Balance transfer credit cards can be an efficient way to free yourself from high interest rates and start consolidating and paying down your debt. Conducting a balance transfer is a simple process, but repaying your debt before the promotional offer runs out can be a daunting task. Here’s how you can conducted a balance transfer, plus a few tips to follow to ensure that your debt consolidation is a successful and smooth process.

Choose a balance transfer credit card

The goal is to compare the offers on the market and discover which one offers you the most value. Remember to consider the following things when looking for a balance transfer credit card:

Promotional APR length. The typical time frame for the intro 0% or low APR is 6-10 months, although there are some cards that offer up to 12 months, or sometimes more, with no interest. It’s best to try to pay off all or most of your debt during the promotional period.

Balance transfer fees. Keep in mind that most balance transfers come with a fee that is typically between 1% to 3% of the debt that you are transferring. Make sure to calculate this into the total price to see if a balance transfer would be worth it for you.

Annual fees. Some credit cards have annual fees. These annual fees typically range from $0-$99. Keep in mind that some companies may waive the annual fee but only for the first year. Take any annual fees into account when you’re trying to budget out your debt re-payment schedule.

Balance transfer limit. Some cards will only allow you to transfer a certain amount of money at a time. If you have a large balance, you may have to complete the transfer in separate transactions and you might end up paying more in fees.

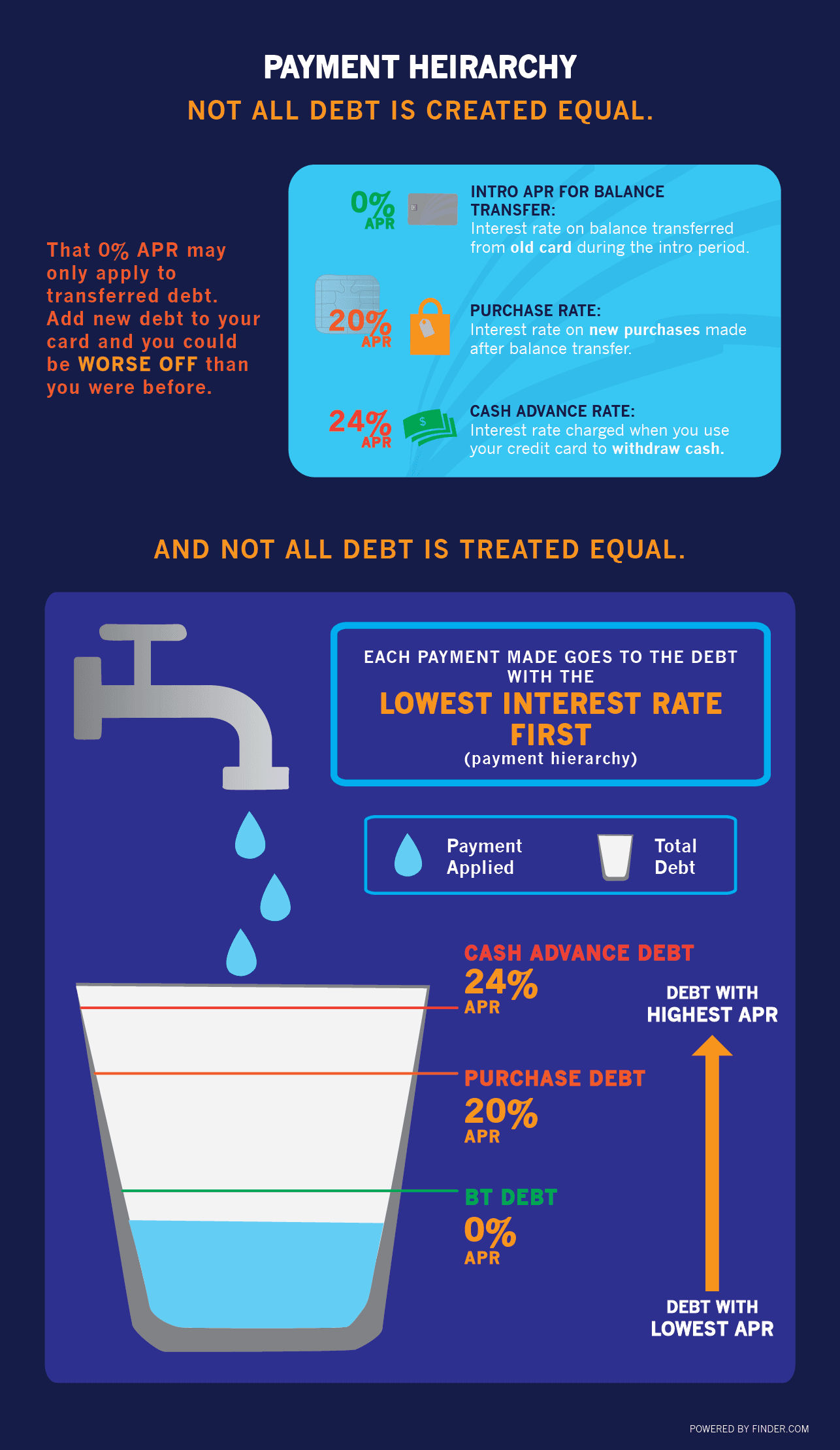

Rewards. Make sure to check if your card comes with any kind of rewards or benefits such as interest-free days, travel rewards or 0% APR on purchases.

Credit rating. Your credit rating will play a huge part in which balance transfer credit cards you will qualify for. If you have a fair or poor credit history, be sure to do your research to find a card with more lenient approval criteria.

Revert APR. If you are late or miss a payment, you may lose your promotional APR and be stuck paying the revert interest rate. To get the full benefits of your balance transfer card, it’s imperative that you make all of your payments on time.

Confirm how much you can transfer. You may only be able to transfer up to a percentage of the available credit limit, such as 80% or 90%. Confirm the total allowed transfer amount with the provider before you select the card.

Now that you’ve chosen the perfect balance transfer card, submit your application. Click “Go to site” in the table below to start your application. When filling out your application you’ll be given the opportunity to include the balance transfers you wish to make. You’ll need to provide the account number and the amount you wish to transfer. This is simply a request on your part. The exact amount you’ll be eligible to transfer will be determined once your application has been reviewed and approved.

If you’re approved, your new card provider will transfer the balances on your behalf, up to the credit limit on your new card minus any transfer or annual fees. Be sure to continue to make your minimum monthly payment on your old card until you’ve confirmed that the transfer has been made.

Make sure to complete the transfer as soon as possible.

If you wait longer than 60 days, you may lose the promotional APR. It typically takes 5-7 business days to be approved. If you haven’t heard back after this time, contact the bank to find out if there’s an issue. You may be asked to provide additional information. You can confirm your transfer once you’ve heard back.

Decide what to do with your old cards

Opening a balance transfer credit card doesn’t automatically close your old cards. While you may want to cancel your old cards, doing this may impact your credit score for the worse. Both your credit utilization rate and the age of your card can positively or negatively affect your credit rating.

Credit utilization rate. This is your debt-to-limit ratio. There are no hard and fast rules for how long you should try to keep your rate, but many money experts recommend that you should shoot for under 30% as a goal. If you have a $1,000 limit and a balance of $800, you have a rate of 80%. Your credit score may take a hit upon transferring one or several balances to your new card if it uses most or all of your limit.

Age of card. A credit bureau likes to see that you have had a long relationship with your credit card. The older your card, the better.

Annual fee. On the other hand, if your old cards have an annual fee and you don’t plan on using them any longer, you may want to consider closing them if you don’t want to keep paying the fee every year.

Tips for managing your debt with a balance transfer

Don’t use your balance transfer credit card for purchases. The sole purpose of getting a balance transfer is to consolidate your debt into one single location and focus on paying it off. Balance transfer credit cards often charge high interest on new purchases and depending on their terms and conditions. By using your card for purchases, your payments go towards your balance transfer debt while the balance for your purchases accrues interest.

Understand your interest-free days. Interest-free days are only active if you’re not carrying a balance at the end of the statement period, so you won’t be able to cut interest costs that way.

Emergency purchases. If you want a card for emergency purchases, you might want to consider applying for a different card with a low interest rate on purchases and do your best to keep the other card for consolidating only.

After the offer ends

If you’ve found yourself with remaining debt at the end of your promotional period, you might want to consider doing another balance transfer. However, if your credit history shows that you were unable to repay your debt during the promotional period, lenders may be less likely to approve your application. Applying for too many credit cards and receiving rejected applications can have a negative impact on your credit score, so it’s important to consider what outcomes using a second balance transfer as a back up will have.

Compare balance transfer credit cards

Looking for a balance transfer credit card? Compare options in the table below.

{"userFilters":[{"config":{"MULTISELECT":true,"VALUES":"Rewards, Cash Back, Low Interest, No Annual Fee, Balance Transfer"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.CARD_TYPE_FILTER"},"dataType":"TEXT","label":"Card Type","order":1},{"config":{"MULTISELECT":true,"VALUES":"Visa, Mastercard, American Express"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.CARD_BRAND_FILTER"},"dataType":"TEXT","label":"Card brand","order":2},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"GENERAL.PROVIDER_ID"},"dataType":"UUID","label":"Card Provider","order":3}],"niche":{"currencySymbol":"$","decimalPoint":".","decimalPlaces":"2","thousandsSeparator":",","filterBoundsMap":{"product.DETAILS.CARD_TYPE_FILTER":null,"product.DETAILS.CARD_BRAND_FILTER":null,"product.GENERAL.PROVIDER_ID":null}},"prefilled":false,"experimental":false}

7 of 14 results

Bottom line

Balance transfer credit cards can be a worthwhile consolidation tool, but only when used properly. Plan your strategy, make regular repayments and follow the above tips to ensure you get the most out of your balance transfer.

Adrienne Fuller is the former head of publishing at Finder US. With a decade of experience creating guides in finance and education, she aimed to deliver the accurate and transparent information she wished she had when she made some of life's important financial decisions. Adrienne has a BA from Colorado College and loves to hike with her two Catahoula dogs.

See full bio

Jaclyn Hurst was an associate publisher at Finder. She has a Bachelor’s degree in Business from Redeemer University and a University Certificate in Management Foundations from Athabasca University. She’s as passionate about business and finance as she is about the great Canadian outdoors, organic Sumatra coffee and music.

See full bio

Find out how to move your debt from a personal loan to a credit card.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.