Get the cash you need to cover everyday expenses or chase new opportunities.

While there are several types of working capital financing, they generally come with short terms and don’t require any specific collateral. For this reason, business financing companies tend to have strict eligibility requirements.

Find out what options are available for your business by selecting information about your credit score, time in business and funding needs.

We currently don't have that product, but here are others to consider:

How we picked these

What is the Finder Score?

The Finder Score crunches 12+ types of business loans across 35+ lenders. It takes into account the product's interest rate, fees and features, as well as the type of loan eg investor, variable, fixed rate - this gives you a simple score out of 10.

To provide a Score, we compare like-for-like loans. So if you're comparing the best business loans for startups loans, you can see how each business loan stacks up against other business loans with the same borrower type, rate type and repayment type.

You can get a working capital loan by following these steps — though the order can vary depending on the type of business financing.

Calculate how much working capital you need by using the working capital formula or estimating how much you need to borrow for a new project.

Compare lenders that offer working capital loans, paying attention to the amount of funding available, rates, terms, fees and requirements.

Prequalify with your top choices, usually by filling out a form online. If you’re applying with a bank or factoring company, you might have to call to ask for a quote.

Fill out the application with your top choice after comparing prequalification offers.

Submit any required documents, like recent bank statements, your business balance sheet, accounts receivable and accounts payable.

Review and sign your loan offer, taking note of the rates, terms and due date.

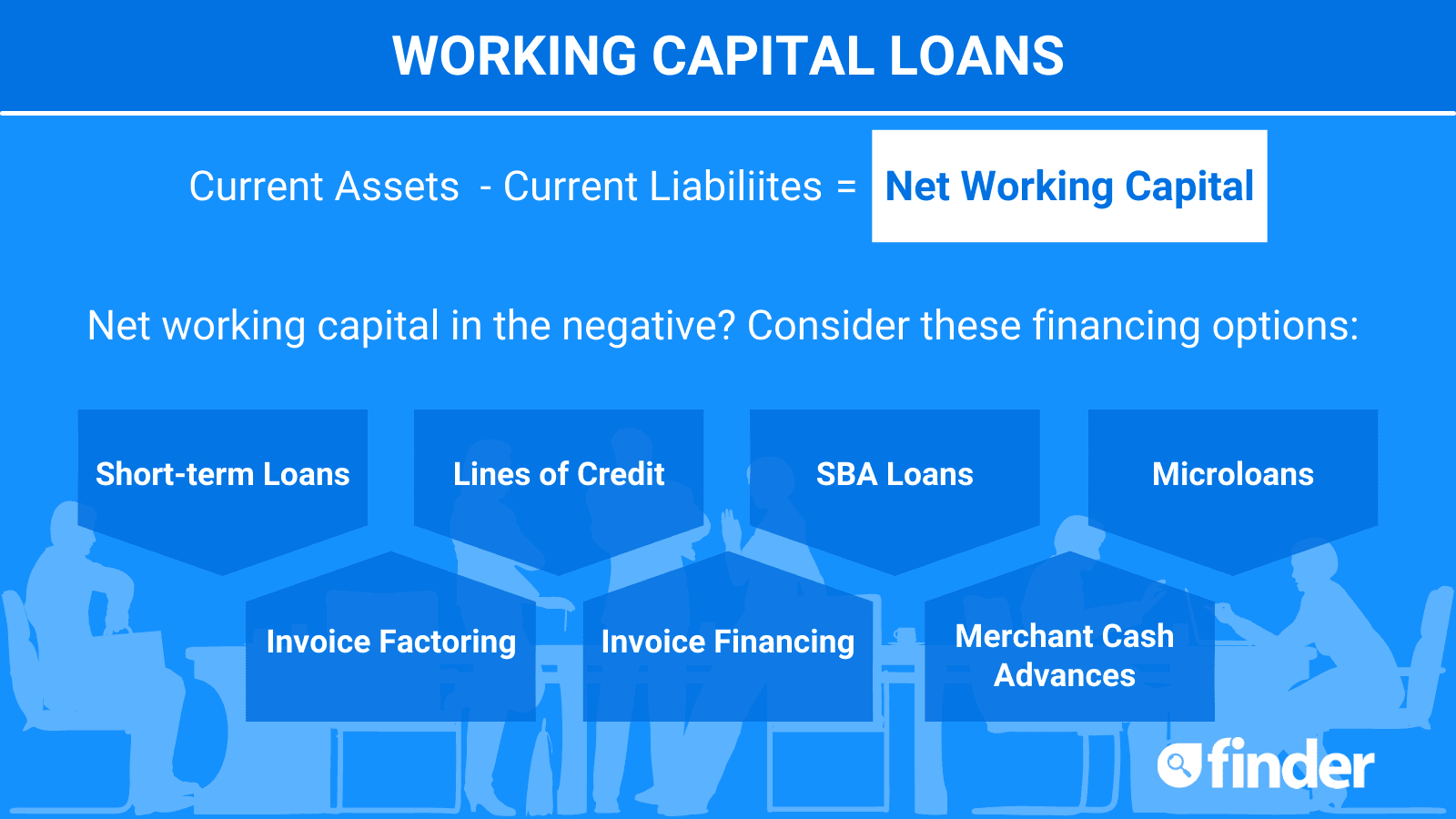

Types of working capital loans and how they work

These are the main types of working capital business loans available through banks, online lenders and any other financial institution.

Short-term loans

Short-term loans are one of the most common type of working capital financing. While long-term loans are designed to finance large projects, short-term loans are designed to cover operating costs.

These give you all of the funds at once, which you repay plus interest and fees in monthly or weekly payments. Usually you can borrow from $1,000 to $500,000, with loan terms between six and 36 months. Rates can start at around 4% APR — but can top 90% APR in some cases.

These are best for businesses that only occasionally need working capital. While many lenders offer discounts to repeat customers, it’s not as convenient as a line of credit.

National Funding is an online lender that offers working capital loans to most small businesses. Its rates are relatively low for an online lender. And its working capital loans come with terms of 12 months or less. But it requires daily payments, which can be difficult for some businesses to manage. And the rates and terms from its partners could be higher than expected.

Loan amount

$5,000 – $500,000

APR

Undisclosed

Min. Credit Score

600

National Funding is an online lender that offers working capital loans to most small businesses. Its rates are relatively low for an online lender. And its working capital loans come with terms of 12 months or less. But it requires daily payments, which can be difficult for some businesses to manage. And the rates and terms from its partners could be higher than expected.

Pros

Low minimum credit score

Funding as soon as next-day

Relatively low rates

Cons

Daily payments

Potentially higher rates from partners

Doesn't disclose costs on website

Loan amount

$5,000 – $500,000

APR

Undisclosed

Min. Credit Score

600

Loan term

24 to 60 months

Requirements

In business 6+ months and make at least $250,000 in annual sales. Other loan types have additional requirements.

OnDeck's short-term business loans are designed for working capital. With minimal paperwork you can borrow as much as $400,000 with a turnaround as soon as the day you're approved in some cases. OnDeck accepts fair credit and has relatively flexible requirements compared to a bank loan — plus it only requires a lien on business assets. But while it offers reduced fees for repeat borrowers, OnDeck's APRs are some of the highest out there. You can likely find a lower rate with another lender, if you can qualify.

Loan amount

$5,000 – $400,000

APR

Average is 56.4% to 56.6%.

Min. Credit Score

625

OnDeck's short-term business loans are designed for working capital. With minimal paperwork you can borrow as much as $400,000 with a turnaround as soon as the day you're approved in some cases. OnDeck accepts fair credit and has relatively flexible requirements compared to a bank loan — plus it only requires a lien on business assets. But while it offers reduced fees for repeat borrowers, OnDeck's APRs are some of the highest out there. You can likely find a lower rate with another lender, if you can qualify.

Pros

Same-day funding available

Reduced fees for repeat borrowers

Reports to business credit bureaus

Cons

High starting APR

Not all industries can qualify

Daily or weekly repayments

Loan amount

$5,000 – $400,000

APR

Average is 56.4% to 56.6%.

Min. Credit Score

625

Loan term

3 to 24 months

Requirements

Companies in business at least 1 year, $100,000+ in gross annual revenue, majority owner with a 625+ personal credit score, active business checking account

A working capital line of credit gives your company access a credit limit, which your company can draw from as needed to cover short-term business expenses. Usually working capital credit limits stop at around $250,000.

This type of financing comes with slightly higher rates and fees than a term loan. Often, each withdrawal turns into a short-term loan, which you repay in installments over a term of six to 12 months.

These are best for small businesses that frequently need access to cash. But it can also be useful to have on hand to cover emergency expenses.

Fundbox is one of the few lenders that truly requires no paperwork on its lines of credit. Instead, it connects with your business's accounting software when you apply. There's no fee to make a withdrawal, and startups as new as six months can qualify for this working capital loan. But it charges weekly repayments and has a lower-than-average credit limit. Longer terms also come with higher rates.

Loan amount

$1,000 – $250,000

APR

Starts at 4.66%

Min. Credit Score

600

Fundbox is one of the few lenders that truly requires no paperwork on its lines of credit. Instead, it connects with your business's accounting software when you apply. There's no fee to make a withdrawal, and startups as new as six months can qualify for this working capital loan. But it charges weekly repayments and has a lower-than-average credit limit. Longer terms also come with higher rates.

Pros

No paperwork

No draw fees

Qualify with just six months in business

Cons

Lower-than-average credit limits

Higher fees for longer terms

Weekly payments

Loan amount

$1,000 – $250,000

APR

Starts at 4.66%

Min. Credit Score

600

Loan term

12 or 24 weeks

Requirements

$30,000+ in annual revenue, 3+ months in business, 600+ FICO credit score, business checking account

A Small Business Administration (SBA) loan is financing backed by the federal government. You can use most SBA loans for working capital, including the popular SBA 7(a) and Express loan programs. The SBA’s Working Capital CAPLine also offers small businesses financing specifically designed to cover everyday business operations.

SBA loans can run as high as $5 million in many cases. But how big of a loan your business can get depends on your business’s financial health. The application process can also take over a month, and lenders require a minimum personal credit score of 620.

Lendio is an online business loan marketplace that can help your small business connect with an SBA lender. Its partners offer SBA 7(a) and Express loans, which your business can use for working capital expenses. Its online platform makes it easier to complete the application and keep track of documents. Plus it has personal funding managers on staff to help you out if you're stuck.

Loan amount

$1,000 – $5,000,000

APR

Varies by lender

Min. Credit Score

580

Lendio is an online business loan marketplace that can help your small business connect with an SBA lender. Its partners offer SBA 7(a) and Express loans, which your business can use for working capital expenses. Its online platform makes it easier to complete the application and keep track of documents. Plus it has personal funding managers on staff to help you out if you're stuck.

Pros

SBA 7(a) and Express loans available

Simplified online application

Staff can help with application

Cons

Takes up to two months to fund after approval

Not a direct lender

Mixed reviews of customer service

Loan amount

$1,000 – $5,000,000

APR

Varies by lender

Min. Credit Score

580

Loan term

3 months to 25 years

Requirements

Operate business in US for 6 months or more, have a business bank account, minimum 580 personal credit score, at least $8,000 in monthly revenue.

SmartBiz is an online connection service that specializes in SBA 7(a) lenders and banks. It also offers packaging services to cut down the turnaround time from months to weeks — for a fee. But it's best for more-established businesses and owners who have good credit. And if you need less than $30,000, another lender is a better choice.

Loan amount

$50,000 – $350,000

APR

Prime Rate, plus 3% to 5.75%

Min. Credit Score

660

SmartBiz is an online connection service that specializes in SBA 7(a) lenders and banks. It also offers packaging services to cut down the turnaround time from months to weeks — for a fee. But it's best for more-established businesses and owners who have good credit. And if you need less than $30,000, another lender is a better choice.

Pros

Offers packaging services

SBA and non-SBA loans

Faster SBA loan turnaround

Cons

Packaging and referral fees

Can still take up to 30 days

Loan amount

$50,000 – $350,000

APR

Prime Rate, plus 3% to 5.75%

Min. Credit Score

660

Loan term

10 years

Requirements

660+ credit score, 2+ years in business, $50,000+ in annual revenue, no bankruptcies or foreclosures in past 3 years

Loan amount

$50,000 – $350,000

APR

Prime Rate, plus 3% to 5.75%

Min. Credit Score

660

Merchant cash advances

Merchant cash advances offer an advance on future credit and debit card sales for consumer-facing businesses. How much you can borrow usually depends on the past three to six months of revenue. And instead of having a loan term, you repay the advance plus a fee with a percentage of your daily sales.

Merchant cash advances are available to businesses in the startup phase and small business owners with bad credit. But it’s one of the most expensive financing options out there, with rates topping 300% APR in some cases.

Fora Financial offers some of the lowest-cost merchant cash advance out there, with factor rates starting as low as 1.1. It also offers an early payoff discount and doesn't charge a monthly maintenance fee. Businesses that have been around for as little as six months can qualify as long as they have $5,000 in monthly credit card sales and no open bankruptcies. But it doesn't display rates online, and it can take as long as 72 hours to receive your funds.

Loan amount

$5,000 – $1,500,000

APR

Undisclosed

Min. Credit Score

570

Fora Financial offers some of the lowest-cost merchant cash advance out there, with factor rates starting as low as 1.1. It also offers an early payoff discount and doesn't charge a monthly maintenance fee. Businesses that have been around for as little as six months can qualify as long as they have $5,000 in monthly credit card sales and no open bankruptcies. But it doesn't display rates online, and it can take as long as 72 hours to receive your funds.

Pros

Low cost for a merchant cash advance

Only six months in business required

Discount for early payments

Cons

More expensive than most working capital loans

Potential 72-hour turnaround

Loan amount

$5,000 – $1,500,000

APR

Undisclosed

Min. Credit Score

570

Loan term

4 to 18 months

Requirements

6+ months in business, $25,000+ gross monthly sales, no open bankruptcies

Invoice financing and factoring offer an advance on unpaid invoices for business-facing businesses (B2B). Invoice financing allows you to retain control of your accounts receivable as your customers pay them off, and is usually available for smaller amounts — say under $30,000 or $50,000. Invoice factoring involves selling unpaid invoices to a third party at a discount.

This type of business funding doesn’t rely on your credit score or time in business. But, like a merchant cash advance, it’s one of the most expensive financing options available and should be saved as a last resort.

Lendio is an online marketplace that can help your business prequalify with multiple factoring companies, including TBS Construction Funding and Raistone Capital. You can receive up to 90% of your accounts receivable in as little as 24 hours. Factor rates start at 2%, and you have as long as a year to pay back the advance. But because it's not a direct lender, it's worth reading up on the companies you're connected with before you go through with the application.

Loan amount

$1,000 – $5,000,000

APR

Varies by lender

Min. Credit Score

580

Lendio is an online marketplace that can help your business prequalify with multiple factoring companies, including TBS Construction Funding and Raistone Capital. You can receive up to 90% of your accounts receivable in as little as 24 hours. Factor rates start at 2%, and you have as long as a year to pay back the advance. But because it's not a direct lender, it's worth reading up on the companies you're connected with before you go through with the application.

Pros

Compare multiple offers from factoring companies

Get funded in as soon as 24 hours

Long term of up to 12 months

Cons

Not a direct lender

Doesn't disclose requirements for factoring

Loan amount

$1,000 – $5,000,000

APR

Varies by lender

Min. Credit Score

580

Loan term

3 months to 25 years

Requirements

Operate business in US for 6 months or more, have a business bank account, minimum 580 personal credit score, at least $8,000 in monthly revenue.

Microloans are are short-term loans from nonprofit lenders. Unlike most financial institutions, microlenders often offer financing to entrepreneurs who need working capital to start a new business. These often don’t require collateral or come with strict credit score minimums.

Usually you can borrow up to $50,000 with terms from six to 12 months. But these can take weeks to fund and rates often start a little higher than an online or bank loan.

Kiva is a nonprofit that offers crowdfunded microloans of up to $15,000 with a 0% APR. There are no credit or time in business requirements. But to qualify, your business must raise funds from at least five members of your social network over 15 days. After that, most small businesses can receive your funds within 30 days. The long turnaround may be worth the 0% APR in some cases.

Loan amount

$1,000 – $15,000

APR

0%

Kiva is a nonprofit that offers crowdfunded microloans of up to $15,000 with a 0% APR. There are no credit or time in business requirements. But to qualify, your business must raise funds from at least five members of your social network over 15 days. After that, most small businesses can receive your funds within 30 days. The long turnaround may be worth the 0% APR in some cases.

Pros

No interest or fees

Loans as small as $1,000

Cons

Can take up to 45 days

Relies on social network

No customer service line

Loan amount

$1,000 – $15,000

APR

0%

Loan term

6 months to 3 years

Requirements

Have at least ten friends and family members willing to contribute to your loan, live in the US, ages 18+, not in bankruptcy or foreclosure, not under any liens, not engaged in: multi-level marketing, direct sales, pure financial investing or illegal activities

You can use the funds from a working capital loan for almost any operational costs. Small businesses often use this type of business financing to pay bills, pay employees or refinance debt.

Many also use a working capital loan to take advantage of a new business opportunity or prepare for a seasonal increase in sales. For example, businesses often need extra working capital to pay for hiring expenses, inventory and advertising.

How to qualify

Your small business generally needs to meet the following requirements to qualify for a working capital loan.

At least 12 months in business

Annual revenue of $100,000 or higher

Good credit score of at least 670

Business bank account

You don’t necessarily need to meet all of these requirements to qualify. In fact, there are business financing options for every type of business — including startups and small business owners with bad credit. But you’ll have more of a selection to choose from if you meet these requirements.

Bottom line

A working capital loan can give your business funding to cover operating expenses or grow when your current assets aren’t enough. And there are a variety of business funding options for startups, established firms and all credit types.

But consider another type of business loan if you want to invest in a long-term project or make a large purchase. Compare more options with our guide to the best business loans of 2026.

Anna Serio was a lead editor at Finder, specializing in consumer and business financing. A trusted lending expert and former certified commercial loan officer, Anna's written and edited more than 1,000 articles on Finder to help Americans strengthen their financial literacy. Her expertise and analysis on personal, student, business and car loans has been featured in publications like Business Insider, CNBC and Nasdaq, and has appeared on NBC and KADN. Anna holds an MA in Middle Eastern studies from the American University of Beirut and a BA in Creative Writing from Macaulay Honors College at Hunter College, CUNY.

See full bio

Anna's expertise

Anna

has written

142

Finder guides across topics including:

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.