance, if you had retirement savings of $91,191 by age 40 and earned the stock market’s average historical return of 10% each year for the next 25 years while making no further contributions, your money could grow to just shy of the $1 million mark by age 65 with compounding alone.

This is a hypothetical, of course. The 10% stock market return is a historical average. Some years will be higher, while others will be lower. And making additional contributions will help you build your savings faster.

But since everyone’s financial situation is different, let’s look at some ways you can boost your savings if you feel you’re behind.

How to save money in your 40s

Saving money in your 40s can be a challenge considering retirement savings is more important than it was when you were in your 20s, but you also may have other obligations to meet like raising a family and saving for a child’s college education.

Here are some steps you can take to elevate your retirement savings.

Contribute enough to get your 401(k) match

In 2024, you can contribute a maximum of $23,000 to your 401(k)(1). But depending on your yearly income, maxing out your 401(k) may not be feasible. That’s OK. But you should contribute at least enough to get any available company match. This is perhaps the closest thing to “free money” you’ll ever see. Matching formulas vary by company. For example, your company may match your annual contributions dollar-for-dollar until you’ve contributed 3% of your salary. So, if you’re making $60,000, consider contributing at least $1,800 a year to get $1,800 in matching funds.

Max out your IRA

The median weekly earnings for someone between the ages of 35 to 44 is $1,263 or $65,676 a year ($1,263 X 52 approximate weeks in a year). (2) Taking the common advice of saving at least 15% of your income each year for retirement, the average 40-year-old should save $9,851 a year. At this amount, you’re saving more than enough to max out your IRA.

The maximum contribution to all your IRAs and Roth IRAs for 2024 is $7,000. IRAs let you invest in virtually any security, and their tax benefits are incredibly valuable. Your traditional IRA contributions may be tax-deductible, while Roth IRA withdrawals are tax-free in retirement.

For an extra boost to your savings, consider opening an IRA or Roth IRA through an online broker that offers an IRA matching program. For instance, Robinhood will match up to 3% of your IRA contributions when you subscribe to Robinhood Gold, or 1% without. So, if you contribute the maximum $7,000 in 2024, that’s an extra $210. While this may not seem like a lot at first glance, it’ll help transform your savings over time.

Probability of member receiving $1,000 is 0.026%. If you don’t make a selection in 45 days, you’ll no longer qualify for the promo. Customer must fund their account with a minimum of $50.00 to qualify. Probability percentage is subject to decrease.

Terms and conditions apply*. For 401k rollovers, existing SoFi IRA members must complete 401k rollovers via this link See full terms and For SoFi members without a SoFi IRA, a SoFi IRA must first be opened, and 401k rollover must be completed utilizing Capitalize via this link. SoFi and Capitalize will charge no additional fees to process a 401(k) rollover to a SoFi IRA. SoFi is not liable for any costs incurred from the existing 401k provider for rollover. Please check with your 401k provider for any fees or costs associated with the rollover. For IRA contributions, only deposits made via ACH and cash transfer from SoFi Bank accounts are eligible for the match. Click here for the 1% Match terms and conditions.

Must be a SoFi Plus member at the time a recurring deposit is received into your SoFi Active or Automated investing account to qualify. Bonus calculated on net monthly recurring deposits made via ACH and paid out as Rewards Points. See Rewards Terms of Service. SoFi reserves the right to change or terminate this promotion at any time without notice. See terms and limitations. https://www.sofi.com/sofiplus/invest/#disclaimers

Get 1%–3% match on contributions, IRA transfers and 401(k) rollovers

Choose your investments or get a recommended portfolio of ETFs

Get bigger instant deposits, professional research and more with Robinhood Gold

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Use an HSA as a retirement savings tool

If you have a high-deductible health plan, you could pair it with a health savings account (HSA). An HSA lets you receive tax benefits while saving for qualified health expenses. The money you put in an HSA is tax-deductible, so it may reduce your tax bill or increase your refund. Money also grows in an HSA tax-free, and withdrawals are tax-free as long as you use them on qualified health expenses.

At age 65, you can withdraw money from an HSA for any reason without penalty. However, you’d still owe income tax on the withdrawals.

Switch to a high-yield savings account

The average interest rate on traditional savings accounts is 0.46% APY, according to the Federal Deposit Insurance Corporation (FDIC). However, some of the most competitive high-yield savings accounts pay around 5% APY as of January 2024.

For any cash savings you may need immediate access to, such as an emergency fund or savings for any other short-term goals, a high-yield savings account can help grow your money in a way that’s not possible with a traditional, brick-and-mortar bank.

Check the following table to see how $10,000 with no additional contributions could transform over time in these different savings accounts. Many high-yield savings accounts credit interest daily, which lets your money grow faster. Compare that to a monthly compounding frequency for many traditional savings accounts.

The average credit card debt for millennials is $4,974, according to our research. And credit card debt is among the most costly debt you can have. The average interest rate on a credit card is 21.19%, according to the Federal Reserve Bank of St. Louis.

If you’re paying more in interest on your debt than you’re earning on your investments, you’re technically losing money. One way to boost your savings is to shed any costly debt. You’ll save on interest, and it’ll free up more money for you to contribute toward savings.

Bottom line

The average retirement savings for someone in the gen Y population is $91,191, according to Finder data. But how much money you personally should have saved by 40 depends on your retirement age and goals. Once you come up with a target retirement amount, see if you’re on track and consider the different ways to increase your savings so you can meet your goals on time.

7 of 7 results

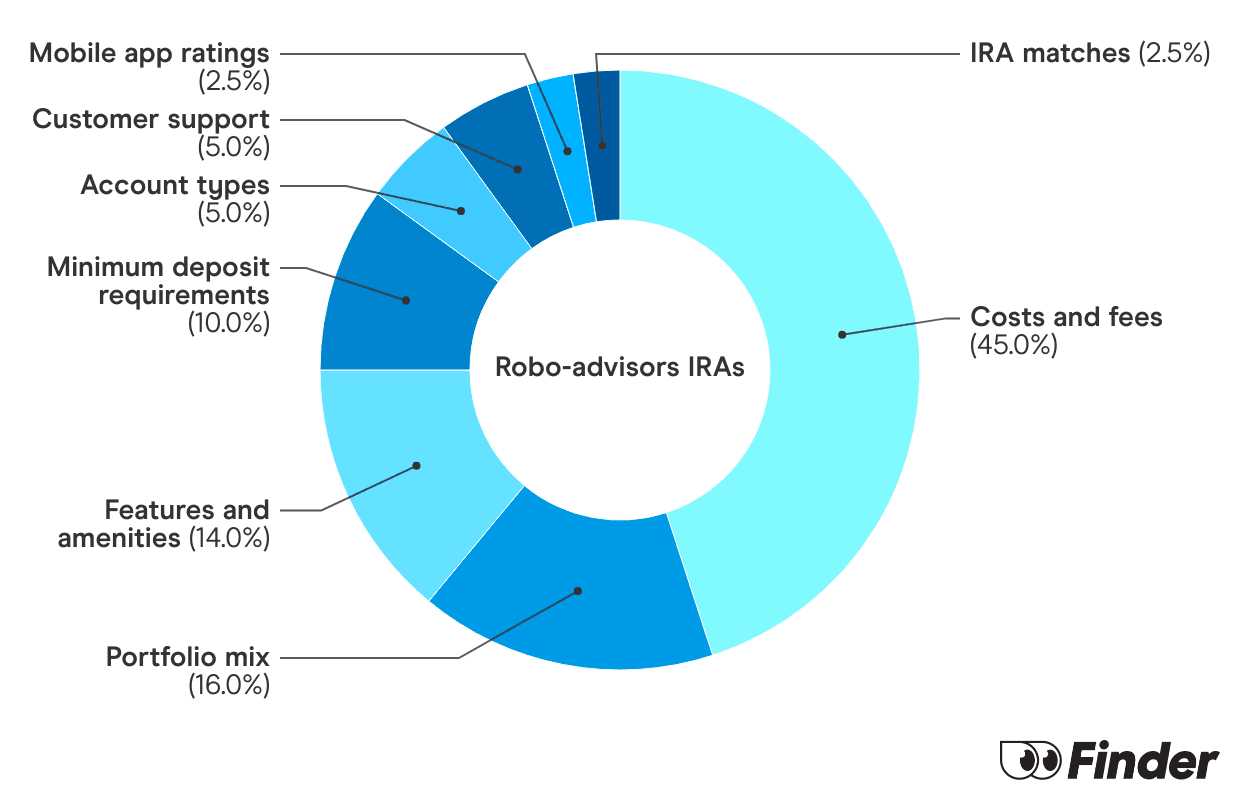

What is the Finder Score?

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Frequently asked questions

Whether having saved $100,000 by age 40 is good depends on when you want to retire and the lifestyle you want to retire in.

A "good" amount of savings depends on different variables. A balance of $50,000 set aside in savings may be more than enough for an emergency fund. If you have retirement savings of $50,000 at age 40, you may need to save more aggressively to reach your retirement goals, depending on what they are.

Javier Simon is a freelance finance writer at Finder and a certified educator in personal finance (CEPF).

He’s featured on NerdWallet, Bankrate, Yahoo Finance and Fox Business, where he’s shared his expertise on personal finance topics, such as investing, retirement planning, taxes, budgeting and savings.

He has also covered breaking news, such as student loan forgiveness initiatives, the housing market and inflation’s impact on consumers’ wallets.

His passion is turning complex financial concepts into actionable content that can help people improve their financial lives.

Javier holds a bachelor’s degree in multimedia journalism from SUNY Plattsburgh.

See full bio

Check out the best IRA providers overall — with guidance on which ones tend to work best for different investing styles.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.