Clear-cut explanations on how balance transfers can help you manage debt.

These diagrams are for all the visual learners out there — those in debt who want to know why it’s so hard to pay off your credit card balances.

We show you how much you’re throwing away in fees, and how a balance transfer credit card might reduce the cost of getting you out of debt faster.

THE SETUP

In the following nine diagrams, let’s use the same scenario for more concrete results.

First, let’s imagine you’re making monthly payments of $100 on a credit card with:

$5,000 balance

17.99% APR

No annual fee

We found that $100 is about the minimum to pay to avoid racking up fees.

Consider a situation where you get an offer for a balance transfer credit card offering:

0% APR on balance transfers for 12 months

3% balance transfer fee

No annual fee

We’ll walk you through how this situation could help you pay off debt and save you money.

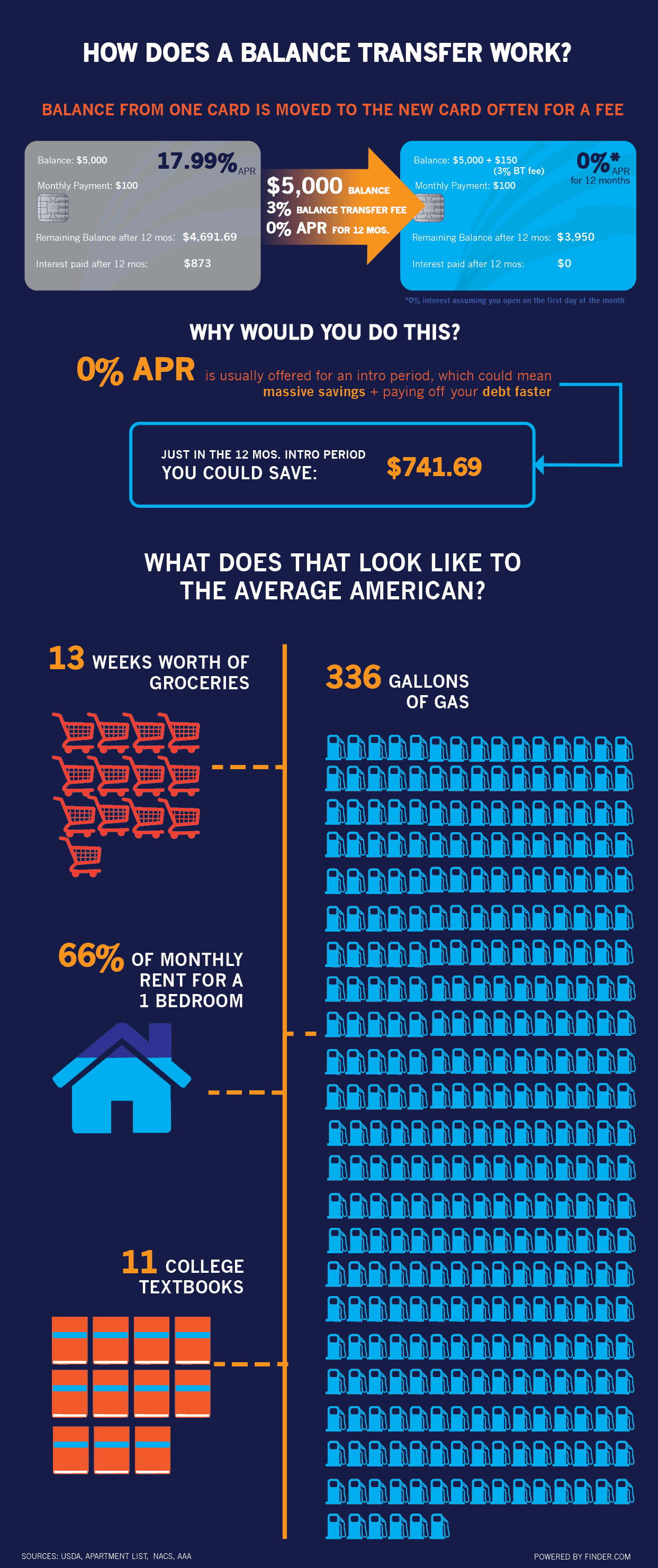

1. How a balance transfer credit card works.

A balance transfer credit card allows you to transfer other debt — credit cards or loans — onto a card with better terms. By transferring debt, you can take advantage of a new card’s lower APR — or even a 0% APR during an introductory period.

Even after you’ve factored in a card’s balance transfer fee, you could stand to save hundreds or thousands of dollars by dodging double-digit APRs found with most credit cards.

In our first diagram, we show you what would happen if you paid the same $100 monthly in our scenario above, but on a stronger balance transfer credit card instead.

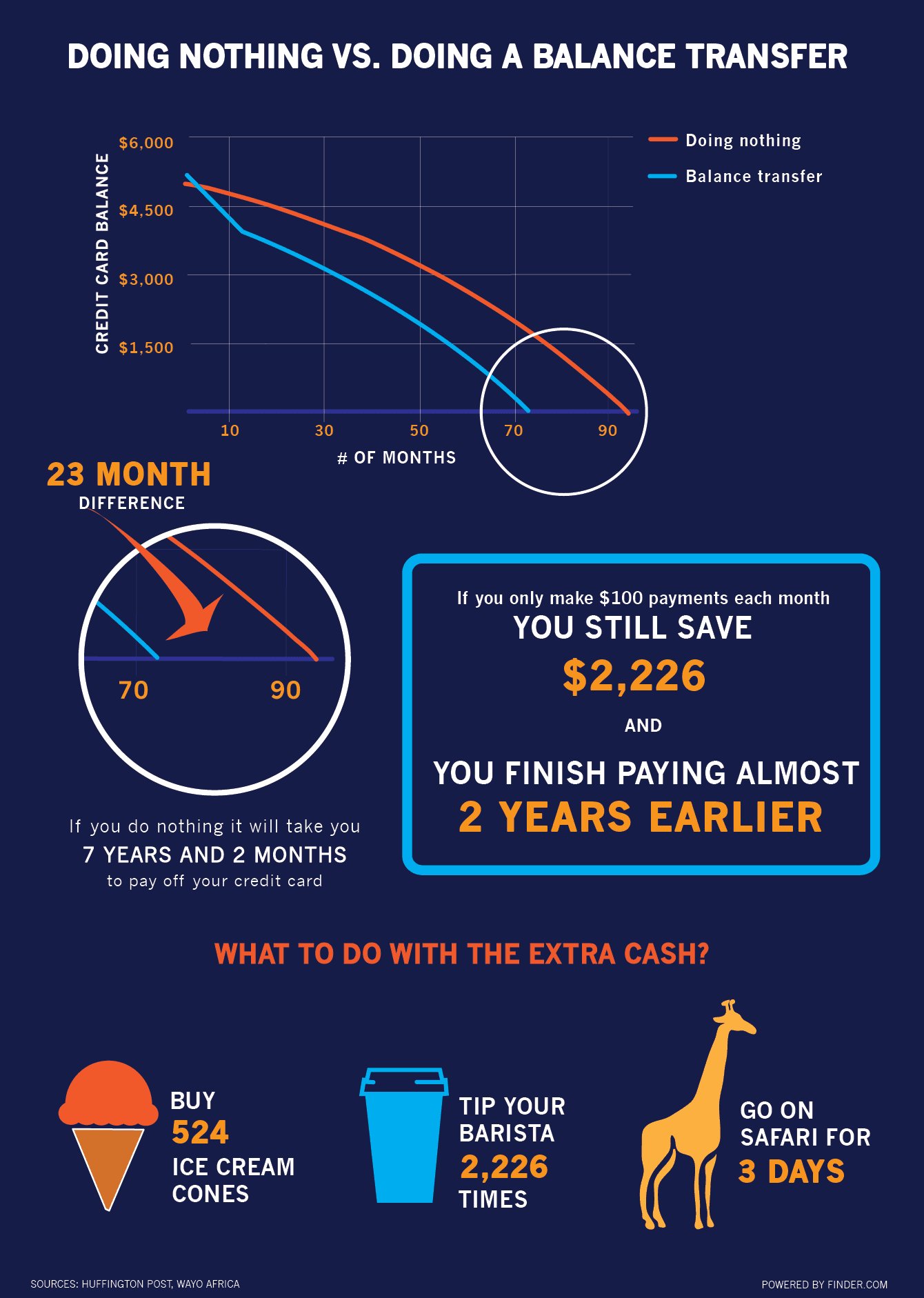

2. What’s the cost of doing nothing?

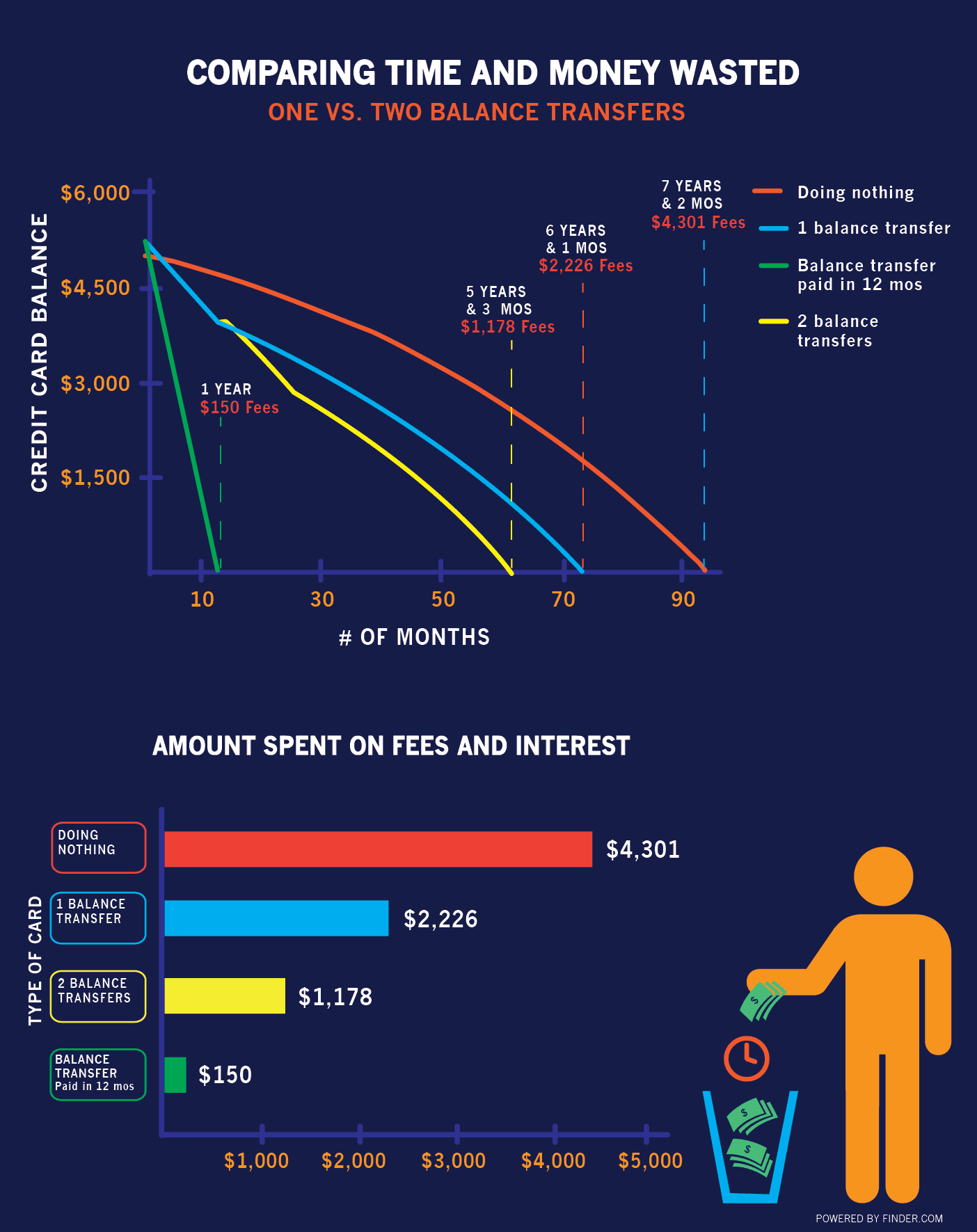

About $4,302 over some seven years.

In the first year of responsible spending on your new balance transfer card, you stand to save $741.69 by taking advantage of its 0% intro period. And if you hadn’t transferred your balance? Paying only $100 a month toward your debt, it’d take you seven years and two months to pay it off, further accruing $4,302 in interest.

Assuming that after the intro rate, your new card reverts to the same APR as your old card, you could save $2,076 and fully pay it off 21 months earlier — simply by maintaining your $100 monthly payments.

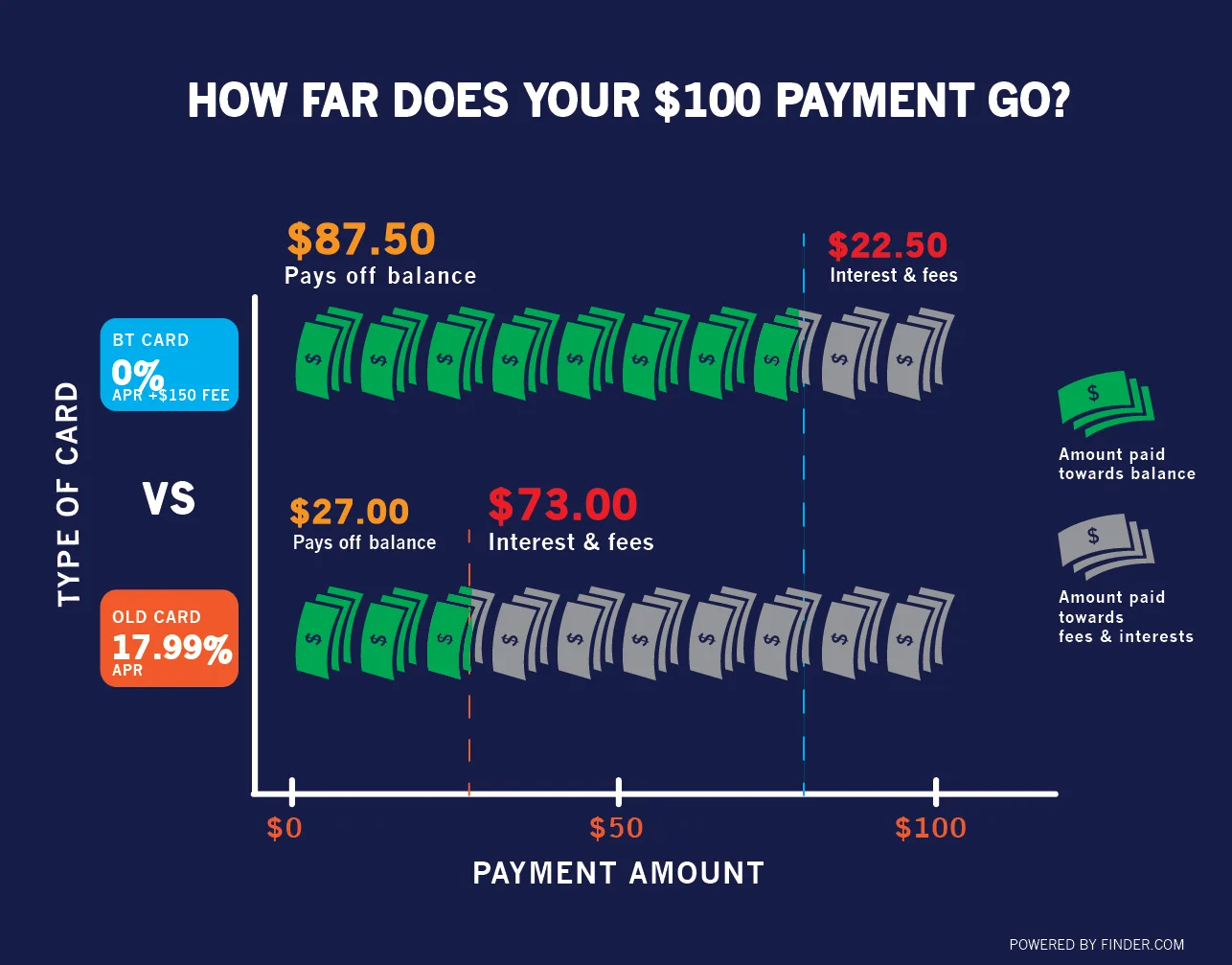

3. Don’t waste your monthly payments on interest.

It may surprise you that almost 73% of your $100 monthly payment is your APR. That means only 27% of your payment each month chips away at your debt balance.

Making only your minimum payment monthly is not recommended because every swiped you’ve made costs you more than your purchase, that only increases as time goes by.

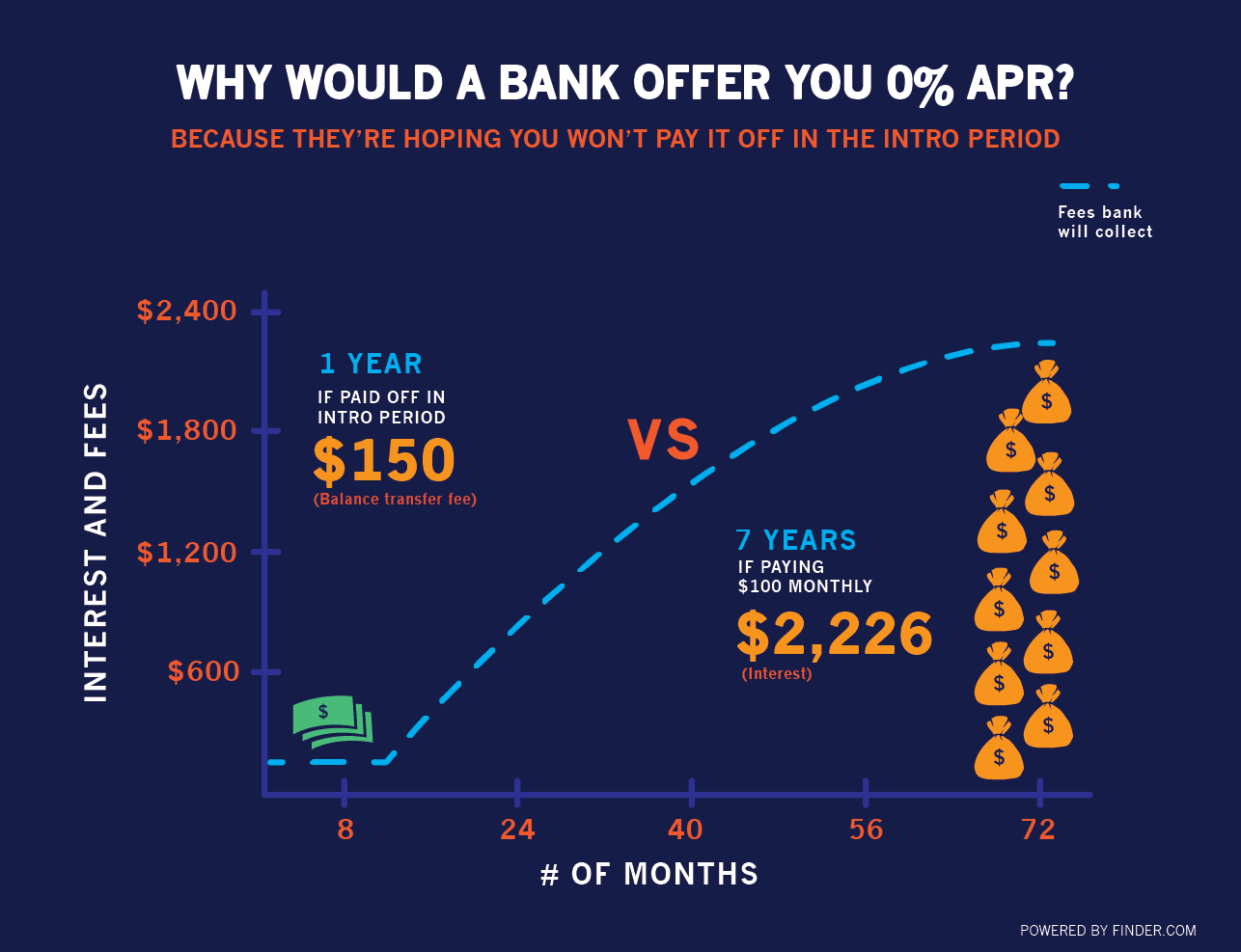

4. How do banks make money on a balance transfer credit card?

When an issuer extends a balance transfer credit card offer, it’s hoping you won’t pay off your balance in the intro period. Worse, it hopes you’ll keep spending and accrue high interest on those purchases.

If you continued making $100 payments after the introductory rate expires, you’d spend $2,076 on interest alone. That’s on top of $150 in balance transfer fees. A potential $2,226 is good enough reason for a bank to offer 0% APR for the first year.

5. Should you get a second balance transfer card?

If you can’t pay off your debt on your balance transfer credit card within the intro period, you might be tempted to take out another. You typically can’t carry two cards with the same issuer, but another bank might be interested in your business.

Below we compare how much you can save by paying off your balance transfer with one card compared with using two cards to pay your balance — and the cost of doing nothing.

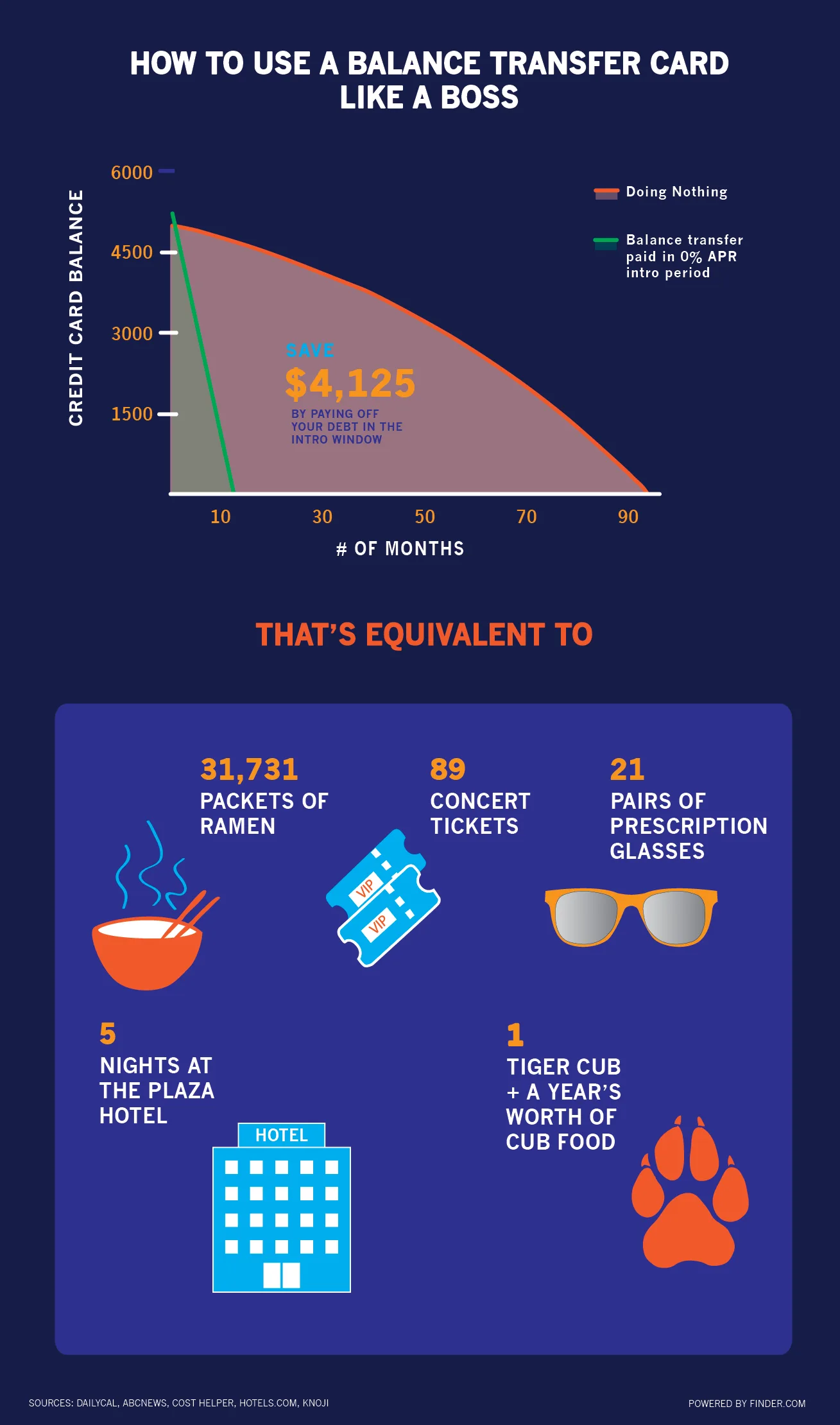

6. The most effective way to use your balance transfer credit card.

To take full advantage of a balance transfer credit card, commit to paying off your full balance within the card’s intro period.

Using our scenario, if you can swing $429.17 a month over the first 12 months, you could pocket $4,152 that’d be used to pay interest on your old card. That kind of cash is worth budgeting for, cutting costs to pay off your balance within the intro period.

Here’s what you could buy with the money that’s escaped you’ve avoided paying on a bank’s interest and fees.

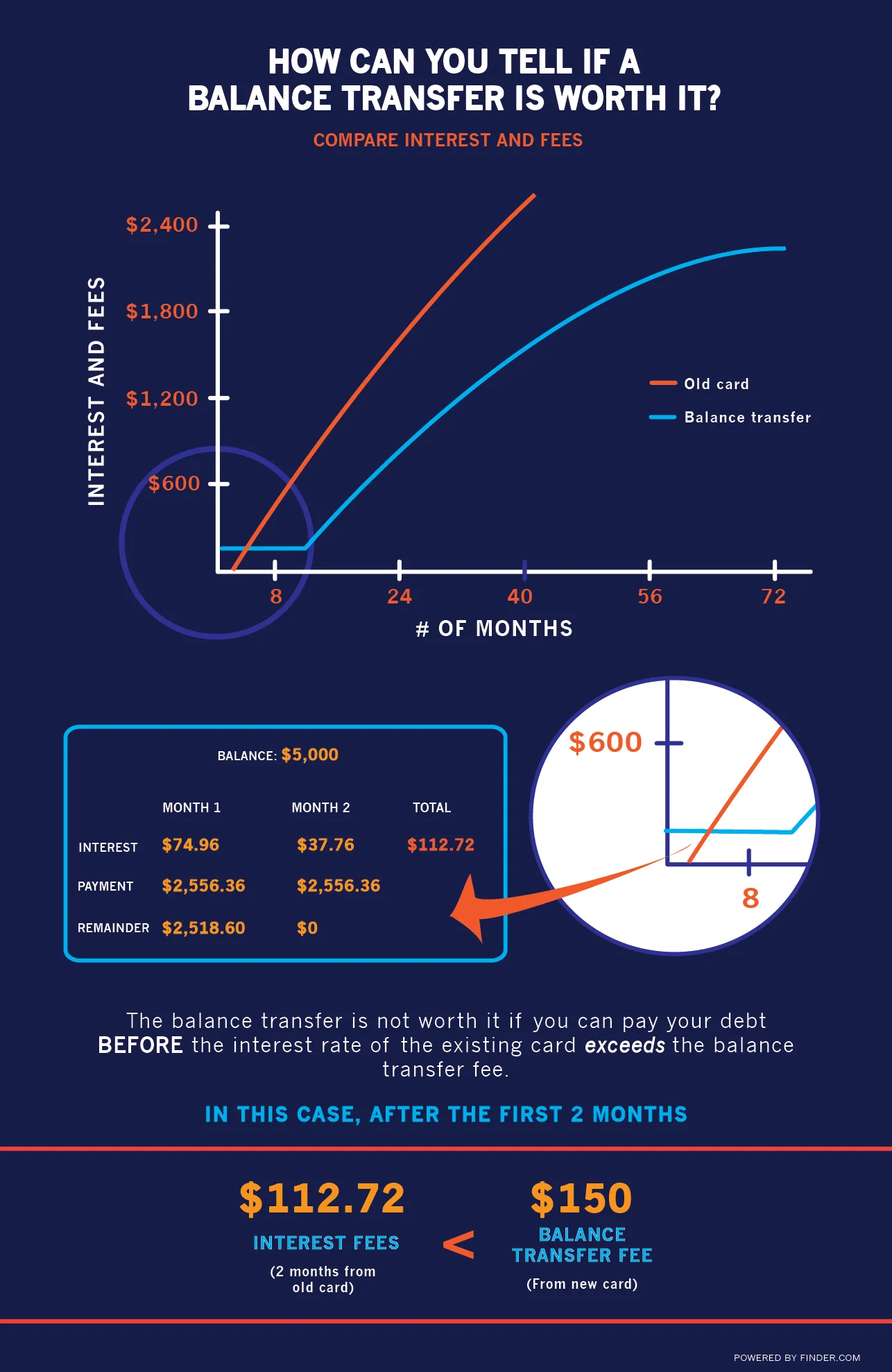

7. When shouldn’t you transfer a balance?

Compare the transfer fees against potential APR. If you can pay off your debt before your accrued interest exceeds the balance transfer fee, then focus on making payments to crush that balance.

We know that a $150 balance transfer fees isn’t chump change: It’s represents about two months in interest payments. So if you can afford to pay your debt in two months, a balance transfer may not be worth it.

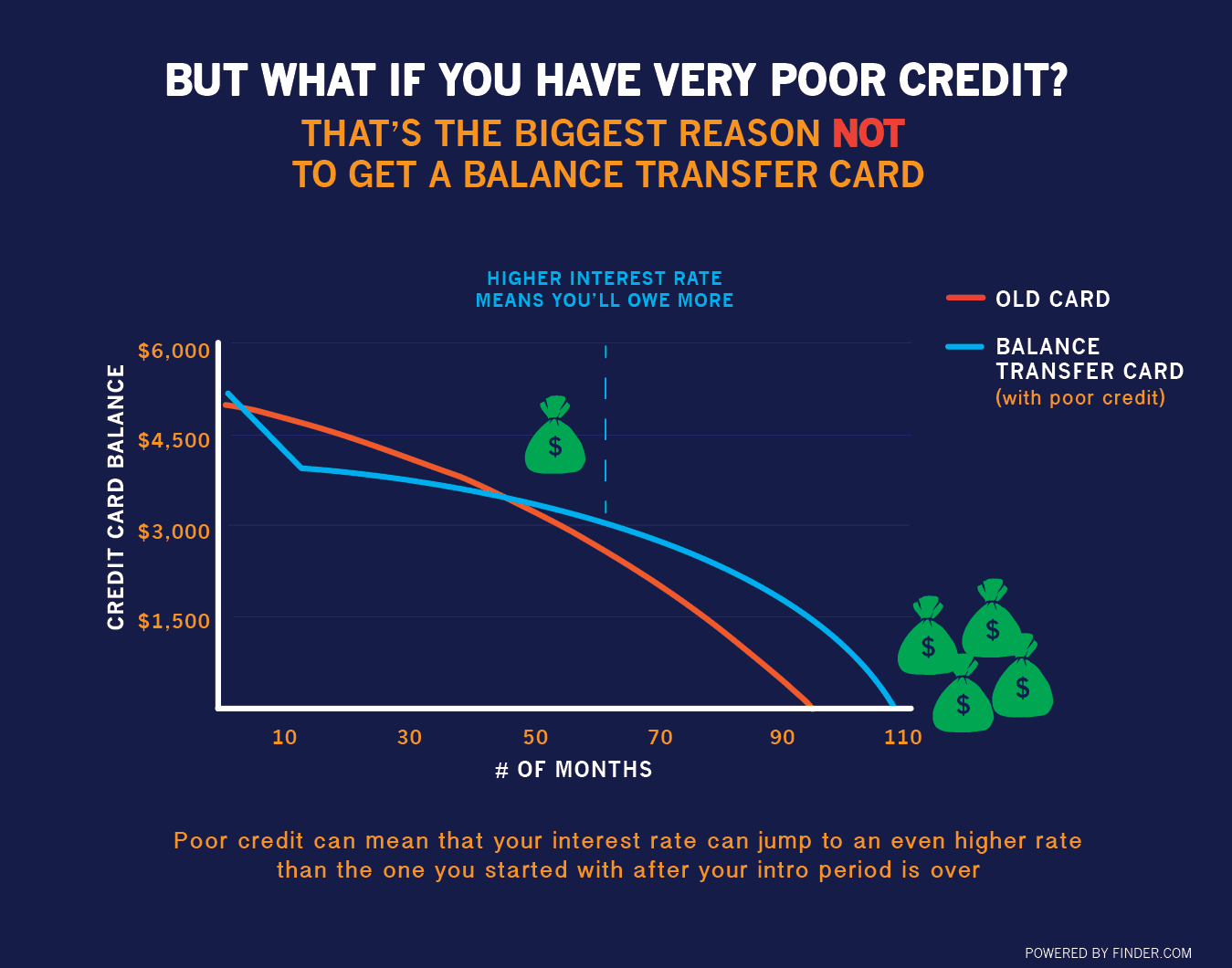

8. When should I avoid a transfer?

If you have poor credit, that could be a big reason to avoid a transfer. It’s more difficult for someone with poor credit to qualify for a credit card with low APR, good terms and minimal fees. If you know you can’t pay off your credit card debt within a new card’s intro period, you could wind up with a higher APR. Paying what you can could be your best bet to saving money. Not sure if you have poor credit? Read our comprehensive guide to understanding your credit score for tips on improving it.

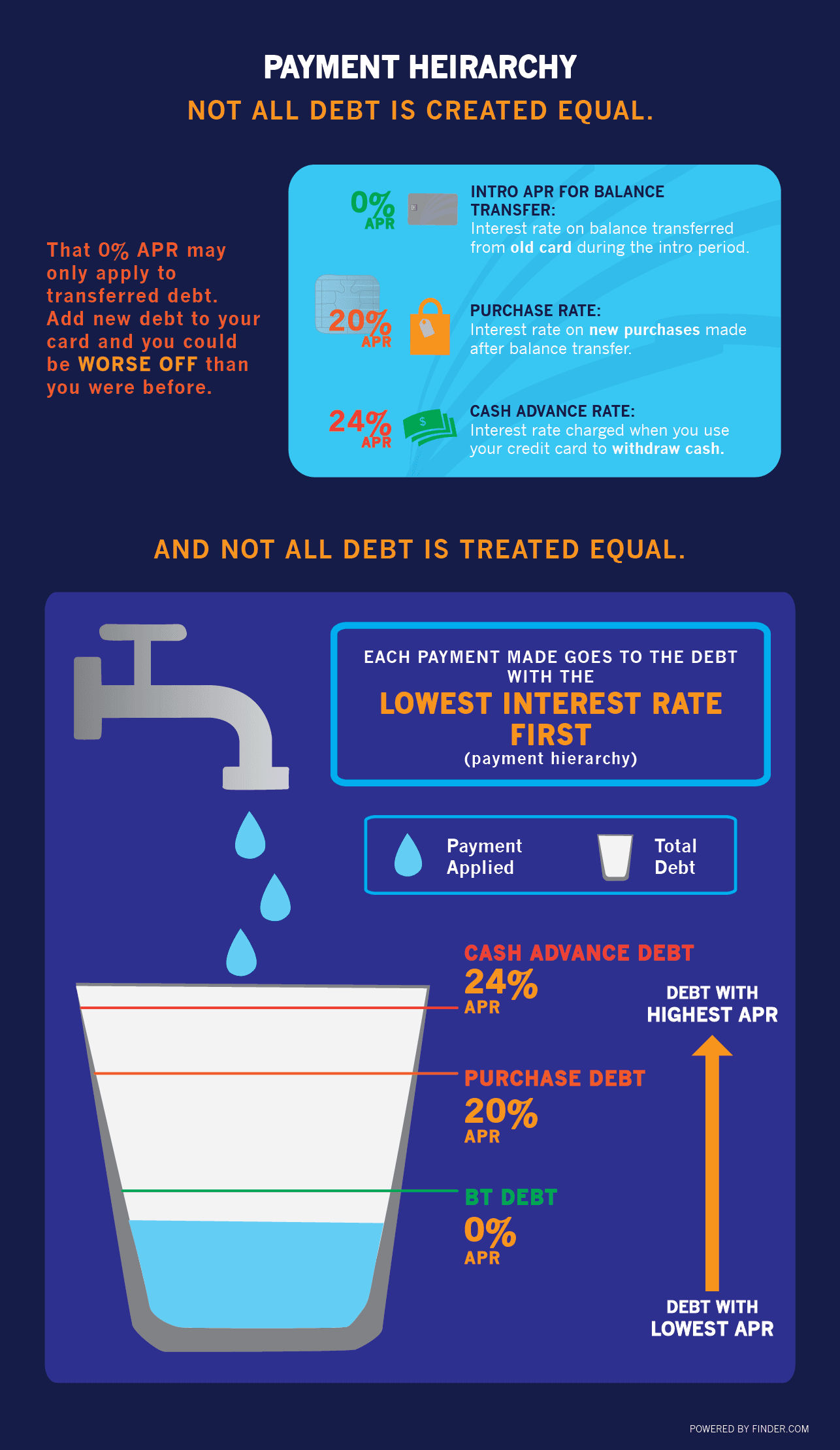

9. Payment hierarchy — or another potential drawback to balance transfers.

Clearly, the best way to take advantage of a balance transfer credit card is to pay off your full balance during the introductory period. But a low or 0% APR credit card might tempt you into racking up new purchases.

By paying with your new plastic, you risk not only paying off your credit card before the intro period expires, but also paying a higher APR on new purchases — part of a credit card’s fine print.

When you make a new purchase with your 0% balance transfer credit card, your monthly payments are applied to the balance with the lowest interest rate. Until you pay off the transfer balance, you’ll accrue the purchase interest rate on your new balance

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.