What is a good credit score? Ranges, factors and how to check

Your credit score determines your borrowing power — do you know yours?

The average FICO Score in the US is 715, according to FICO’s 2025 data. That puts the typical American in the “good” credit range. You can check your credit score on select credit card or loan statements, through a nonprofit counselor or with a free credit score service.

What is a credit score?

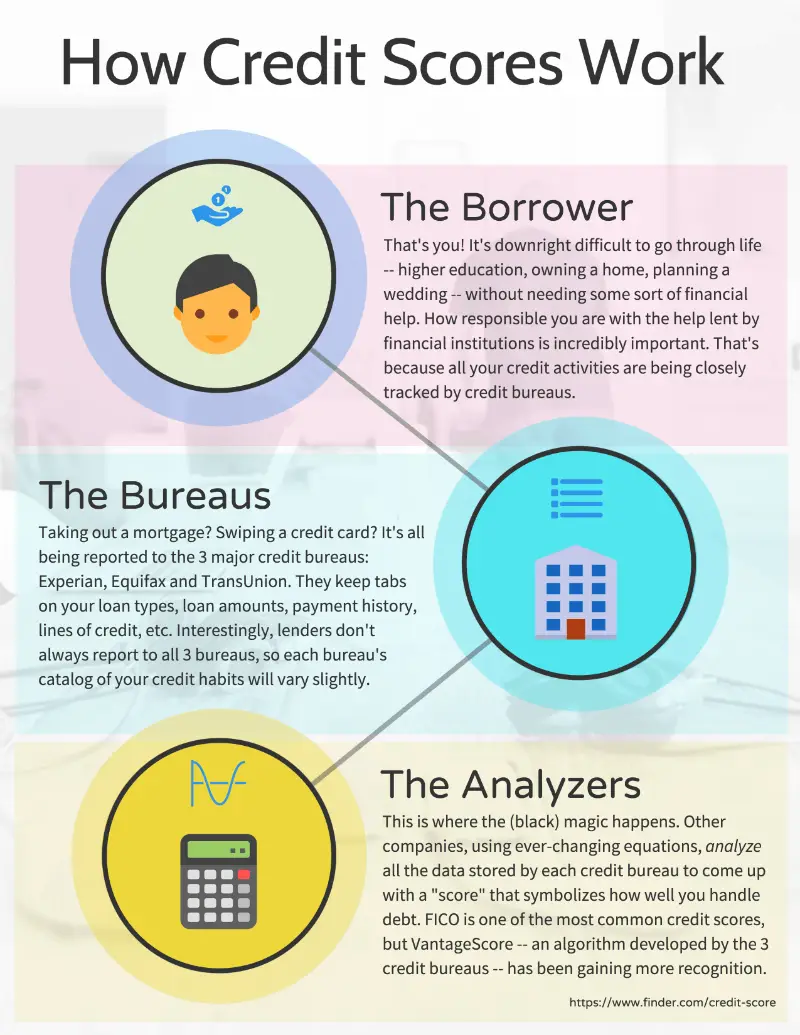

Your credit score is a three-digit number between 300 and 850 that represents your credit history, including your payments and defaults. Lenders use your credit score to predict how likely you are to repay a loan on time.

The higher your credit score, the better your odds of approval for financial products with low interest rates and flexible terms. It can also affect how much you’ll pay for car insurance in most states and what landlords charge for rent.

The “big three” credit bureaus — Equifax, Experian and TransUnion — calculate your credit score based on proprietary algorithms that weigh different factors of your credit history.

What is a good credit score?

A credit score of 670 or higher is generally considered “good.” About 71% of Americans have a good credit score or better, according to Experian. Most lenders are far more likely to approve those with good credit scores for loans and offer better terms and rates.

Scoring systems vary depending on which model provides your score. However, they’re similar in that the higher the credit score, the better your chances of being approved for a low-rate loan.

Borrowers with good credit or higher are typically delinquent on payments less than 5% of the time. This gives lenders confidence that loans extended to these borrowers will be paid back on time.

A credit score of 740 or higher is considered very good, and 800 or above is exceptional. Consumers in these ranges are the easiest for lenders to approve and typically receive the best interest rates. About 23% of Americans have an exceptional FICO Score of 800 or higher.

Credit score ranges

There’s more than one model for calculating credit scores, and lenders and bureaus weigh the information in your credit history differently. However, two scores are widely used: your FICO Score and your VantageScore.

Both scoring systems consider similar factors when determining your credit score, including how long you’ve had credit, your payment history, your credit utilization rate and how many loan products or other types of credit you carry. However, lenders use FICO Scores in about 90% of credit decisions, which makes it a good barometer for how potential lenders might see you when determining approval.

Credit rating

How a lender sees your credit score

FICO Score

VantageScore 3.0

Exceptional / Excellent

You represent the lowest risk to lenders. You’ll qualify for the best interest rates and most favorable loan terms.

800+

781–850

Very good / Good

You’re more likely than the average American to maintain healthy credit, and it’s unlikely you’ll incur an adverse event in the next 12 months.

740–799

661–780

Good / Fair

You’re less likely to declare bankruptcy, miss a payment on a debt or have a judgment against you, indicating less likelihood of a default.

670–739

601–660

Fair

You’re more likely to incur an adverse event such as a default, bankruptcy or something similar in the next year.

580–669

—

Poor

You’re highly likely to have adverse events listed on your credit report within the coming year, including court judgments, bankruptcies, insolvency or defaults.

579 or lower

600 or lower

Note: FICO and VantageScore use different category labels and ranges. The table above maps them side by side for comparison, but the tiers don’t align one-to-one.

How to understand your score

Several factors affect your overall credit score. The three major credit bureaus — Equifax, Experian and TransUnion — all have their own models for calculating your score, which can result in slightly different scores from each.

Both the FICO Score and VantageScore 3.0 use a range of 300 to 850. Some older or proprietary scoring models from individual bureaus may use slightly different ranges, but the 300-to-850 scale is the standard you’ll encounter most often.

Some aspects of your credit score aren’t completely within your control. For example, if you recently turned 18, are new to the country or new to credit, there’s little you can do to add to the length of your credit history. Also, your credit score doesn’t consider your income, employment status, marital status or place of residence.

How your score is calculated

If you’re trying to maintain or improve your score, you should know what piece of the pie these five factors account for when calculating your FICO Score:

Payment history (35%)

Amounts owed (30%)

Credit history length (15%)

Credit mix (10%)

New credit inquiries (10%)

The “amounts owed” factor looks at your total debt across all accounts, not just credit cards. A key metric here is your credit utilization ratio, which measures how much of your available revolving credit you’re using. Keeping this below 30% is a common guideline, but lower is better.

VantageScore weighs similar factors but groups them differently. Payment history is the most influential factor in both models.

A credit bureau is an agency that collects and files information about your credit history into a report. The three main credit bureaus in the US are Equifax, Experian and TransUnion.

These bureaus don’t make lending decisions when you apply for credit. They simply provide your credit history to the lender.

Equifax. Founded in 1899, Equifax operates in multiple countries and monitors information on hundreds of millions of consumers and businesses worldwide. It also offers products such as credit monitoring, fraud prevention and identity theft protection.

TransUnion. TransUnion maintains reports on consumers across the US and monitors nearly every credit-active individual in the country. It also offers a range of credit and fraud-protection products to consumers and businesses.

Experian. Experian monitors more than 1 billion individuals worldwide as well as millions of businesses. Some of its products include credit monitoring, identity theft protection and its Experian Boost program, which lets you add utility and phone payments to your credit file.

How to get your credit score

Credit card or loan statement. Many major credit card issuers now provide free credit scores to their cardholders, including American Express, Bank of America, Chase, Capital One and Discover. Discover and Capital One allow anyone to check their score, even non-customers.

Free credit score service. Services like Credit Karma and Experian offer free access to your credit score and make recommendations for loan products based on your history and needs.

Nonprofit counselor. Reputable nonprofit credit counselors can access your credit score for free and offer advice on managing your debts, creating a budget and improving your overall score.

Credit reporting companies. You can purchase your FICO Score directly from myFICO.com. These companies typically package access to your score into a monthly membership with other credit services like identity theft protection and fraud monitoring.

Can I get my score from my credit report?

Not usually. Your credit report is a detailed record of your borrowing history, while your credit score is a numerical representation of your creditworthiness based on your credit report. Most credit reports from bureaus don’t contain your credit score.

Your credit report includes:

Your repayment history.

Details of any defaults you may have.

Personal identifying information (name, address, Social Security number).

A record of credit applications and inquiries.

It also contains data held on public records, such as bankruptcies.

Even though your credit report doesn’t typically contain your credit score, it’s important to regularly review your report for any errors. You can get free copies of your credit report from all three bureaus every week through AnnualCreditReport.com. This weekly access was made permanent in 2023.

If you spot errors, you can dispute them directly with the credit bureau that issued the report.

Check your credit report. Review your reports from all three bureaus for mistakes that could negatively affect your credit. You can do this weekly for free at AnnualCreditReport.com.

Stay on top of your bills. Build a history of on-time repayments by signing up for autopay. Payment history is the single most important factor in your credit score.

Pay off your debts. Focus on high-interest debts to lower your debt-to-income ratio and reduce your credit utilization.

Keep your credit cards open. Avoid carrying a balance, but keep older accounts open to maintain a longer credit history and a lower overall utilization ratio.

Consider a secured credit card. A secured credit card can help build or improve your credit score by limiting the amount you spend. Some secured credit cards upgrade you to an unsecured card after a streak of responsible usage.

5 credit score pitfalls

Avoid these five common credit mistakes that could drag your score down:

Having a credit utilization ratio of 30% or more. Lower is better.

Missing or making late payments.

Closing old credit accounts that have reported healthy activity to the three credit bureaus.

Not monitoring each credit report for inaccuracies. Check at least once a year, though weekly is now free.

Making too many hard credit inquiries in a short period.

Frequently asked questions

How does continually carrying a balance affect my credit score?

Carrying a balance increases your credit utilization ratio, which can lower your score. Use your credit card regularly to show you can responsibly manage a line of credit, but pay the balance in full at the end of each billing cycle to avoid extra interest charges and keep utilization low.

How does getting married affect your credit score?

Some people think that once you get married, you have a joint score with your spouse. This is a common credit myth. Marriage has no direct effect on your credit score. However, if you open joint accounts with your spouse, their payment behavior on those accounts can affect your credit.

What is an “adverse event?”

An adverse event refers to a negative item on your credit history, such as a default, bankruptcy, court judgment or personal insolvency.

What is the difference between a FICO Score and a VantageScore?

Both are credit scoring models that range from 300 to 850 and use your credit report data. FICO has been the industry standard for decades and is used in about 90% of lending decisions. VantageScore was created in 2006 by the three credit bureaus and is growing in adoption. VantageScore can generate a score with as little as one month of credit history, while FICO typically requires at least six months.

Holly Jennings is the deputy crypto editor and updates writer at Finder, working with writers across all niches to deliver quality content to readers. She’s edited hundreds of financial articles ranging from credit cards to investments. With empathy at heart, she especially enjoys content that breaks down complex financial situations into easy-to-understand information. Prior to her role at Finder, she collaborated with dozens of small businesses to maximize the reach and impact of their blog posts, website copy and other content. In her spare time, she is an award-winning author for Penguin Random House, writing about virtual reality worlds, magical girls and lasers that go pew-pew.

See full bio

Holly's expertise

Holly

has written

43

Finder guides across topics including:

If you’d like to find out your score, you may generate it through credit agencies available like Equifax, Experian, or TransUnion. Though please keep in that your score differs from the company you request it from. You can find more information from our guide on how you can check your credit rating.

Hope this helps.

Cheers,

May

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

What is my credit score

Hi Dion,

Thank you for your inquiry.

If you’d like to find out your score, you may generate it through credit agencies available like Equifax, Experian, or TransUnion. Though please keep in that your score differs from the company you request it from. You can find more information from our guide on how you can check your credit rating.

Hope this helps.

Cheers,

May