Please note: You should always refer to your loan agreement for exact repayment amounts as they may vary from our results.

Late repayments can cause you serious money problems. See our debt help guides.

If you’re strapped for cash or have an unexpected expense that needs taking care of then a personal loan might be the right option for you. A personal loan can help you deal with costs that are above and beyond your savings, from repairing a car to financing your wedding. Our page will help guide you through the process of applying for a personal loan.

Jump to the step-by-step walkthrough

Before you start on the application process, confirm what type of loan you need. Personal loans are generally fixed-term, fixed-rate, unsecured products. They use your credit history to reduce risk, rather than using an asset like your house or car as collateral. If you need a larger loan or an ongoing, flexible source of credit, for example, then you may want to consider other financing options like secured loans or credit cards.

The amount you borrow will normally be based on the expense you’re trying to cover, and the duration of the loan will normally be based on how much you can afford to pay back each month. It’s better to determine how much you can spend each month and borrow less than your maximum so you can avoid stretching yourself too thin. You should never borrow more than you can afford to repay.

Taking out a loan that’s too small can leave you with remaining financial needs, but if you take out a loan that’s too large, you’ll be stuck paying interest on a larger amount than necessary. This is why you should carefully calculate the debt you can handle and the amount of your purchase before you apply.

By comparing lenders you can ensure that you pay as little interest as possible, and can keep the loan as short as possible.

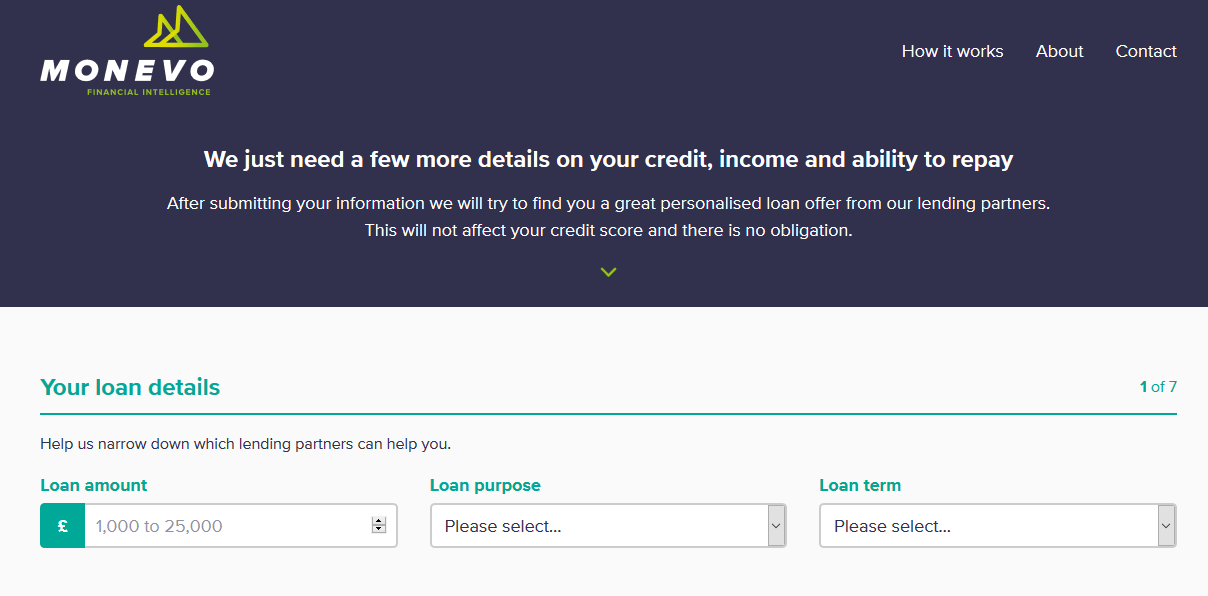

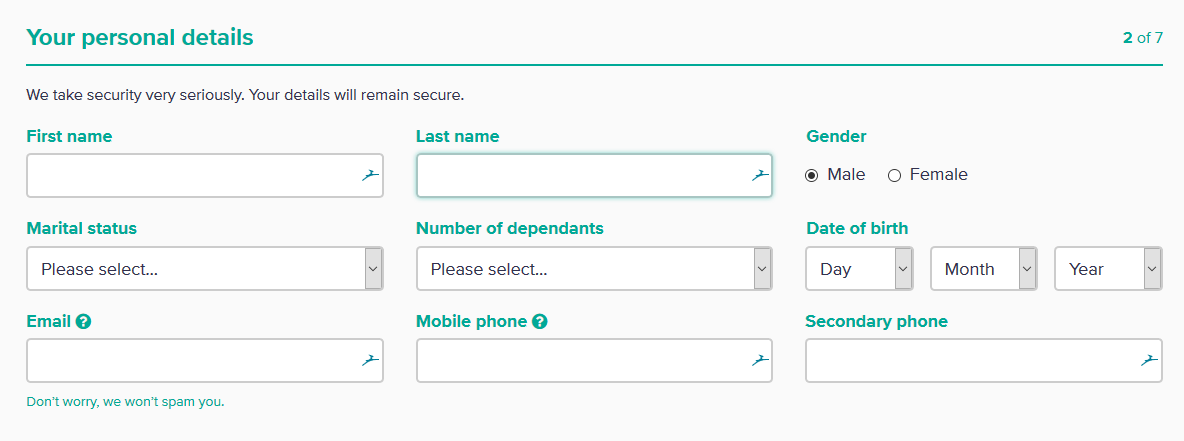

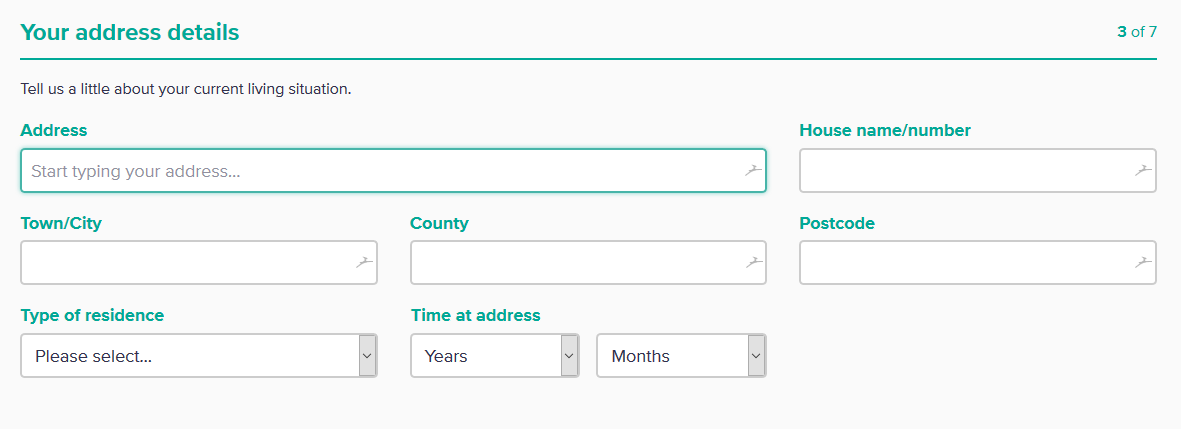

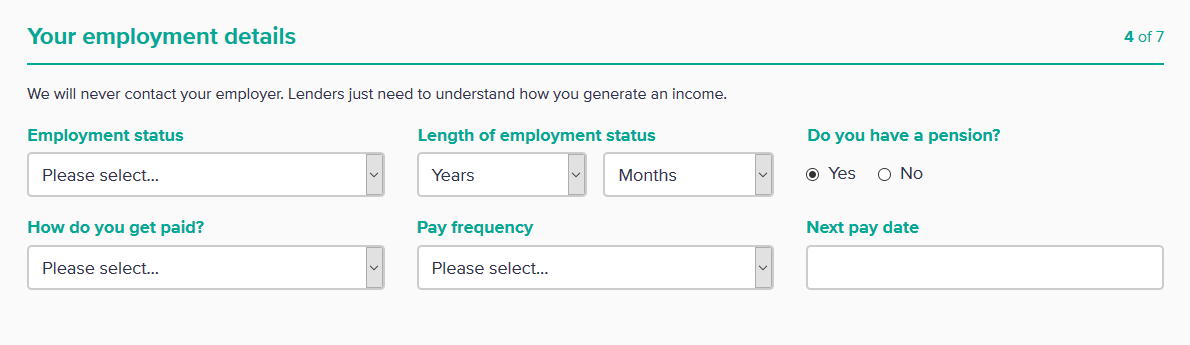

Most personal loan applications are fairly straightforward and take around 15-20 minutes. To make the process straightforward, and so that you don’t waste your own time, you should take a moment to considering the following points:

Each lender will list its own minimum criteria for applicants, and if you don’t meet these terms, you shouldn’t apply. Meeting these terms doesn’t guarantee approval, just that your application will be considered. While criteria can vary from lender to lender, below is a typical example:

The lenders that offer the best rates typically issue loans to the lowest-risk applicants, and risk is primarily assessed through a search of your credit file, which is held by credit reference agencies (CRAs). The three main CRAs in the UK are:

It’s free and easy to check your own credit score with any of the above. But even easier than this is using a soft search facility or eligibility checker provider by the lender that you have in mind. These give you a good idea of whether or not you’d be approved for a loan, without affecting your credit score.

In order to lend responsibly, lenders will require:

However when you apply for a personal loan online, most lenders can now electronically verify all of these through a credit reference agency CRA. In this case, you may need to answer some questions that only you would know the answer to, but you won’t have the hassle of having to dig out any ID, bank statements etc.

If you apply in a branch, you’ll need to prove your ID and address with separate, acceptable documents, and you may be asked to prove your income (generally through the last two months of payslips and/or bank statements, or if you’re self-employed, a HMRC document confirming your latest tax return calculation).

The application process may vary slightly from lender to lender, but generally they all follow a format similar to the one above.

Many lenders and banks require that you have a current account to receive your loan via a direct transfer, but that’s not always the only option. Some lenders will be able to send you a cheque or load your money onto a prepaid debit card. If this is important to you, ask your lender how they transfer funds.

It’s very important to make your payments on time so you don’t end up paying extra in fees or damaging your credit. Be sure to verify how you’ll make repayments. Can you pay by phone with a credit card or account number, online through the lender’s website or do you need to mail a cheque? Is there an automatic payment option? These will impact which lender you choose and how you’ll pay off your debt.

We currently don't have that product, but here are others to consider:

How we picked theseTo make it even easier to compare and evaluate unsecured loans we came up with the Finder Score. Speed, features and flexibility across 60+ lenders are all weighted and scaled to produce a score out of 10. The higher the score the better the lender – simple.

Read the full methodologyPlease note: You should always refer to your loan agreement for exact repayment amounts as they may vary from our results.

Late repayments can cause you serious money problems. See our debt help guides.

Find out whether a personal loan from Finio Loans could work for you.

Abound (formerly Fintern) is a UK lender that promises to offer borrowing “reinvented”, with affordable tailored loans.

Calculate the cost of an MBNA personal loan and see how much you can borrow today.

The super-popular UK challenger bank Monzo now offers flexible personal loans to existing users.

Borrow £5,000 to £25,000 with a competitive fixed rate personal loan from AIB. Find out how other lenders compare.

Find out more about Admiral unsecured personal loans of between £1,000 and £25,000. Get an instant decision and enjoy a fixed rate with no setup fees.

Novuna (formerly Hitachi) Personal Finance is not a bank – it’s a simplified, online finance provider from Japan that makes instant decisions on personal loans. Check out whether Novuna could be the yin to your financial yang.

See how to get a personal loan with the innovative lender Zopa, and get the latest Zopa loan rates, in our review.

Find out all you need to about personal loans from 118 118 Money. Fast simple comparison with a range of UK lenders.

Compare Halifax fixed-rate personal loans against products from a range of UK lenders. Apply online and secure a competitive rate.