A 401(k) can be a powerful retirement savings tool, but your plan may be downgraded by high fees and poor investment options. We’ll explain everything you need to know about 401(k)s and other retirement savings vehicles you may want to consider if yours is subpar.

What is a 401(k)?

A 401(k) is an employer-provided retirement savings and investing plan that offers tax benefits. Build your 401(k) portfolio by picking from an investment menu that usually includes stocks, bonds and mutual funds. To contribute to your 401(k), you set a percentage of your pay that you want to invest. Then, your employer automatically deducts that amount from each paycheck and invests it in your account.

Because your money flows from your check to your 401(k) before it’s taxed, it reduces your taxable income and can lower your tax bill each year. Some companies also match their employees’ contributions.

How is a 401(k) different from an IRA?

A 401(k) is similar to an individual retirement account (IRA). Anyone can open an IRA with a bank or brokerage, so you can opt for one if your company doesn’t offer a 401(k). But there are some key differences.

Enrollment

2025 contribution limits

Tax advantages

401(k)

Enrollment period and eligibility is set by the employer

Some automatically enroll eligible employees

$23,500

$31,000 if you’re 50 or older

Tax-deductible contributions

Investment earnings grow tax-free in your account

IRA

You can enroll whenever you want

$7,000

$8,000 if you’re 50 or older

Tax-deductible contributions

Investment earnings grow tax-free in your account

Because 401(k) plans vary widely because of employer choices, you may want to consider saving in an IRA in addition to or instead of a 401(k). You can compare retirement account options here.

How does a 401(k) grow?

Your 401(k) grows based on the performance of the assets it invests in. But it also benefits from compound interest. This means interest that your account earns one year is built upon by future earnings. With simple interest, your interest only builds on the initial deposit. So if you deposited $10,000 and you get an annual interest rate of 9%, it grows by $900 every year. After 30 years, it’ll be $12,700.

Now let’s see how $10,000 would grow in a 401(k). Let’s say your annual interest or rate of return is still 9%. After 30 years, your 401(k) balance would grow to $147,305. And that’s assuming you don’t contribute anything beyond that $10,000 balance.

Who manages a 401(k)?

A 401(k) is managed by a plan sponsor. This sponsor can be your company or a third-party benefits firm. Plan sponsors hire asset-management companies that handle investing matters.

Can I lose money in a 401(k)?

As with any investment, your 401(k) can lose money. The assets your 401(k) invests in may not perform well some years, thereby cutting your earnings.

But think of a 401(k) as a long-term savings vehicle. Over time, markets recover from recessions and even crashes. In fact, the average stock market return for the last 50 years has been 10.9%.

Nonetheless, diversifying your portfolio is one of the best ways to protect your 401(k) from market downturns. This means investing in a variety of securities like stocks, bonds, exchange-traded funds (ETFs) and mutual funds.

Many 401(k) plans offer target-date funds (TDFs). These professionally managed, diversified portfolios automatically shift their investment mix to safer assets, such as bonds and money market funds, as you get closer to retirement age. While not the perfect investment, TDFs can be great tools for those who would rather hand off investment decisions to the pros.

What does 401(k) stand for?

The 401(k) plan is named after a subsection in the Internal Revenue Code. It allows employers to create retirement savings plans to which employees can contribute portions of their wages before taxes. It also permits earnings on these contributions to grow tax-free until they’re withdrawn from the account.

Section 401(k) was added to the code in 1978. But the first 401(k) plan didn’t launch until 1981 when benefits consultant Ted Benna interpreted the code to create one for a client.

401(k) types

There are two main types of 401(k) plans offered by employers.

Eligibility

Contribution limits for 2025

Tax advantages

Traditional 401(k)

Determined by plan sponsor

$23,500

$31,000 if 50 or older

Tax-deductible contributions

Earnings grow tax-free in the plan

Withdrawals are taxed as part of ordinary income plus a 10% early withdrawal penalty if you’re under 59.5

Roth 401(k)

Determined by plan sponsor

$23,500

$31,000 if 50 or older

Contributions can be withdrawn any time regardless of age

Earnings grow tax-free in the plan

Withdrawals are tax-free if you’re 59.5 or older and the account has been open for at least five years

Note that the above limits apply to all types of 401(k) accounts, which fall under the umbrella of defined contribution (DC) plans. So if you have a traditional and a Roth 401(k), your contribution limit is $19,500 across both plans.

Also, the contribution limits listed above represent employee contributions, also known as elective deferrals. Some companies offer employer matches. The maximum contribution from you and your employer is $70,000.

However, the IRS states that contributions from all sources can’t exceed 100% of your compensation.

d41666c6-f9bf-4b8f-8a0e-9850e2f6067c-Comprehensive 401(k) search service

Comprehensive 401(k) search service

Find all your old 401(k)s and their hidden fees

Borrow from your Beagle 401(k) or IRA with 0% net interest

Robo-advisor available if you roll over your 401(k) to Beagle

Lifecycle of a 401(k)

To make the most out of your 401(k), it may be helpful to think of the lifecycle of the 401(k), from its inception through your retirement.

Opening a 401(k)

Some companies auto-enroll their employees in their 401(k) plan. So follow the instructions on your plan documents or ask your HR department for these. Otherwise, it’s a pretty straightforward process.

Check with your HR department to see if you’re eligible. You may be eligible even if you’re working part time, thanks to the SECURE Act passed in 2019.

If you’re eligible, ask your HR department about next steps. You may need to fill out some paperwork or set up an account online. Keep some information at hand.

Legal name

Current address

Personal email address

Social Security number

Bank account information plus routing number to fund your 401(k) electronically

Decide how much to contribute to your 401(k). Experts recommend 15% of your pay, but even starting with 3% and gradually increasing can help.

Choose investment options. Look out for fees like expense ratios if you’re choosing ETFs or mutual funds. These funds invest in a variety of assets like stocks and bonds, so they’re a good way to get diversified from the start.

Contributing to a 401(k)

Before you get your paycheck, your employer automatically deducts an amount of your choosing to direct to your 401(k) plan if you choose to contribute. It’s common practice to pick a dollar amount or a percentage of your pay.

How much of my salary can I contribute to my 401(k)?

Contribute the lesser of 100% of your salary or the applicable contribution limits set by the IRS each year. For 2025, the 401(k) contribution limits are $23,500 or $31,000 if you’re 50 or older.

How 401(k)s are taxed

The taxation of 401(k)s generally depends on the type of plan and the age at which you withdraw money.

Withdrawing from a 401(k)

Withdrawing from your 401(k) often comes with complex rules, and doing so without incurring heavy penalties requires meeting certain age requirements.

Withdrawing from a traditional 401(k)

After 59.5: Withdrawals are considered part of your income, so these will be taxed at your federal tax-bracket rate. Some states will also tax your withdrawals. After age 73, you must take required minimum distributions (RMDs) based on the IRS Uniform Lifetime Table.

Before 59.5: Your withdrawals will be taxed as ordinary income plus a 10% early withdrawal penalty. The IRS also takes an automatic 20% early withdrawal withholding.

Withdrawing from a Roth 401(k)

After 59.5: You can withdraw contributions and earnings tax-free. You must take required minimum distributions (RMDs) from a Roth 401(k) when you reach age 73.

Before 59.5: You can withdraw your contributions tax-free. But earnings will be taxed as ordinary income plus a 10% tax penalty.

The good news is that for some needs you can borrow money from your 401(k) and avoid penalties. Read the rules for 401(k) loans here.

Employer 401(k) contributions

Some companies offer employer matches. The rules for this vary across companies.

Full match: Your company may match 100% of your contributions up to 3% of your annual salary. So let’s say your annual salary is $40,000. Your employer would match your contributions dollar-for-dollar up to $1,200 (3% of $40,000).

Partial employer match: Your company may offer a 50% match on 401(k) contributions up to 6% of your annual salary. Let’s say your annual salary is $40,000. Your contributions eligible for matching would be $2,400. But because the company will match 50%, the most it can give is half of your contribution or $1,200.

4 alternatives to your employer’s 401(k)

If you find your 401(k) plan isn’t so hot, you have other options.

Traditional IRA

A traditional IRA is essentially a traditional 401(k) that’s not provided by an employer.

Key benefits:

More investment options

Lower fees in some cases

Option to shop around for the best IRA

Drawbacks:

No employer match

Much smaller contribution limits

Roth IRA

This works similarly to a Roth 401(k), but nearly anyone can open a Roth IRA through a bank or brokerage.

An HSA is a tax-advantaged savings and investing account designed to help you pay for medical expenses. But you can also use your HSA for retirement.

Key benefits:

Tax-deductible contributions

Money grows tax-free in the account

Withdrawals are tax-free for qualified medical expenses

Withdrawals for non-medical expenses are tax-free after age 65

Drawbacks:

You need a high-deductible health plan (HDHP) to open an HSA

Low contribution limits

Taxable brokerage account

This is your basic investing account.

Key benefits:

No contribution limits

Invest in virtually anything your brokerage offers

Drawbacks:

Earnings are taxed

Self-directed accounts can be difficult to manage for non-experienced investors

Withdrawing without penalty

Withdraw from your 401(k) without penalty if you’re 59.5 or older. Early withdrawal penalties on some hardship withdrawals may be waived if your plan allows these. The rules vary by plan. But you can usually waive the penalty if you need the money to cover the following.

Medical expenses exceeding 7.5% of your adjusted gross income (AGI).

Court-ordered payments to a divorced spouse, a child or a dependent.

You lose your job at the age of 55 or later.

You become disabled.

Triggering events for a 401(k) plan

Roll over a 401(k) when you experience a triggering event, also called a qualifying event. Your plan sponsor defines these events, but they’re usually the following.

Job termination: You were either discharged from your company or changed jobs.

Retirement age: You reached age 59.5.

Death: Your family or beneficiaries can receive the funds in either a lump sum or in installments, which could stagger the taxes on the withdrawals.

Disability: Your plan document would define disability.

4 options for triggering events

If a triggering event occurs in your life, you have several options.

Roll the assets into an IRA.

Pros

More investment options

Same tax benefits

Cons

May trigger a taxable event unless you do a direct trustee-to-trustee transfer

Depending on your plan’s vesting schedule, you may not keep all your employer matches

Leave the assets in the existing 401(k).

Pros

Your money stays in a tax-advantaged account

Account keeps benefiting from investment earnings

Cons

May face higher fees

You can’t contribute to the plan

Roll the assets into a new employer’s plan.

Pros

May find better investment options

Could see lower fees

Cons

The plan may not be as good as your previous one

It can be difficult to transfer funds out of the new plan unless you face a triggering event

Cash out.

Pros

You can do whatever you want with the cash

Tax burden may be low depending on your age and income

Cons

May trigger severe tax consequences

You lose the benefits of compound interest

You eradicate your nest egg unless you have retirement funds elsewhere

Compare retirement accounts

These companies offer IRAs or offer help managing retirement accounts.

7 of 7 results

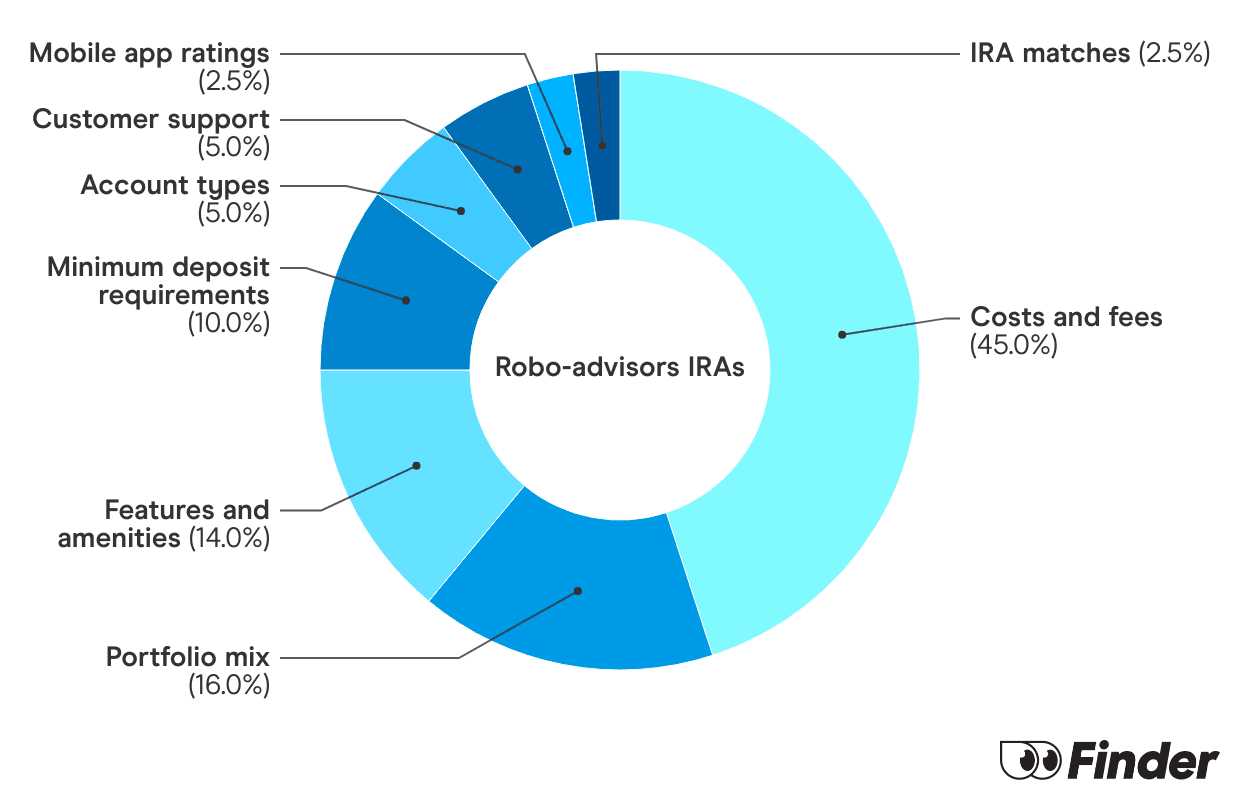

What is the Finder Score?

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Bottom line

401(k) plans allow you to invest in your retirement while enjoying tax breaks. Your contributions are tax-deductible, and investment earnings grow tax-free. Some companies even offer matching contributions. But the quality of 401(k) plans varies across companies. In some cases, an IRA may be a better option. You can open one with most brokerages, but compare your choices to find the one that’s right for you.

How does your retirement balance stack up to the average?

How much do you have for retirement?

Response

Contributions

Balance

Amount

$7,409.56

$196,192.48

Source: Finder survey by Qualtrics of 2,033 Americans

In 2023, the average American has an average of $196,192 in their 401K and plans to contributed an average of $7,410 in the last year.

Frequently asked questions

Yes. Some people contribute just enough to their 401(k) to get the full employer match, and the rest goes toward an IRA that may have better features.

No. The only income that funds your 401(k) is taken directly from your paycheck.

Nothing. 401(k) plans are protected from creditors. But withdrawing money from these accounts triggers taxes and penalties if you’re under the age of 59.5. So it’s usually not a great idea to tap into your 401(k) to pay debt.

Javier Simon is a freelance finance writer at Finder and a certified educator in personal finance (CEPF).

He’s featured on NerdWallet, Bankrate, Yahoo Finance and Fox Business, where he’s shared his expertise on personal finance topics, such as investing, retirement planning, taxes, budgeting and savings.

He has also covered breaking news, such as student loan forgiveness initiatives, the housing market and inflation’s impact on consumers’ wallets.

His passion is turning complex financial concepts into actionable content that can help people improve their financial lives.

Javier holds a bachelor’s degree in multimedia journalism from SUNY Plattsburgh.

See full bio

Here’s how retirement savings accounts work and how to compare your options.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.