How my credit score dropped 60 points in two years

This post was originally going to be one long humblebrag about my 819 credit score — of which I am extremely proud — and how you too could potentially have such amazing credit one day.

I even pitched it out to my coworkers with an air of haughtiness: “Well, you guys, the preapproval lady from USAA said I have one of the highest scores of anyone she’s talked to under the age of 30. Maybe I should write a post about that.”

Maybe I will someday. But not today.

I thought it best to first confirm my actual number (Maybe it went up, I thought excitedly), and so I signed on to all three credit bureaus to get my score.

After getting hit with a bunch of offers for monthly subscriptions, I finally realized I couldn’t just pay for a one-time score from the bureaus. Instead, I shelled out $60 to the credit reporting site myFICO for my three scores (at $20 a pop).

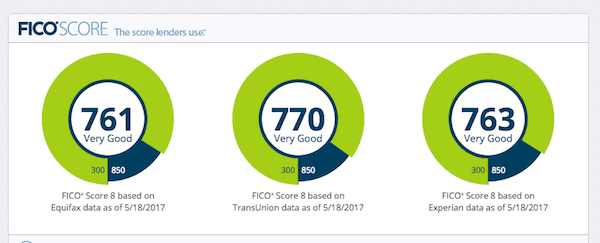

Staring back at me was this:

I’m sorry, come again? What is this “Very Good” bullshit?

What … happened? How did I drop from the Excellent range into merely Very Good — and only two years after that USAA call had inflated my ego to unimaginable heights? We’re talking a nearly 60-point spread here.

The high horse on which I’d paraded around now felt more like a miniature donkey.

Why are credit scores so fragile?

Exploring the negative bullets on my report, I kept coming across “You have a short credit history.” It sounded implausible: My oldest account is 12 years old — more than a third of my life. However, according to the myFICO report, the typical account age for “high achievers” (eye roll) is 25 years.

Looking closer, I find that it’s not about just the age of my oldest account, but also the average age of all my accounts.

Seeing that I took out a car loan three months ago, that pulls the average age of my total accounts down to four years and nine months. MyFICO high achievers hold accounts that average 11 years, again more than double my figure.

I can’t speed up time. I’m 32 and not getting any younger, but account age is not an element I can control. I could presumably pay off my car loan quickly and close it out to bring my average back up. Unfortunately, I don’t have the cash for that. So instead I’ll take the ding to my score and trust that as I pay my loan, it will go back up.

But that’s not all: In looking at my report, I also see a message about the balance on my mortgage. Which means my credit score not only factors in the average age of my credit accounts but also the equity I have in my house and my car.

I bought my house two years ago with 5% down and an FHA loan. It’s going to be a while before I increase my equity to 40% to match the average MyFICO high achiever. Looks like that will come with time as well.

Is a credit score fragile though?

Is a 60-point drop in two years a lot? It depends on who you ask. In those two years, I got two car loans and an FHA mortgage, which I then refinanced a year later. That’s quite a bit of activity in a two-year span.

Some might say my score is doing pretty well for all I’ve put it through.

Because payment history makes up 35% of a credit score, you could argue that my score is somewhat resilient as a result of almost 12 years of credit payments made in full and on time.

Regardless, it’s pretty clear that it’s easier to bring down your score than it is to improve it.

What’s the point of a good score if you don’t use it?

As this story unfolded, I was texting the narrative to a friend of mine.

“HAHA, so much for that 819 score.”

But what’s the point of a good score if you don’t use it? That 819 score I had two years ago got me a 2.8% interest loan on a Prius, a 3.2% interest loan on a Tacoma and a 3.2% mortgage refi.

It’s as if I traded in those 60 points for thousands of dollars in the form of lower interest rates. That’s what good credit scores are used for: getting good rates and terms.

So where do I go from here?

I think it goes without saying that I’ll forgo generating any credit activity for a while to focus on paying down my balances.

I have 819 in my sights. It may take patience, diligence and aggressively paying down my loans to increase my equity — but I will get there. And once I get my score back up, maybe I’ll use it to qualify for a great rate on a loan for … something else. :P

Ask a question