What’s the minimum income for a credit card in Canada?

Find out how much money you’ll have to make to qualify for a credit card in Canada.

Many credit card providers require you to earn a minimum annual income for a credit card. The minimum income requirement for basic credit cards typically sits above $12,000 while for premium credit cards you could be required to make as much as $100,000. Find out more about how much you’ll need to earn to get a credit card in Canada, and learn more about other alternatives you can explore if your annual income for a credit card isn’t high enough.

Minimum credit card income requirements are classified as the lowest net income you can make to qualify for a specific credit card. Minimum income requirements generally start at $12,000 a year (before tax). Basic cards tend to come with lower credit card income requirements while premium cards typically demand higher incomes. Requirements can apply to your personal or household income, depending on your marital status.

Credit card income requirements in Canada are often broken down into different earning brackets for personal and household income. These are outlined below along with several examples of credit cards that fall into each category.

Income threshold | Types of credit card | Sample credit cards |

|---|---|---|

$0 to $59,999 |

| |

$60,000 to $79,999 |

| |

$80,000 and above |

|

Get Paid Twice for Your Financial Moves

Finder Rewards adds a digital Visa gift card to your provider's existing welcome bonus when you switch through our platform.

There are two main reasons why credit card companies check your annual income for a credit card:

Credit card companies have minimum credit card income requirements in place to make sure you have enough money to repay your credit card. By checking your annual income for a credit card in advance, they can make sure you’re set up to be able to make your repayments on time. This protects them against losing money due to a high volume of accounts in default.

Credit card companies impose requirements on premium cards to reduce the interchange fees that merchants have to pay. Premium credit cards come with higher merchant fees than basic cards, which has caused many merchants to complain about the number of premium credit cards in circulation.

In 2010, the federal government introduced a voluntary code of conduct to protect merchants against rising credit card processing fees. Many credit card companies complied by placing more restrictions on premium card ownership to appease merchants and avoid mandatory regulation which might restrict them from charging higher rates altogether.

Finder data suggests that men aged 25-34 are most likely to be researching this topic.

| Response | Male (%) | Female (%) |

|---|---|---|

| 65+ | 2.09% | |

| 55-64 | 4.01% | 6.10% |

| 45-54 | 7.67% | 7.49% |

| 35-44 | 11.15% | 6.27% |

| 25-34 | 18.64% | 11.85% |

| 18-24 | 12.20% | 12.54% |

It seems to depend on the provider. Some customers indicate that they were able to get approved for a credit card without meeting the mandatory credit card income requirements. Others indicate that they had to send pay stubs and employment verification into their credit card provider in order to qualify.

Again, this boils down to how much risk a provider is willing to accept by issuing a credit card to you without knowing whether you have the income required to pay it back. It also depends on whether you apply for a basic or premium credit card, as providers will limit premium cards to abide by the voluntary code of conduct established to protect merchants from high fees.

Credit card providers usually include credit card income requirements on their websites or product pages, so you can double check before you apply for a particular credit card. Other lenders prefer not to outline minimum credit card income requirements, so you won’t see this information for every credit card you look at.

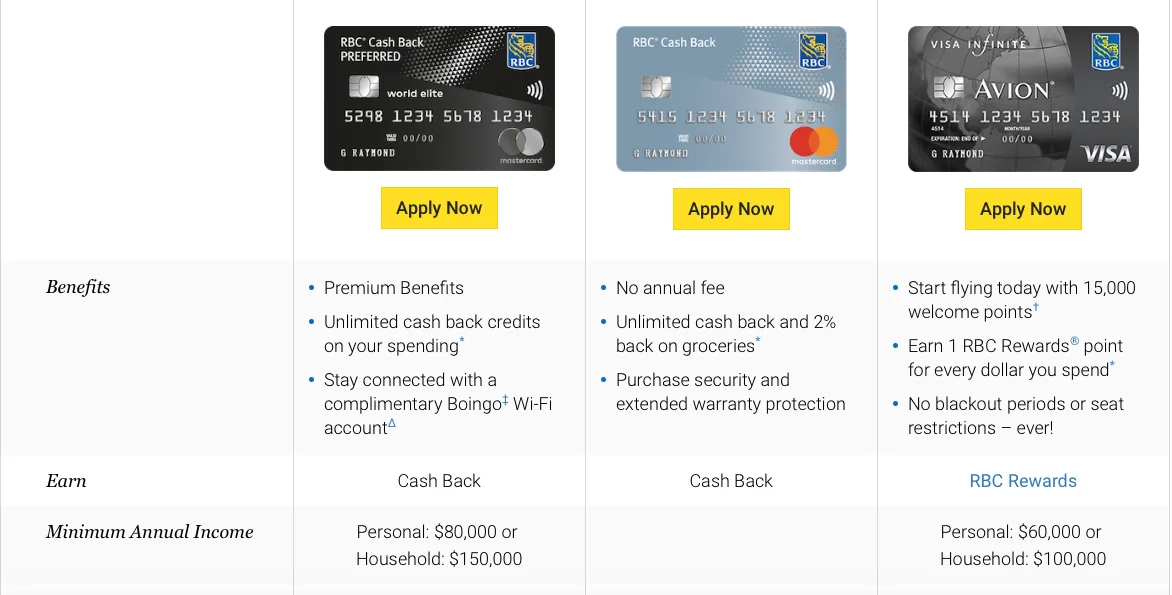

If you can’t find minimum credit card income requirements for a particular card, you can try calling the provider’s customer service department to ask about your eligibility. Here is an example of how the Royal Bank of Canada discloses the annual income requirements for its credit card products:

Picture: RBC Royal Bank

The main reason that credit card income requirements are much higher for premium cards than for basic cards is to minimize the processing fees that merchants have to pay. Premium cards come with much higher processing fees so credit card companies try to hand out fewer premium cards to make it fair for merchants.

Many credit card companies also impose higher credit card income requirements to make sure that they’re targeting big spenders with their premium cards. This helps to ensure that customers spend a decent amount of money on their card and can afford the annual fee that comes with most premium cards.

You may qualify for a credit card even if you’re between jobs or are currently relying on government assistance. Many credit card issuers will look at other sources of annual income for a credit card when deciding whether to approve you. These include the following:

Credit card issuers weigh a range of other factors before approving or denying your request for credit. These include the following:

The better your credit score is, the more likely you are to be approved for a credit card, even if you don’t meet the minimum income threshold. This is because it’s up to credit card companies to decide whether or not they want to accept you based on your credit alone.

You could also find it difficult to qualify for a credit card if you have bad credit or no credit at all. You’ll typically need to have a credit score of 650 or higher to be considered for a credit card and your eligibility will vary based on your provider.

You may be required to show proof of employment to qualify for some credit cards. In this case, you could show letters of reference from employers or pay stubs. If you can’t show an ongoing employment status, you may need to prove that you have enough money from other sources to make your repayments on time.

While credit card issuers typically prefer people to have full-time employment, you could still be eligible for some cards if you work part-time, are self-employed or if you have a pension or other steady source of income.

Each credit card issuer will have its own process to evaluate the risks involved in lending to you. Aside from checking your credit score, your provider may pull your credit report to find out more about your history of missed payments or bankruptcy. It may also do some detective work to figure out how much debt you have and what your assets are worth.

Many credit card companies will approve you based on assessing your overall financial health. For this reason, you should try to gather as much proof of your income and financial stability as possible before you apply for a credit card to make sure you have the necessary documents on hand to demonstrate your eligibility and overall credit worthiness.

If you’re struggling to get approved for a credit card due to not having a high enough income, you still have options.

Credit card income requirements are in place to make sure you’re in a position to make your repayments. They’re also used to limit how many premium credit cards get dispersed to reduce the transaction fees that merchants have to pay. Now that you have a better understanding of minimum income requirements, you can compare credit cards to see which one might be the best fit for you.

The Neo Secured Mastercard is a solid option for those with bad credit, but there are some drawbacks. Learn more in our review.

Shop with partners retailers to earn accelerated cashback with the Neo Mastercard.

Despite your credit history, it is possible to get a credit card without a credit check. Here’s how.

Transfer money from your credit card to your bank account but watch out for higher interest rates and fees.

Check out the best credit cards for fair credit, and learn how a fair credit score of 560-659 can impact your card options.

Do you travel, work or spend money in the US frequently? Find out if a US dollar credit card is the right fit for you.

Going abroad and wondering whether you can use your credit card while travelling? Here’s the lowdown on credit cards vs. cash, fees, and which cards to get.

Find out how old you have to be to get to get a credit card for teens in Canada, and learn how your child can qualify if they’re under 18.

Find out how you can apply for an instant approval credit card in Canada and get a response within 60 seconds.

Compare guaranteed approval credit cards for bad credit in Canada and learn how to qualify for a card.