Groundfloor review

- Minimum deposit

- $10

Summary

Nonaccredited investors can get started for just $10, but you risk borrowers defaulting on their loan.

Groundfloor connects investors with short-term, high-yield residential loans. For a small investment, investors of all levels can help fund a private house-flipping project. But investors only have access to residential real estate assets and you risk borrowers defaulting.

- Consider Groundfloor if you’re a nonaccredited investor seeking individual short-term real estate investments.

- Look elsewhere if you’re a passive investor seeking a REIT, RELP or REIG.

How does Groundfloor work?

Groundfloor is a real estate crowdfunding platform that offers investors the opportunity to finance house-flipping projects. Before a project goes live on the platform, Groundfloor vets the project and underwrites the loan. Once this process is complete, the project is added to the Groundfloor marketplace where investors get the opportunity to contribute.

Borrowers pay a fee to have their project put up on Groundfloor, but there are no platform fees for investors.

Here’s how the process works:

- Create an account. It’s free to sign up for a Groundfloor investor account and only takes a few minutes.

- Fund your account. You can invest as little as $10 to get started.

- Browse the marketplace. Explore Groundfloor’s marketplace to find projects that fit your investment goals.

- Invest. Decide how much you’d like to contribute to a project and transfer funds.

- Monitor. Monitor your investments through your Groundfloor dashboard with scheduled developer updates.

- Payback. Once the loan you’ve funded matures, withdraw your payback funds or reinvest in a new project.

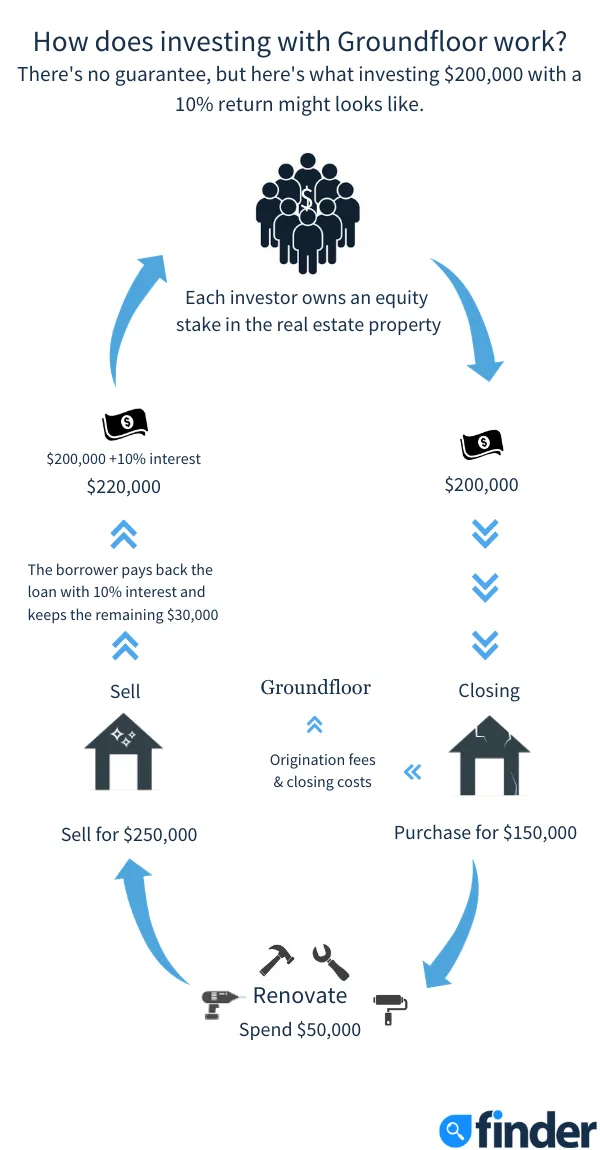

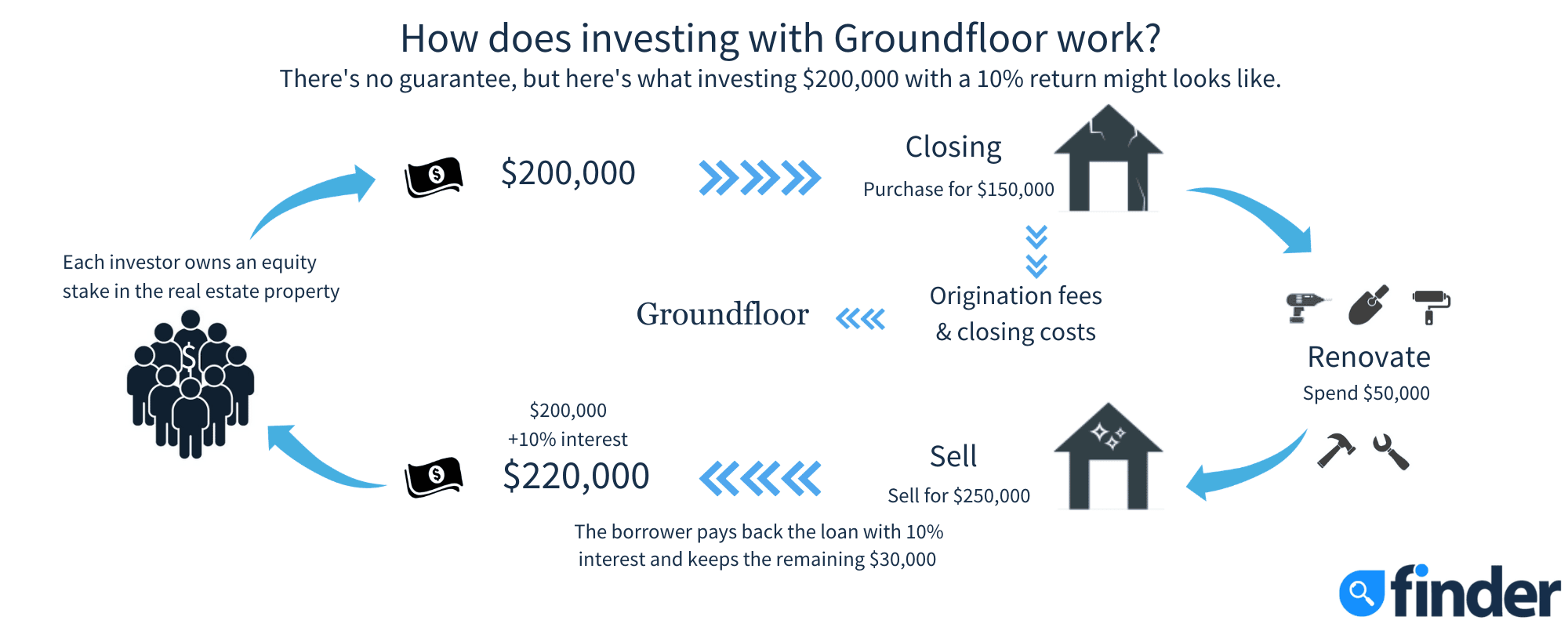

How does investing with Groundfloor work?

There’s no guarantee, but here’s what investing $200,000 with a 10% return might look like.

- Funding. Each investor owns an equity stake in the real estate property. Their money is pooled together to fund a $200,000 loan.

- Closing. The borrower purchases a house for $150,000. The origination fee and closing costs go to Groundfloor.

- Renovation. The borrower spends $50,000 renovating the home.

- Sale. The borrower sells the renovated home for $250,000. They pay back the $200,000 loan with 10% interest, which is $20,000 in interest, and keep the remaining $30,000 as profit.

- Return on investment. The $20,000 in interest is divided among the original investors based on how much they initially invested. Each investor receives 10% a return on investment.

Who is Groundfloor best for?

Groundfloor’s investment platform is ideal for:

- Nonaccredited investors. Groundfloor is one of the few real estate platforms available to nonaccredited investors.

- Active investors. Investors have full control over what, when and how much they invest through Groundfloor.

The platform makes real estate investing accessible with investment minimums as low as $10. Some loans pay interest monthly, while others pay all accrued interest once the project is complete. Most projects are completed in 12 months or less, so investors typically see a return within a year. Groundfloor states that most investments offer a 10% annual return.

New investors can ease into the world of real estate investments with Groundfloor’s $10 minimum. While active investors may like that they can control where and how funds are allocated.

Pricing and fees

Groundfloor’s platform fees are structured similarly to most other real estate investing platforms. Borrowers pay a platform fee to list projects, but investors can sign up for free.

What sets Groundfloor apart is its $10 investment minimum and six- to 12-month average holding period. Platforms like RealCrowd and CrowdStreet ask investors to lock in funds for years at a time with minimum investments starting at $25,000.

| Platform fee | $0 |

| Minimum investment | $10 |

| Average hold period | 6–12 months |

That said, platforms like RealCrowd and CrowdStreet offer access to a different type of investment: commercial real estate. These investments are limited to accredited investors and have high minimums for a reason — commercial properties are expensive to purchase and maintain.

Pros and cons

Pros

- Open to nonaccredited investors. Unlike many of its competitors, this provider opens up its investment opportunities to nonaccredited investors.

- Low minimum. No steep minimum investments here — get started with just $10.

- No platform fees. Investors can access Groundfloor’s platform for free.

- Short-term investments. Investors aren’t required to lock in funds for years at a time — most Groundfloor investments mature within 6 to 12 months.

Cons

- Potential loan defaults. While Groundfloor has the right to foreclose on a defaulted loan, the process can be time-consuming. Groundfloor investors say the process can take years before funds are released.

- Limited exposure. Groundfloor only offers access to a single asset class, so portfolio diversification options are limited.

- Limited support. Investor support is only available weekdays during business hours.

How Groundfloor loan defaults affect investors

When Groundfloor borrowers fail to adhere to one or more of the terms of their loan agreement, the loan goes into default. This can include a failure to keep current on insurance and tax agreements, failing to provide required project updates or falling behind on loan payments. If the borrower doesn’t correct the default within 30 days, Groundfloor has the right to foreclose on the loan.

Groundfloor states that even if a loan an investor has backed is in default, the loan is unlikely to experience a loss. And while investment disbursements may be delayed as a result of the default or foreclosure process, most Groundfloor loans are repaid in full. Investor reviews echo this sentiment, stating that the process can be time consuming but that funds are typically returned once the dust settles.

Groundfloor reviews and complaints

Groundfloor investor feedback is mixed. While its an accredited business with the Better Business Bureau (BBB) and receives an A rating, it averages 2 out of 5 stars from its eight BBB customer reviews, as of October 2020.

There’s not much Reddit chatter about the investing platform, but from the small handful of comments available, investors say they’re happy with returns but that loan defaults are common. While investors typically still get a return on a foreclosed property, the process can tie up funds for years.

Groundfloor customer service

Reach out to Groundfloor’s investor services team by:

- Phone. Call 404-850-9223 weekdays from 9 a.m. to 5 p.m. ET.

- Email. Send an email to support@groundfloor.us.

Bottom line

Groundfloor sets itself apart as one of the few real estate investment platforms that accepts nonaccredited investors. But its asset options are limited and potential loan defaults could hold up your investment for years.

Not sure Groundfloor is the right fit? Explore your real estate investment options with other providers.

Compare Groundfloor to other platforms

Yieldstreet

★★★★★

Finder rating 3.5 / 5

Available asset types

Real estate, Art, Other

Minimum deposit

$10,000

Frequently asked questions

Your reviews

Finder

Editor

You are about to post a question on finder.com:

- Do not enter personal information (eg. surname, phone number, bank details) as your question will be made public

- finder.com is a financial comparison and information service, not a bank or product provider

- We cannot provide you with personal advice or recommendations

- Your answer might already be waiting – check previous questions below to see if yours has already been asked

Finder only provides general advice and factual information, so consider your own circumstances, or seek advice before you decide to act on our content. By submitting a question, you're accepting our finder.com Terms of Use and Privacy and Cookies Policy.

This site is protected by reCAPTCHA and the Privacy Policy and Terms of Service apply.