Each year, approximately 12 million Americans take out payday loans. What they need the money for might not be what you’d expect.

How many Americans are taking out payday loans?

You’ve probably seen a payday loan storefront or online ad for quick cash loans at some point in your life. Whether you’ve ever considered taking out a payday loan or not, you may be familiar with the concept of short term lending. These loans are typically used by people with lower incomes and are usually marketed by lenders as a remedy for unexpected financial emergencies.

What you may not know is that most people who use payday loans end up taking out more than one over the course of the year — and what they need the money for might not be what you’d expect.

What exactly are payday loans?

A payday loan is an alternative form of credit that can be accessed quickly and taken out by those with bad credit or on lower incomes. Because they can be accessed by those in need of urgent funds, or by those who wouldn’t be eligible for traditional loans, payday loans typically have a higher annual percentage rate (APR) than you’ll find for other personal loans or credit cards.

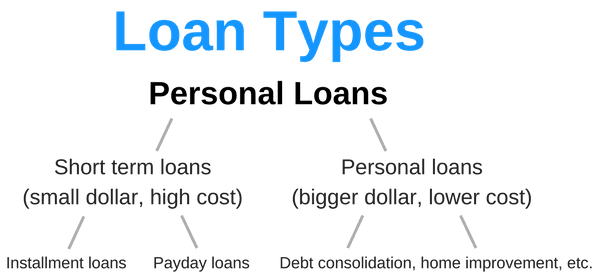

Payday loans are a form of short term lending. These small dollar, high cost loans are usually between $50 to $1,000. Here’s a diagram that quickly illustrates the different types of personal loans:

Who uses payday loans?

Approximately 12 million Americans use payday loans each year. View the diagram below to see payday loan usage by demographics.

People ages 25 to 49 are more likely to use payday loans compared to other age groups. Senior citizens ages 70 and older are least likely to use payday loans.

Education

No four-year college degree

Those who haven’t completed a four-year college education are more likely to take out payday loans. Beyond that, there isn’t much difference based on level of education.

Race

African American

African Americans are twice as likely to take out a payday loan than people of other races/ethnicities

Income

$15,000 – $25,000

Those with household incomes less than $40,000/year are almost three times more likely to take out a payday loan than those with higher incomes. People in households making between $15,000 and $25,000/year are the most likely to take out a payday loan.

Real Estate

Renter

Renters are more than twice more likely to use payday loans than homeowners.

Workplace

Disabled

Those who are disabled or unemployed are more likely to use payday loans than those who are employed.

Familial status

Parent

Parents are more likely to use payday loans than those without children.

Marital status

Separated or divorced.

Those who are separated or divorced are twice as likely to use payday loans than people of any other marital status.

What expenses do people take out payday loans for?

Surprisingly, the vast majority (69%) of people who take out payday loans use the money to cover recurring expenses such as credit card bills, rent and food. This demonstrates that most people who take out payday loans have an ongoing shortage of cash and a constant need for more income.

Although many payday loan lenders market their loans as a quick fix for unexpected emergencies, only 16% of payday loan borrowers use the money for that purpose.

The majority (73%) of payday loan borrowers visit a storefront to get payday loans. Those in southern states are more likely to take out payday loans than those in other geographic areas within the US. People residing in the northeast are least likely to take out payday loans. Drilling down to cities, those living in urban cities are most likely to take out payday loans.

Payday loan regulations by state

What are some alternatives to payday loans?

When experiencing a financial hardship, it may seem difficult to see other options that are available to help get out of the situation. Here are some payday loan alternatives, including other ways to borrow and ideas besides borrowing:

Aliyyah Camp is a SEO content strategist and former publisher at Finder, specializing in consumer and business lending. Her writing and analysis has been featured in CentSai, the Dough Roller and the Chicago Tribune. She holds a BA in communication from the University of Pennsylvania.

See full bio

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.