Finder makes money from featured partners, but editorial opinions are our own.

Advertiser disclosure

Is your debt stopping you from finding love?

Would an "I owe you" stop you from saying "I do"?

Was this useful?

Why did you choose this rating?

By

Richard LaycockUpdated

Roughly 37% of American adults say they would reconsider a romantic relationship due to someone’s debt, according to a recent Finder survey. That means if you’ve got debt, you’re narrowing your dating pool by about 98 million adults.

But what is the biggest debt no-no when it comes to love? Roughly 46% of those surveyed say that debts owed to family or friends would be a deal breaker for a potential romantic partner. The next two biggest debt concerns are for credit card and payday loan debt, both at 43%.

It terms of how much debt is “too much”, payday loans have the lowest threshold at an average of $1,732 being the amount at which people would reconsider a relationship. Owing money to family or friends ($5,246) is the second lowest amount of acceptable debt with auto loans ($13,940) the other podium finisher.

Close to two-thirds (38%) of men say won’t date someone if they’re in debt, compared to 36% of women. At 44%, credit card debt was the biggest bugaboo for men, while more than half of women surveyed (57%) owing money to friends or family is a romantic deal-breaker. Mortgage debt is a big dividing line between the sexes, with twice as many men (25%) than women (12%) saying they wouldn’t date someone paying off a mortgage.

Women are far more forgiving with how much debt is too much, with the debt threshold for women ($33,868) more than twice that of men ($15,045).

Close to half of Gen Z (44%) say someone in debt is a non-starter for them in the romantic department. Gen X is at the other end of the spectrum at 32%. Both Gen Y and Gen Z say that credit card debt is the No. 1 issue, whereas for Gen X it’s owing money to friends or family and payday loans for boomers.

It terms of how much debt you’re carrying, $7,863 is too much for Gen Z. That number is about six times higher for Boomers: $44,164.

Payday loan debt is the lowest threshold of debt for both Boomers ($902) and Gen X ($1,734). Gen Y will have issues if you owe $934 for medical bills and Gen Z will not pursue a relationship if you owe family or friends an average of $1,994.

A little over two in five (41%) of those in the Northeast would swipe left on someone with debt, but if you’re in the West that figure is 34%. Owing money to family or friends is the least acceptable debt for both those in the South (47%) and Midwest (51%), while credit card debt is the top choice for both those in the Northeast (37%) and the West (50%).

Payday loans are the least forgivable debt dollarwise, no matter where you live.

The Finder Consumer Confidence Index is an ongoing quarterly survey that captures the perceptions of a nationally representative sample of 2,112 American adults and asked questions related to household finances. Results were collected October 4 to October 19, 2022.

We define generations by the age of participants at the time of the survey:

We define geographical regions according to the divisions of the US Census Bureau.

However, it’s not just whether you have debt, but how you incurred the debt that will be the biggest flag, according to Leif Dahleen from Physician on Fire.

Would debt stop you from forming a relationship — or make you rethink your current who you’re currently with? Yes, say the roughly third (37.82%) of American adults who’d reconsider a romantic partnership due to a partner’s debt.

In general, most people are OK with certain types of debts that involve buying a house or a car, because most people don’t have the kind of money lying around where they can plonk down cash to own them outright. That’s why only 5.79% of Americans said that they would reconsider a relationship with someone who had a mortgage, and 4.76% said they’d have an issue with an auto loan. And the recent pandemic may have made people more sympathetic to medical challenges–only 3.20% said they’d have an issue with medical debt.

The types of debts that might raise questions with a partner are credit card debt (17.25%), loans from friends or family members (16.89%), and payday loans (14.60%).

But it’s not just the type of the debt: Size also matters. When asked how much debt is acceptable, unsurprisingly mortgages had the highest threshold, with the average American willing to be with a partner who owes up to $76,786.29 for their home.

At the other end of the spectrum, Americans are least likely to be with someone who owes as little as $3,160.82 for a payday loan.

Roughly a third of both men and women say they’d reconsider a relationship due to debt. In a switch from last year, men are slightly more likely than women to say that they would do so, with 41.5% of women saying they’d reconsider the relationship, versus 34.7% of women.

As far as the types of debts men and women find unacceptable, men are more likely than women to take issue with a partner having credit card debt or home, home equity, business, student, medical or auto loan. Whereas women are more likely than men to find loans from family and friends and payday loans as unacceptable.

| Type of debt | Men | Women |

|---|---|---|

| Credit card | 18.45% | 16.24% |

| Money owed to family and friends | 14.36% | 19.02% |

| Payday loan | 12.12% | 16.69% |

| Mortgage | 8.56% | 3.45% |

| Business loan | 8.30% | 3.00% |

| Auto loan | 6.19% | 3.56% |

| Home equity loan | 6.19% | 3.00% |

| Student loan | 4.35% | 3.11% |

| Medical bill | 3.82% | 2.67% |

As for how much is too much, men and women draw the line for different types of debts at different amounts. While women say they’re more willing to be with a partner who has debt, men admit to tolerating a larger amount of debt than men do.

For example, men are willing to be with a partner who owns up to $40,260.29 in debt, whereas the cutoff for women is $34,350.93.

| Type of debt | Men | Women |

|---|---|---|

| Payday | $3,231.59 | $3,117.42 |

| Family & friends | $6,154.46 | $3,919.80 |

| Credit card | $9,275.00 | $11,426.59 |

| Medical bill | $14,138.73 | $15,145.13 |

| Auto loan | $22,791.87 | $18,654.78 |

| Student loan | $25,096.82 | $19,970.36 |

| Home equity loan | $22,138.16 | $56,066.71 |

| Business loan | $45,113.30 | $64,062.84 |

| Mortgage | $64,973.54 | $101,554.96 |

45.8% of Gen X say they’d reconsider a romantic partner due to debt, followed by millennials (39.5%) and Gen Z (36.4%). The older generations seem to be more understanding of partner debt with only 34.2% of baby boomers and 25.7% of the silent generation saying they would reconsider a romantic relationship due to debt by a partner.

| Generation | Yes | No |

|---|---|---|

| Gen Z | 36.4% | 63.6% |

| Millennial | 39.5% | 60.5% |

| Gen X | 45.8% | 54.2% |

| Baby boomers | 34.2% | 65.8% |

| Silent gen | 25.7% | 74.3% |

Looking at student debt tolerances across the generations, Gen Z is the least tolerant of student debt with 5.78% of Gen Z saying they would reconsider a relationship with someone who had student debt, compared to only 4.54% of Millennials, 6.77% of Gen X, and 2.50% of Baby Boomers who said the same. Millennials are the least tolerant towardscredit card debt (20.41%) and mortgages (8.84%).

Gen X is the least tolerant of partners who has a business loan (7.55%, an auto loan (8.07%), a home equity loan (6.77%), or medical debt (3.65%). Of the generations, baby boomers come down hardest on partners who have borrowed from family or friends (22.50%) and who have taken payday loans (20.58%).

| Type of debt | Gen Z | Millennial | Gen X | Baby boomers | Silent gen |

|---|---|---|---|---|---|

| Credit card | 16.18% | 20.41% | 17.97% | 16.15% | 10.71% |

| Family & friends | 15.03% | 12.02% | 16.15% | 22.50% | 15.71% |

| Payday | 6.94% | 8.84% | 15.10% | 20.58% | 18.57% |

| Mortgage | 6.94% | 8.84% | 8.59% | 1.92% | Not enough data |

| Business loan | 6.36% | 7.26% | 7.55% | 2.59% | Not enough data |

| Auto loan | Not enough data | 5.90% | 8.07% | Not enough data | Not enough data |

| Home equity loan | 5.78% | 4.54% | 6.77% | 2.50% | Not enough data |

| Student loan | 5.78% | 3.85% | 3.65% | 3.08% | Not enough data |

| Medical bill | Not enough data | 3.40% | 3.65% | 2.50% | Not enough data |

The older generations agree that payday loan debts are hardest to tolerate, with the Silent Generation expressing intolerance for the lowest payday debt amount of $2,160.15, followed by baby boomers at $2,721.38 and Gen X at $2,807.33.

Gen Z was the least tolerant of money owed to family and friends, with a threshold tolerance of $3,548.41. Millennials were the least tolerant of medical debt with a threshold of $4,251.28.

Finder’s data is based on an online survey of 1,658 US adults born between 1928 and 2003 commissioned by Finder and conducted by Pureprofile in January 2021, with representative quotas for gender and age. Participants were paid volunteers.

We assume the participants in our survey represent the US population of 254.7 million Americans who are at least 18 years old according to the July 2019 US Census Bureau estimate. This assumption is made at the 95% confidence level with a 2.36% margin of error.

Our survey questions asked people whether they would reconsider a romantic relationship due to a partner’s debt, the types of debt they found unacceptable and the amounts of debt they found unacceptable by debt type. Possible debt types were: Mortgage, Business loan, Home equity loan, Student loan, Medical bill, Auto loan, Credit card, Money owed to family and friends, and Payday loan.

Average calculations of unacceptable debt are based on participants who expressed an unacceptable debt amount for that particular debt type — for example, to calculate the mean amount of unacceptable mortgage debt, the participants who selected that they would not reconsider a romantic relationship due to a partner’s debt and the respondents who responded “0” (meaning they may find another type of listed debt as unacceptable, but do not find any amounts of mortgage debt to be problematic) were not included.

To avoid skewing the data, we also excluded extreme outliers from our calculations.

We define generations by birth year according to the Pew Research Center’s generational guidelines:

However, it’s not just whether you have debt, but how you incurred the debt that will be the biggest flag, according to Leif Dahleen from Physician on Fire.

Would debt stop you from forming a relationship — or make you rethink your current who you’re currently with? Yes, say the roughly third (33.78%) of American adults who’d reconsider a romantic partnership due to a partner’s debt.

In general, most people are OK with certain types of debts that involve buying a house or a car, because most people don’t have the kind of money lying around where they can plonk down cash to own them outright. That’s why only 4.54% of Americans said that they would reconsider a relationship with someone who had a mortgage, and 3.15% said they’d have an issue with an auto loan.

The types of debts that might raise questions with a partner are credit card debt (16.92%), payday loans (16.3%) and loans from friends or family members.

But it’s not just the type of the debt: Size also matters. When asked how much debt is acceptable, unsurprisingly mortgages had the highest threshold, with the average American willing to be with a partner who owes up to $255,688.80 for their home.

At the other end of the spectrum, Americans are least likely to be with someone who owes as little as $1,476.85 for a payday loan.

Roughly a third of both men and women say they’d reconsider a relationship due to debt. Women are slightly more likely than men to say that they would do so, with 35.81% of women saying they’d reconsider the relationship, versus 30.69% of men.

As far as the types of debts men and women find unacceptable, men are more likely than women to take issue with a partner having a home, business, student, medical or auto loan. Whereas women are more likely than men to find loans from family and friends, home equity loans, payday loans and credit card debt as unacceptable.

As for how much is too much, men and women draw the line for different types of debts at different amounts. While men say they’re more willing to be with a partner who has debt, women admit to tolerating a larger amount of debt than men do.

For example, women are willing to be with a partner who owns up to $120,230.01 in debt, whereas the cutoff for men is $109,127.68.

Baby boomers may associate with free love, but it turns out that love might have a price tag, with 35.17% of boomers saying they’d reconsider a romantic partner due to debt. Millennials (34.77%) aren’t far behind, followed by Gen X (31.89%), Gen Z (30.95%) and the Silent Generation (28.95%).

As far as types of debts that the generations find unacceptable, Gen Z is least likely to be with someone who has credit card debt (18.25%), a mortgage (7.14%), a business loan (7.94%) or an auto loan (4.76%).

Millennials are least likely to be with someone who’s borrowed from family or friends (13.54%) or carries student loans (6.31%), debt (5.85%) or a home equity loan (4.77%). Of the generations, baby boomers come down hardest on partners who have debt from a payday loan (20.26%).

All generations agree that payday loan debts are hardest to tolerate, with the Silent Generation expressing intolerance for the lowest payday debt amount: $883.67.

In fact, the Silent Generation across the board is least forgiving when it comes to debt, indicating the lowest acceptable amount in all but two debt categories: credit card debt and auto loans. Gen Z is least forgiving with those two types of debt, albeit with higher thresholds.

Our data is based on an online survey of 2,398 US adults commissioned by Finder and conducted by Pureprofile in January 2020. Participants self-reported birth years from 1928 to 2002, and all were paid volunteers.

We assume the 2,398 participants in our survey represent the US population of 254.7 million Americans who are at least 18 years old, according to the July 2019 US Census Bureau estimate. This assumption is made at the 95% confidence level with a 2% margin of error.

Our survey questions asked people whether they would reconsider a romantic relationship due to a partner’s debt, the types of debt they found unacceptable and the amounts of debt they found unacceptable by debt type. Possible debt types were:

Our 2020 survey asked more in-depth questions than previous years in this series, and, therefore, this data is not comparable to 2019’s survey results.

Average calculations of unacceptable debt are based on participants who expressed an unacceptable debt amount for that particular debt type — for example, to calculate the mean amount of unacceptable mortgage debt, the 66.22% of participants who selected that they would not reconsider a romantic relationship due to a partner’s debt and the 9.39% who responded “$0” were not included.

To avoid skewing the data, we did not include extreme outliers in our calculations.

We define generations by birth year according to the Pew Research Center’s generational guidelines:

Kevin O’Leary, star of ABC’s Shark Tank and Founder of O’Leary Financial Group, seems to confirm our findings. We reached out to seek his expert advice on debt, love and the “money talk.”

O’Leary first discussed harsh truths of relationships. “The majority of unions break up,” he explains. “Marriages within five and seven years, 50 percent fail. Most people think it’s from infidelity. It isn’t. It’s from financial stress. Most marriages can survive infidelity, but they can’t survive financial stress. It’s an incompatible relationship financially.”

O’Leary suggests couples “set goals on a three- to five-year basis and agree on them,” adding, “If you express a financial interest in somebody on, let’s say, the third date or even the second date, that’s a sign you’re really interested in a future with that person.” He adds, “It can be a powerful aphrodisiac.”

According to O’Leary, too much debt starts the second you have “the inability to support it.”

“What happens with people is they make the assumption that they can take on a student debt averaging $58,000 and then start buying crap and putting on $2,000-a-month worth of clothes,” O’Leary explains. “It’s a very simple task: If you’re servicing debt with more than one-third of your free cash flow after taxes from your salary, you’re going to fail. You’re in trouble.”

For the Americans surveyed by finder.com, too much depends on the type of debt and amount you owe. Of all debt, it appears the least “desirable” is credit card debt. However, while least desirable, the average credit card debt amount people say they find most unacceptable falls in the third lowest among all debts: $12,615.96.

Nevertheless, O’Leary is less discriminating. In his view, the type of deal-breaker debt for any relationship should be “any type of debt.”

“If you’re starting a union with someone, say, OK, how much student debt do you have?” — Cohost of ABC’s Shark Tank Kevin O’Leary

Interestingly, for those finder.com surveyed, student loans are in the second spot, with 52% saying this type of debt is unacceptable. The amount of education financing found unacceptable comes in at an average $48,761.15. This is particularly jarring, given two in five Americans graduate with student debt.

In third place is payday loan debts, with 49% of those surveyed saying these types of debts are unacceptable. However, payday loans come with the lowest threshold for the amount of debt considered acceptable: $4,885.52.

| Type of debt | % |

|---|---|

| Credit card | 56% |

| Student loan | 52% |

| Payday loan | 49% |

| Mortgage | 49% |

| Auto loan | 49% |

| Personal loan | 45% |

| Medical bill | 45% |

| Family and friends | 42% |

| Home equity loan | 39% |

| Business loan | 39% |

If you’ve ever been tempted to tell financial fibs, O’Leary says don’t. “You can’t lie about money,” he insists. “You have to be transparent about it, particularly in a relationship. You might as well fess up to it, because it’s going to come out one way or another. It always does. You can’t avoid it.”

The money talk can be difficult, but it’s a key discussion for any relationship. “People should realize in a relationship, there’s always a third person there. It’s called money. It’s always there. It’s sitting right beside you,” O’Leary says. “The best way to work with it is to have a good relationship with it, and not a secret one. Be open and transparent.”

O’Leary believes that “great financial pillars keep people together for their whole lives.”

Overall, women are more likely than men to shy away from a romantic partnership if their paramour has debt. Men are more likely to hesitate if a partner owes either student loan or mortgage debt. However, women are more likely to take issue with debts related to payday loans, auto loans, personal loans, credit cards, medical bills and home equity loans.

| Type of debt | % of women | % of men |

|---|---|---|

| Student loan | 51% | 52% |

| Mortgage | 48% | 50% |

| Payday loan | 51% | 47% |

| Auto loan | 49% | 48% |

| Family and friends | 42% | 42% |

| Personal loan | 46% | 45% |

| Credit card | 56% | 55% |

| Medical bill | 46% | 43% |

| Home equity loan | 40% | 39% |

| Business loan | 39% | 39% |

There’s also disparity in how much debt is unacceptable. The highest amount considered unacceptable for men looking for a potential partner involves a business loan at $196,541.56. Whereas, the top figure for women is a partner with a mortgage of $272,995.37.

It looks like Gen Y might be all about that paper, as they’re most likely to find all categories of debt unacceptable in a mate. Both student loan and credit card debt top their list, with 59% saying they’d steer clear of someone with this type of debt.

For the most part, Gen X and baby boomers flip-flop as most accepting generation of debt, though baby boomers are most open overall.

| Type of debt | % of Baby Boomers | % of Gen X | % of Gen Y |

|---|---|---|---|

| Student loan | 46% | 51% | 59% |

| Mortgage | 46% | 47% | 53% |

| Payday loan | 48% | 47% | 52% |

| Auto loan | 47% | 46% | 54% |

| Family and friends | 37% | 41% | 47% |

| Personal loan | 44% | 44% | 49% |

| Credit card | 56% | 53% | 59% |

| Medical bill | 43% | 42% | 50% |

| Home equity loan | 37% | 38% | 43% |

| Business loan | 35% | 38% | 44% |

“My No. 1 piece of advice is talk about money. Talk about it. It matters. It helps you build a relationship with somebody. Don’t be scared to talk about money. Most people think it’s a turnoff. It isn’t. It’s absolutely a very positive thing when people are getting together. So that’s my No. 1 thing: Just be ready to talk about it. It’s not bad. It’s good for you.”

According to the Federal Reserve Bank of New York, household debt was at an all-time high between 2004 and the third quarter of 2017, when it totaled $12.96 trillion. This is an increase of $280 billion from 2008’s third-quarter peak during that year’s financial crisis.

Many different types of credit commitments contribute to overall household debt, and we weigh each differently according to how we prioritize their importance.

Attempting to dig deep into the details, finder.com surveyed 2,000 Americans to find out which types of debt we find most unacceptable in a partner.

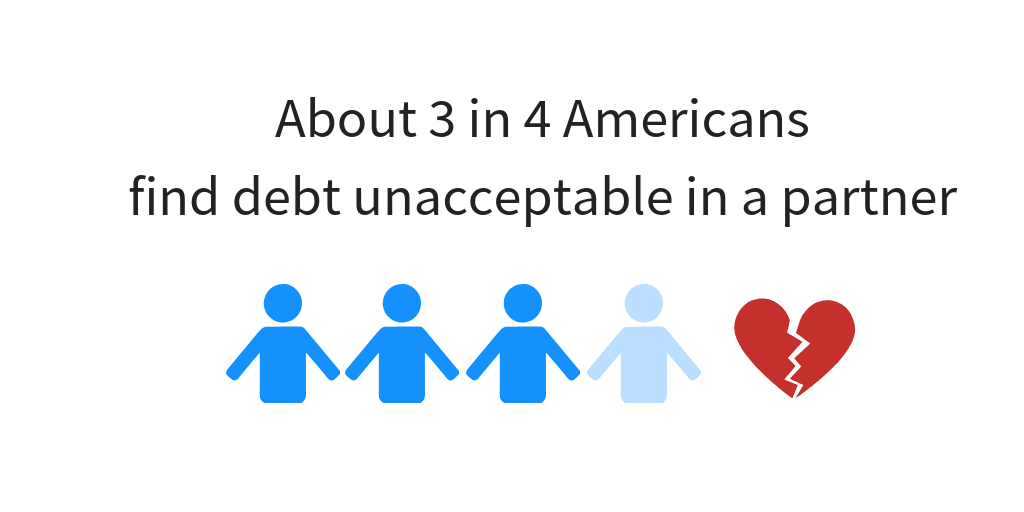

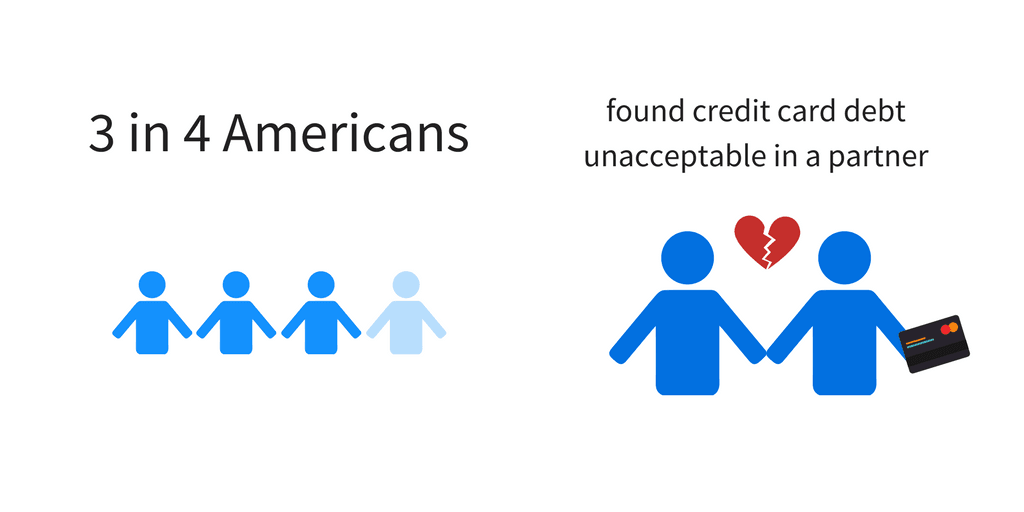

Our survey revealed that of household debts, Americans find credit card debt most unacceptable in a partner — with 77.55% of our respondents saying debt on plastic is most distasteful. Payday loans closely followed at 77.35%.

Some 3 in 4 Americans may not fully appreciate the value a college degree can provide: 76.20% (about 187.14 million) name student loans an unacceptable debt, finding an average $51,000 in debt objectionable. (The good news is that only 1 in 4 students owes $43,000 or more in student loans, according to a 2016 report from the Pew Research Center.)

More Americans find it harder to accept a partner’s need to borrow money for medical purposes than they do for a business loan. Americans find business loans the most tolerable type of debt, with an estimated 70.90% considering borrowing for a business unacceptable in a partner, followed by home equity loans at 71.25% and medical bills at 72.20%.

| Debt | Average amount considered unacceptable | Proportion of respondents who consider each debt unacceptable |

|---|---|---|

| Student loan | $51,000 | 76.20% |

| Mortgage | $305,745 | 72.85% |

| Payday loan | $1,830 | 77.35% |

| Auto loan | $27,298 | 72.55% |

| Family and friends | $6,092 | 73.95% |

| Credit card | $11,525 | 77.55% |

| Medical bill | $35,221 | 72.20% |

| Home equity loan | $77,193 | 71.25% |

| Personal loan | $25,905 | 72.80% |

| Business loan | $153,166 | 70.90% |

Source: finder.com

| Debt | Proportion of women who consider each debt unacceptable | Proportion of men who consider each debt unacceptable |

|---|---|---|

| Student loan | 75.69% | 76.73% |

| Mortgage | 72.35% | 73.37% |

| Payday loan | 77.06% | 77.65% |

| Auto loan | 72.35% | 72.76% |

| Family and friends | 75.49% | 72.35% |

| Credit card | 77.75% | 77.35% |

| Medical bill | 72.06% | 72.35% |

| Home equity loan | 71.27% | 71.22% |

| Personal loan | 72.65% | 72.96% |

| Business loan | 70.78% | 71.02% |

Source: finder.com

More baby boomers than any other generation consider all debts except student loans unacceptable in a partner. Whereas millennials are least tolerant of student loans, more than 4 in 5 of them consider it unacceptable in a partner.

Gen Xers appear the most tolerant generation when it comes to debt in any form. However, Gen X finds payday loans (74.67%) slightly more unacceptable than credit cards (74.01%). Baby boomers are consistent with the general population trend: 81.36% find credit cards most unacceptable, followed by payday loans (80.83%) and student loans (76.96%). The most unacceptable loans for millennials are student loans at 80.04%, credit cards at 77.19% and payday loans at 76.17%.

| Debt | Proportion of baby boomers who consider each debt unacceptable | Proportion of Gen Xers who consider each debt unacceptable | Proportion of millennials who consider each debt unacceptable |

|---|---|---|---|

| Student loan | 76.96% | 72.96% | 80.04% |

| Mortgage | 75.23% | 69.53% | 74.34% |

| Payday loan | 80.83% | 74.67% | 76.17% |

| Auto loan | 75.63% | 68.47% | 74.13% |

| Family and friends | 76.43% | 70.71% | 75.15% |

| Credit card | 81.36% | 74.01% | 77.19% |

| Medical bill | 76.17% | 68.34% | 72.10% |

| Home equity loan | 74.97% | 66.75% | 72.51% |

| Personal loan | 76.30% | 68.60% | 73.93% |

| Business loan | 74.30% | 66.49% | 72.51% |

Source: finder.com

Richard Laycock, Insights editor and senior content marketing manager

Sign up for the Finder newsletter

We know what the best deals in personal finance on the market are at all times, and now you will too.

By clicking Subscribe I agree to the Privacy and Cookies Policy, Terms of Use and to receive emails from Finder.

Richard Laycock is Finder’s NYC-based lead editor & insights editor, spending the last decade data diving, writing and editing articles about all things personal finance. His musings can be found across the web including on NASDAQ, MoneyMag, Yahoo Finance and Travel Weekly. Richard studied Media at Macquarie University, including a semester abroad at The Missouri School of Journalism (MIZZOU). See full bio

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.