Finder makes money from featured partners, but editorial opinions are our own.

Home Equity Line of Credit

Need a bit of extra cash? Use the equity in your home to secure low-interest financing by taking out a second mortgage.

{"userFilters":[{"config":{"MULTISELECT":true,"VALUES":"Direct Lender,Broker"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.LENDER_TYPE"},"dataType":"TEXT","label":"Provider Type","order":1},{"config":{"MULTISELECT":true,"VALUES":"First mortgage, Second mortgage, HELOC, Refinancing, Reverse mortgage, Bridge mortgage, Rent to own"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.OFFERED_LOANS"},"dataType":"TEXT","label":"Loans Offered","order":2},{"config":{"MULTISELECT":true,"VALUES":"Alberta, British Columbia, Manitoba, Newfoundland and Labrador, New Brunswick, Northwest Territories, Nova Scotia, Nunavut, Ontario, Prince Edward Island, Quebec, Saskatchewan, Yukon"},"dataSelector":{"recordType":"product","fieldCode":"DETAILS.PROVINCES_TABLE_FILTER"},"dataType":"TEXT","label":"Where do you live?","order":3},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"GENERAL.PROVIDER_ID"},"dataType":"UUID","label":"Provider","order":4}],"niche":{"currencySymbol":"$","decimalPoint":".","decimalPlaces":"2","thousandsSeparator":",","filterBoundsMap":{"product.DETAILS.LENDER_TYPE":null,"product.DETAILS.OFFERED_LOANS":null,"product.DETAILS.PROVINCES_TABLE_FILTER":null,"product.GENERAL.PROVIDER_ID":null}},"prefilled":false}

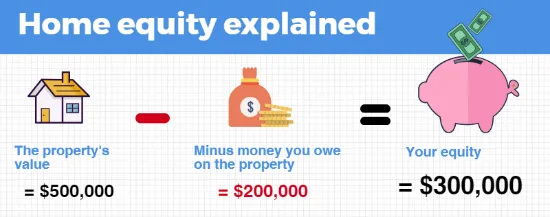

Do you have a significant amount of equity in your home? You might want to consider a home equity line of credit. This type of loan lets you borrow against the appraised value of your home minus the amount you still owe on your mortgage. Just be aware that a HELOC is secured by the title of your home, which means you could risk losing this asset if you default on your payments.

How does a home equity line of credit work?

A home equity line of credit is a secured line of credit that allows borrowers to access funds and pay off their outstanding balance on a flexible basis. It works a lot like a credit card – you can withdraw up to your limit, and you’ll only pay interest on the amount you actually borrow. Any amount you pay toward the principal then goes back into your credit line, which means you can borrow that money again as you see fit.

A home equity line of credit is different from a regular line of credit because it lets you borrow money against the equity in your property. Your property acts as collateral for the line of credit, which means if you don’t repay the amount you borrow, your lender can repossess or sell your home to get its money back. The benefit is that your credit score will matter less when determining your eligibility for financing, and you’ll typically get lower interest rates.

Home equity line of credit rules in Canada

There are a couple of home equity line of credit rules in Canada that define how much you can borrow against your home. These include the following:

You can only borrow up to 65% of your home’s value. You can borrow up to 65% of the value of your home with a home equity line of credit in Canada. This means if your home is worth $500,000, you can access up to $325,000 in financing.

Your mortgage plus your HELOC must be less than 80% of your home’s value. Any outstanding mortgage you have plus your HELOC can’t equal more than 80% of your home’s value. If you still owe 80% or more on your mortgage, you won’t be able to take out a HELOC since your mortgage amount already exceeds allowable borrowing limits.

How much can I borrow?

Here’s how to figure out how much you can borrow with a HELOC:

Take the value of your home and multiply it by 0.8 (0.8 represents the maximum amount of 80%).

From this number, subtract the balance of your mortgage.

The remaining amount is the amount you’d be able to borrow through a HELOC – as long as the amount does not exceed 65% of the value of your home.

Types of home equity lines of credit in Canada

There are two main types of home equity lines of credit in Canada. These include those that are tied to your mortgage and those that are held independently.

HELOC tied to your mortgage. Some lenders will tie the HELOC to your mortgage, which usually means you can borrow up to 80% of the value of your home. This means you’ll need to hold your mortgage and HELOC with the same lender.

Standalone HELOC. This type of HELOC is not linked in any way to your mortgage. You’ll need to abide by the rules above, which means you can only borrow up to 65% of the value of your home.

How much does a home equity line of credit in Canada cost?

You’ll pay a number of different fees with a HELOC, along with variable interest rates that fluctuate in line with the prime rate of Canada.

What interest rates can I expect with a HELOC? As of January 2021, home equity line of credit rates are sitting around 2.35% to 3.45%. The current prime rate is 2.45%, which means you could pay interest rates as low as prime minus 0.10%.

How can I minimize the interest I pay? The most obvious way to cut down on your home equity line of credit rates is to borrow only what you absolutely need. This is because interest is only calculated on the money you withdraw. To save even more money, you should try to make regular payments that are large enough to make a dent in both the interest and principal balance you owe.

When can I make repayments? Your interest payment will usually be automatically withdrawn from your bank account each month. It’s up to you to pay more toward the principal balance if you can.

How does interest accrue for HELOCs?

Home equity line of credit rates in Canada are usually higher than mortgage interest rates and lower than unsecured personal loan rates. The interest on a HELOC is charged daily and is a variable interest rate that’s tied to the prime rate. The prime rate typically changes based on the Bank of Canada’s overnight rate – and it tends to fluctuate frequently, which is why your HELOC interest payments can rise sharply.

HELOC interest rates are typically shown as the prime rate plus or minus any given number. Your financial institution can change that number as they see fit, while the prime rate will be the same across Canada and will fluctuate in line with market conditions. The amount of interest you pay will depend on how much of your home equity line of credit you actually use. For example, if you have a HELOC with a $50,000 line of credit but you only spend $30,000 of your balance, then you’ll only pay interest on the $30,000 you spend.

What fees can I expect to pay with a HELOC?

Appraisal fees. These usually cost from $150 to $250 and are required to pay for an appraiser to price out the value of your home.

Title search fees. These are required to make sure there are no liens on the property. These fees can cost anywhere from $250 to $500.

Legal fees. These fees are usually the most expensive, sitting anywhere from $500 to $1,000 depending on your lawyer.

Administration fees. Admin fees are charged to open the HELOC and costs will vary between providers.

Closing fees. These fees sit anywhere between $200 to $350 and are charged to close your HELOC once you no longer need it.

Inactivity fees. If you don’t use your HELOC, you may also be charged inactivity fees which can vary by provider.

What can I use a HELOC for?

You can use the money in a home equity line of credit for any legitimate purpose – this can include taking a vacation, renovating your home, paying bills, buying a new car or consolidating your debt. Just be aware that you’ll need to put your home on the line to get the financing you need to cover your expenses.

The beauty of taking out a home equity line of credit in Canada is that you won’t have to tell your lender why you need the funds, and you can dip into them whenever you need a top-up. Your lender will then send you your outstanding balance with interest added on and you’ll simply need to make regular payments to stay on top of your debt.

How to use a HELOC to invest

It’s not recommended that you borrow money to invest in the stock market. This is because there’s too much risk involved and you could stand to lose a substantial amount that you’ll still have to pay back. However, you can use your HELOC to invest in a rental property.

This type of property can help you to diversify your portfolio and can give you a consistent form of income in your retirement years. Just keep in mind that using your HELOC to put down a deposit on a second property can be risky, so you should be 100% sure you can make it work before you take the leap.

What makes HELOCs unique?

The following features make HELOCs a unique form of financing:

Structure. This type of loan allows you to use money from a credit limit as needed – similar to how a credit card and typical line of credit works.

Flexible time limits. Many HELOCs don’t come with a specified term, which means you can have it open for as long as you need as long as you keep paying it down.

Repayments. If you choose, you only have to make a minimum payment that covers interest each month (though it’s advisable to make larger payments wherever possible).

Interest charged on the amount withdrawn. You’ll only pay interest on the amount you withdraw from your HELOC, even if your available credit is higher than this amount.

Credit limit. You can qualify for a large amount of credit if your home has a high value and you’ve paid off a decent portion of your mortgage.

Pros and cons of getting a home equity line of credit in Canada

Pros

Competitive rates. A HELOC comes with more competitive rates than those offered with an unsecured line of credit or personal loan.

Can be used for almost anything. The funds can be used for any legitimate purpose – and you typically don’t have to tell your lender what you’re using them for.

Flexible access to funds. You can withdraw money whenever you need it as long as you haven’t reached your available credit limit.

Bad credit doesn’t matter. You’ll typically still be able to qualify for a loan if you have bad credit as long as you own your own home.

Cons

Interest-only payments. While interest-only payments can be a good feature, you may struggle with your debt if you don’t focus on paying down your principal.

Risk losing your property. If your line of credit isn’t repaid according to the terms of your contract, the lender can take your property as payment.

Additional fees. You’ll pay additional fees to get your home equity line of credit set up – especially if you need to get the value of your home appraised.

Potential interest rate increases. Since interest is dependent on the prime rate, your home equity line of credit rates will go up if the prime rate increases.

How can I protect my home?

Always have a cushion of funds available in case you need to cover interest payments for a prolonged period of time. Since you don’t have to pay toward the principal balance, having money set aside for a few months to cover interest can help you if you run into financial difficulties.

Tips for managing a HELOC

Since the equity in your home is used as collateral, there’s a lot to think about when considering a HELOC. Here are some tips to keep in mind:

Minimize the amount of interest payable on your HELOC by making payments toward the principal balance.

Don’t withdraw more funds than you need.

Compare a range of lenders to ensure you’re getting a competitive rate.

Set money aside for a few months’ worth of interest payments in case you go through financial difficulties.

How can I apply for a home equity line of credit?

To apply for a HELOC, you’ll need to meet the following criteria:

Be at least 18 years of age

Be a Canadian citizen or a permanent resident

Have a mortgage worth less than 80% of the appraised value of your home

To apply, compare a variety of home equity line of credit rates in Canada. Once you’ve found a potential lender, contact them to start the process. You’ll need to submit a variety of information including your personal details, information about your home and financial details to prove you can make repayments.

Should I take out a HELOC?

If you’re thinking of taking out a HELOC, you should consider the following:

Whether you have the discipline to stick to a budget

Whether you have the restraint to not use all the funds at once

Whether you have a cash buffer to protect yourself from rising interest rates

Bottom line

A home equity line of credit is a revolving line of credit that lets you secure financing using the equity in your home. This type of lending product typically comes with lower interest rates than personal loans and lines of credit, and you may even be able to qualify with bad credit. Just be aware that if you fail to make your repayments on time, your lender can repossess the property you used as collateral to pay off your debt.

Frequently asked questions

Currently, the prime rate in Canada is fairly low, so you may be able to get a HELOC with rates as low as 2.35% interest. Your best bet to find the lowest rates is to compare providers ahead of time so that you know the median home equity line of credit rates you should be paying.

You may be able to simply request an increase with your financial provider. Some providers will require you to go through the approval process again while others may assess your repayments, credit score and home equity to make a decision on your creditworthiness.

Yes, you can usually make payments towards your HELOC’s principal balance whenever you like. However, if you’re using a HELOC to pay off your mortgage, you could face early repayment fees.

Unfortunately, no. You’ll need to meet certain eligibility criteria to qualify and you’ll have to own your own home. Your loan decision may also be based on factors like your income, employment status, credit score and debt-to-asset ratio.

There’s a real risk that you might not be able to make your payments if you take out a second or third mortgage. This is because you’ll still have to pay off your first mortgage at the same time that you’re making payments on your subsequent loans.

If you can’t make your payments, you’ll likely have to foreclose on your property to make ends meet. This means that your home will be sold off to pay your lenders and you’ll typically get whatever’s left over.

Claire Horwood is a writer at Finder, specializing in credit cards, loans and other financial products. She has a Bachelor of Arts in Gender Studies from the University of Victoria, and an Associate’s Degree in Science from Camosun College. Much of Claire’s coursework has focused on writing and statistics, with a healthy dose of social and cultural analysis mixed in for good measure. In her spare time, Claire enjoys rock climbing, travelling and drinking inordinate amounts of coffee.

Larger living space and a garage still top the list of most desirable features, but Canada’s housing market trends continue to shift. Here’s what buyers want in 2023.

How likely would you be to recommend finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Advertiser Disclosure

finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which finder.com receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. finder.com compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

A home equity line of credit is a secured line of credit that allows borrowers to access funds and pay off their outstanding balance on a flexible basis. It works a lot like a credit card – you can withdraw up to your limit, and you’ll only pay interest on the amount you actually borrow. Any amount you pay toward the principal then goes back into your credit line, which means you can borrow that money again as you see fit.

A home equity line of credit is a secured line of credit that allows borrowers to access funds and pay off their outstanding balance on a flexible basis. It works a lot like a credit card – you can withdraw up to your limit, and you’ll only pay interest on the amount you actually borrow. Any amount you pay toward the principal then goes back into your credit line, which means you can borrow that money again as you see fit.